Sandra Beldine Otieno, MSc

August 12, 2025

Share article

Kasi Insight’s Share of Wallet dataset captures how consumers distribute their monthly household spending across both essential and lifestyle categories in multiple African markets. By tracking what people purchase, how much they spend in each category, and the key factors influencing those decisions. The Q2 2025 Nigeria data reveals how shoppers prioritise fresh staples while navigating wide variations in spending power and purchase drivers.

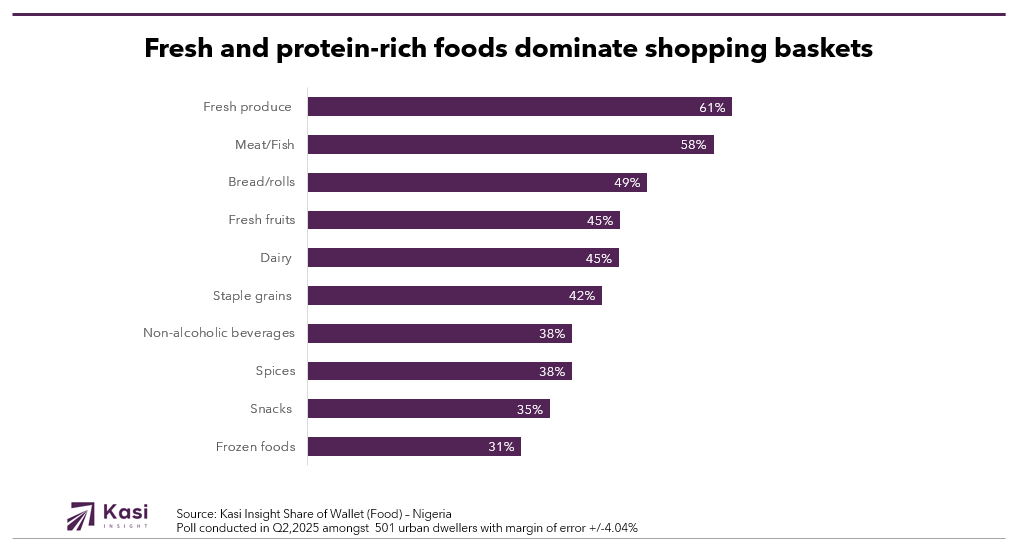

Fresh produce leads Nigeria’s food purchases, with 61% of households buying items such as potatoes, tomatoes, and onions each month. Meat and fish follow at 58%, highlighting the continued centrality of protein in the diet. Bread and rolls are purchased by 49% of consumers, while fresh fruits and dairy products such as milk, yoghurt, and cheese each record a 45% monthly purchase rate.

Staple grains, including rice, maize meal, and pasta, are bought by 42% of households, reinforcing their role as everyday cornerstones. Spices and non-alcoholic beverages each attract 38% of buyers, while snacks reach 35% and frozen foods 31%. The dominance of fresh and staple categories over convenience foods suggests that Nigerian consumers continue to anchor their shopping habits in traditional dietary choices, supplementing them with occasional indulgences rather than replacing them.

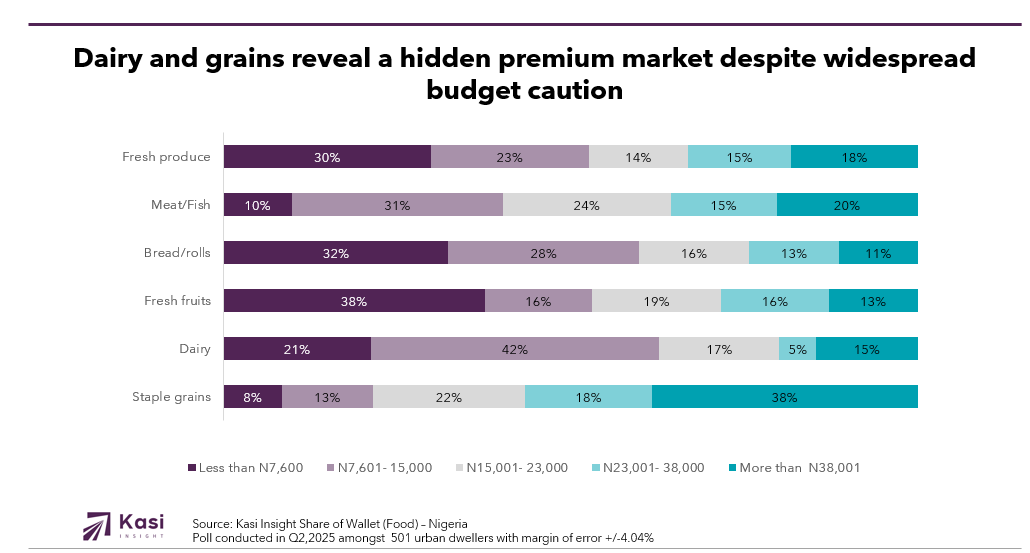

Spending data reveals a stark divide between households keeping costs low and those paying for premium choices. For meat and fish, 30% of consumers spend less than ₦7,600 per month, while 18% spend more than ₦38,000, pointing to two very different market realities. Fresh produce spending is more evenly distributed, with 31% of buyers in the ₦7,601–₦15,000 range and 24% in the ₦15,001–₦23,000 bracket, showing its role as a broadly purchased staple. Bread and rolls remain a predominantly low-cost purchase, with 38% of households spending under ₦7,600.

Fresh fruits see their highest spend concentration in the ₦7,601–₦15,000 bracket at 42%, while dairy is firmly premium, with 38% of consumers spending over ₦38,000 monthly. Staple grains display a more balanced spend profile, with strong representation in both mid-range and higher tiers.

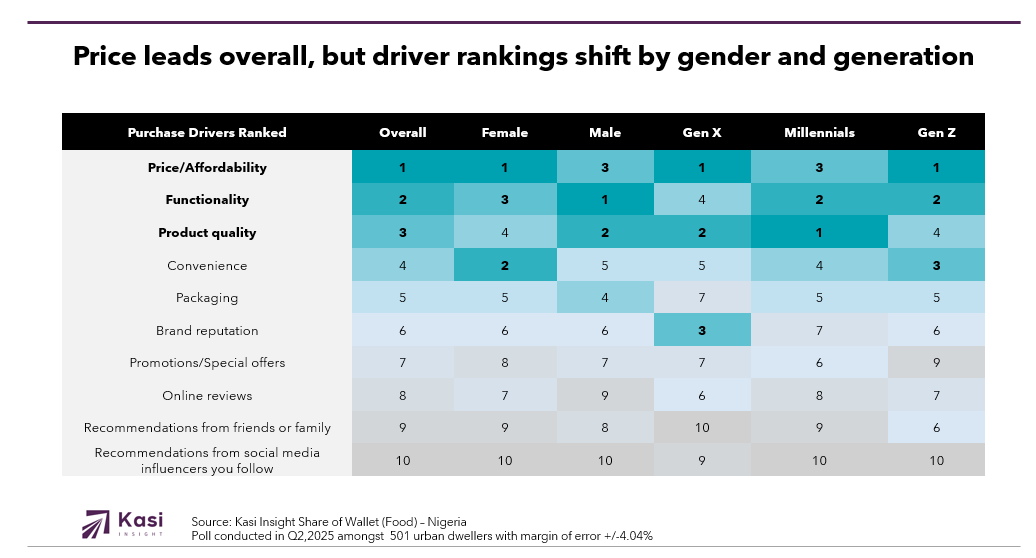

Affordability dominates food purchase decisions overall, taking the top spot for most groups except men, who prioritise functionality. Functionality, which reflects how well a product serves its purpose, ranks second overall and is particularly valued by male shoppers. Product quality comes third overall but is the leading driver for Millennials, suggesting that younger buyers may be more inclined to reward brands that deliver superior standards.

Convenience ranks fourth overall but jumps to second place among women, pointing to the appeal of time-saving formats for this group. Packaging, brand reputation, promotions, and online reviews carry some weight but remain secondary to practical value. Recommendations from friends, family, or influencers rank lowest, showing that Nigerian consumers are less swayed by endorsements than by tangible product benefits. This focus on value and performance underscores why brands must deliver more than just low prices to win loyalty.

The Q2 results show that Nigerian consumers are staying loyal to core food purchases, continuing to prioritise fresh produce and proteins even as budgets tighten. Brands that wish to grow must combine value leadership with targeted offers that meet specific needs. Premium dairy appeals strongly to a smaller but high-spending group, while convenience-focused solutions could resonate with the 61% of households buying fresh produce regularly. The most successful strategies will connect affordability with clear functional or quality advantages for different consumer segments.

Retailers and manufacturers can leverage high-frequency categories such as fresh produce and meat as anchors for promotions, loyalty programmes, and cross-category deals. At the same time, offering tiered product ranges can ensure relevance across both lower-income and premium-spending households. In a competitive market where every percentage of share of wallet is hard-won, the brands that succeed will be those that bridge the gap between delivering value and inspiring aspiration.

Share on socials using this caption: 🥔🍅🐟 Nigerians keep fresh staples at the heart of their diets even as budgets tighten. Q2 data shows a widening gap between value seekers and quality spenders price wins, but quality and function drive loyalty. #Nigeria #FoodTrends #ConsumerInsights #KasiInsight #ShareOfWallet

2851 views

Share article

Cameroon’s protein market in 2026 is shifting from habitual consumption to structured and intentional demand

Consumer Choices Post COVID-19 Are Redefining Kenya’s Beverage Landscape

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories