Alison Okatch

April 15, 2026

Share article

The defining characteristic of Cameroon’s protein market in 2026 is not low demand, but controlled demand. Households are still consuming protein, but they are doing so with intention, spacing out usage, simplifying choices, and prioritizing essentials.

The Kasi Consumer Basket Survey insights underpin this analysis, a framework designed to plan and execute consumer marketing and experience strategy by tracking household purchasing patterns, preferences, and behaviors across the typical basket of goods, enabling a structured understanding of how consumption shifts over time.

Cameroon’s protein landscape is best understood not as a single category, but as three distinct consumption systems: meat and fish, supplemental proteins, and extenders (beans and legumes). Across all three, the past four years show a consistent structural shift away from frequent, habitual consumption toward more managed, intentional usage.

By 2026, protein consumption is no longer dominated by daily intake. Instead, it is concentrated in medium-frequency occasions, which now account for 54.6% of overall protein consumption, while high-frequency usage falls to 33.8%. Meat and fish are increasingly consumed on a weekly rhythm, supplemental proteins are consolidating around a few core staples, and extenders are being used more selectively.

The market today is not shrinking uniformly; it is fragmenting into categories with different roles in the household diet.

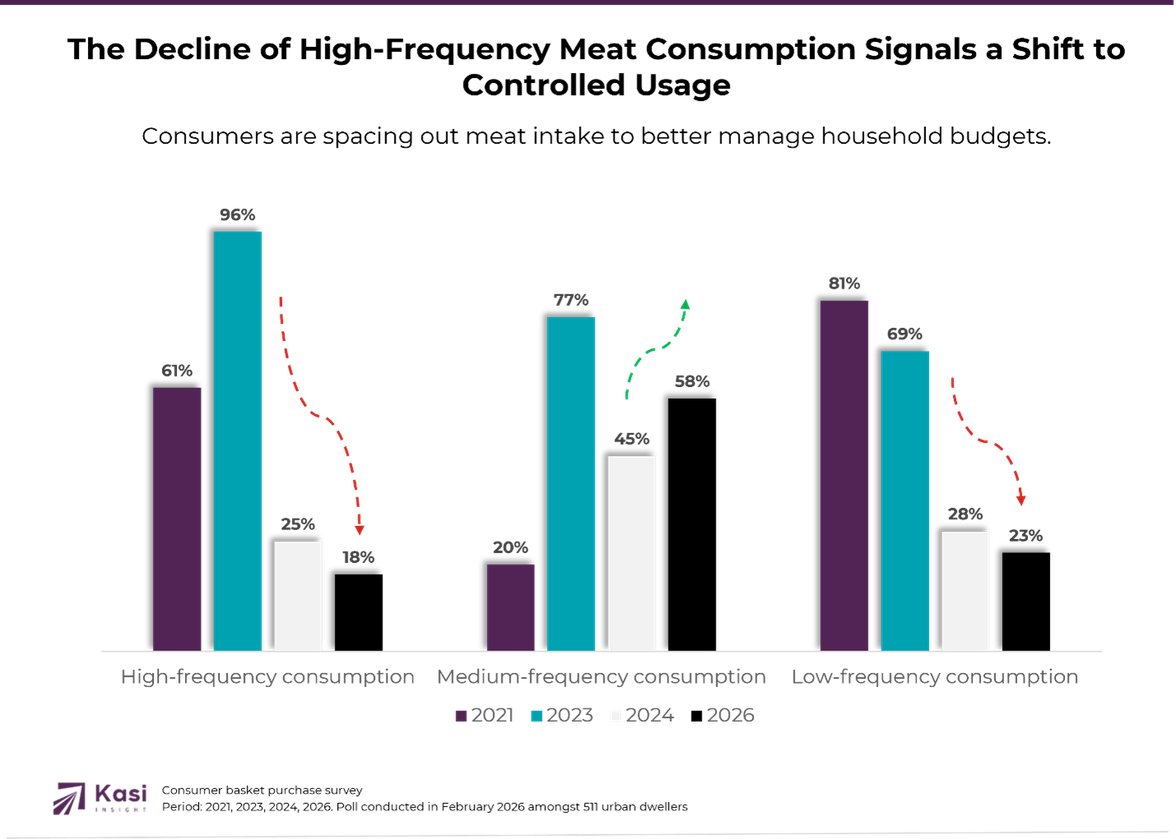

Within meat and fish, the most important shift between 2024 and 2026 is not just the decline in high-frequency consumption (25% to 18%), but the clear migration into structured, weekly usage. The increase in once-a-week consumption to 32.4% indicates that households are deliberately timing meat intake rather than consuming it freely.

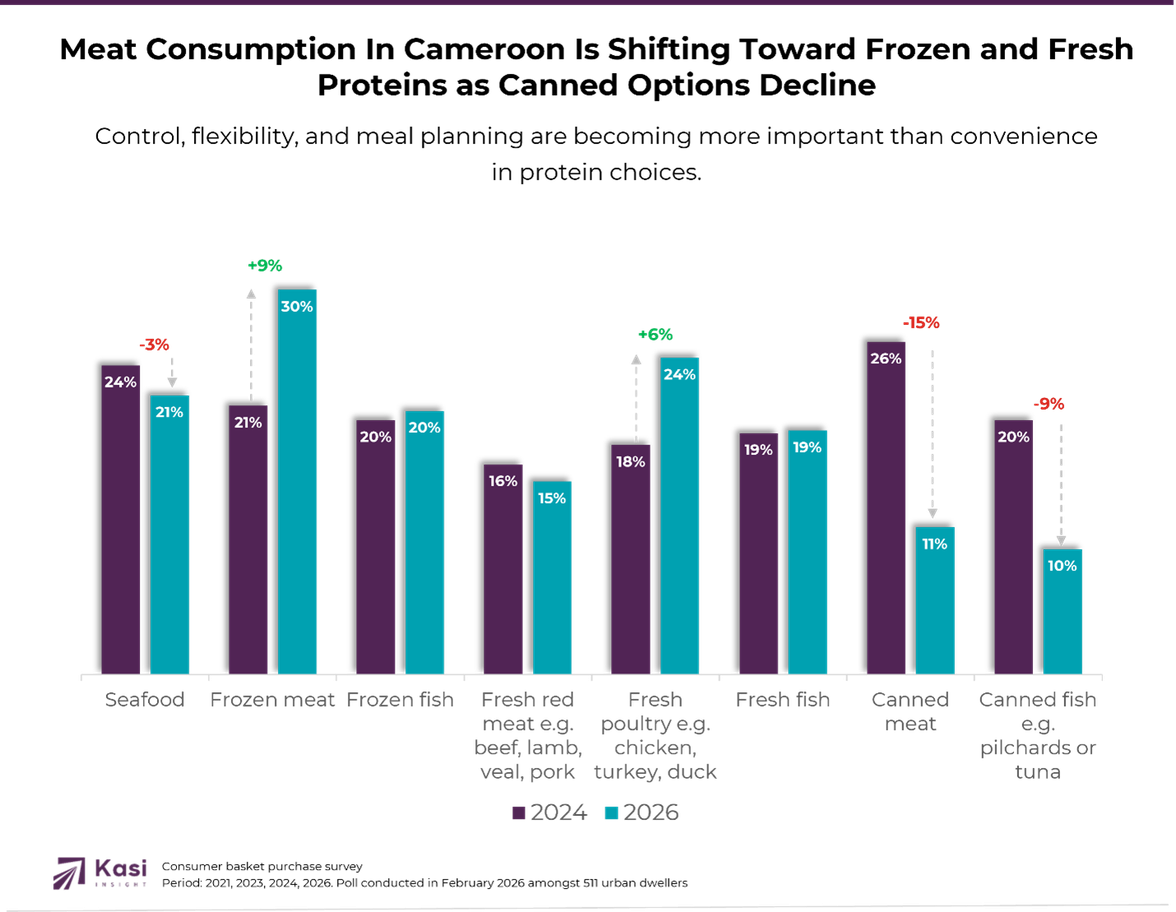

This is reinforced by what consumers are buying: frozen meat increases significantly from 20.6% to 29.5%, and fresh poultry rises from 17.6% to 24.3%, while canned fish declines sharply to 9.6%. What is winning here are formats that allow storage, portioning, and control over spend per meal. The decline in canned options suggests that convenience alone is not enough, value perception must align with portion flexibility.

The opportunity for brands lies in reinforcing meat as a planned consumption item, offering smaller cuts, multi-use packs, or formats that can stretch across meals. The driver of change is clear: consumers are not rejecting meat, but re-timing and restructuring how it fits into their weekly budgets.

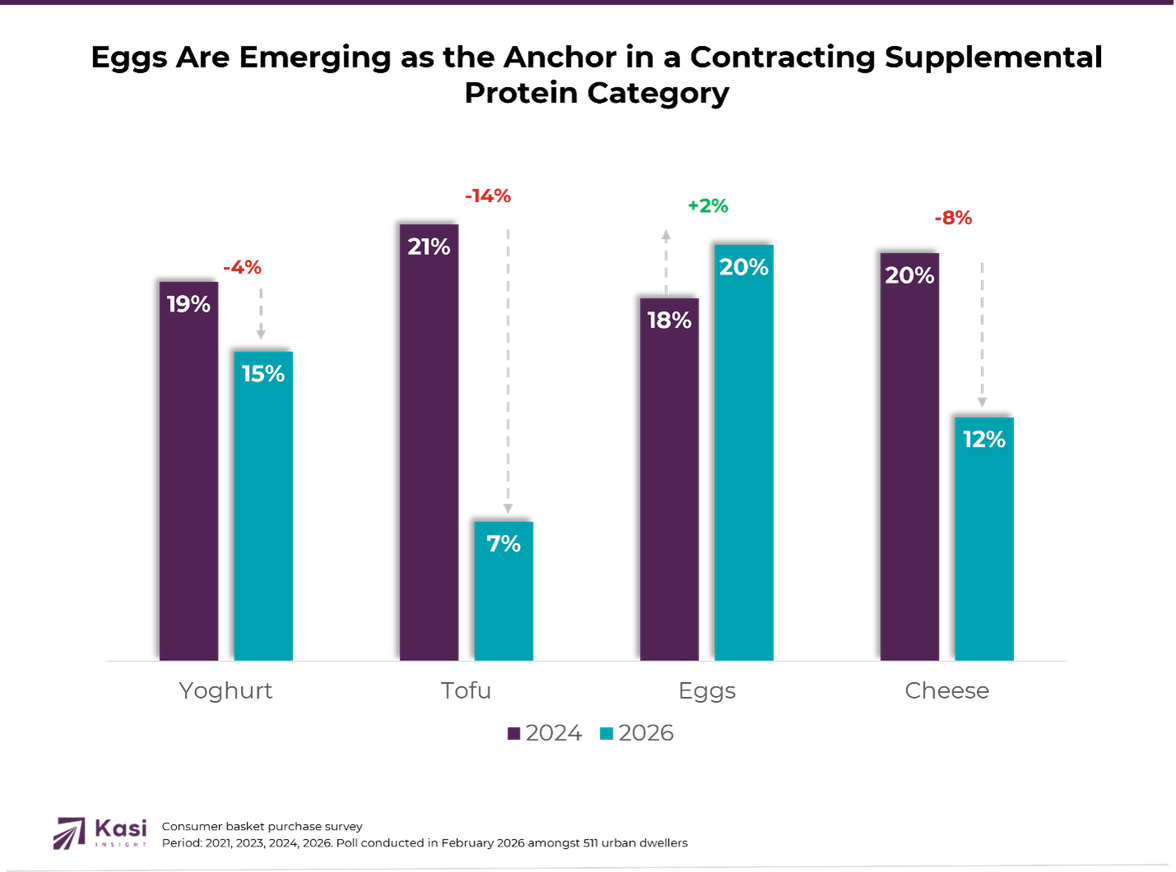

The supplemental protein category is undergoing the most visible consolidation. Between 2024 and 2026, yoghurt declines from 19% to 15.1%, cheese from 19.9% to 11.9%, and tofu drops sharply to 6.8%. Eggs, however, edge up to 20.3% and dominate across all income groups at approximately 47% penetration.

The opportunity lies in either competing directly with eggs on value or positioning other products as complements that enhance egg-based meals.

For brands in dairy or alternative proteins, the challenge is clear: justify inclusion in a basket that is becoming increasingly minimal.

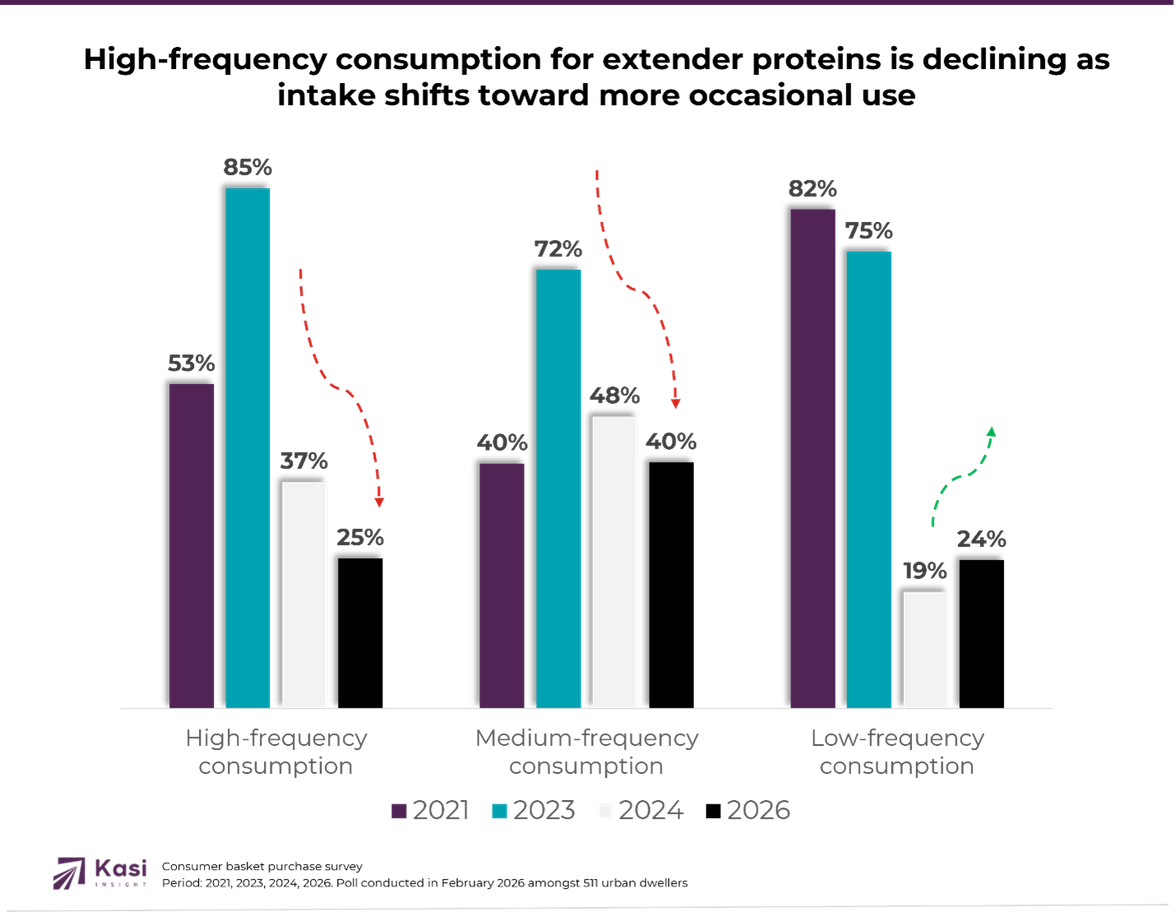

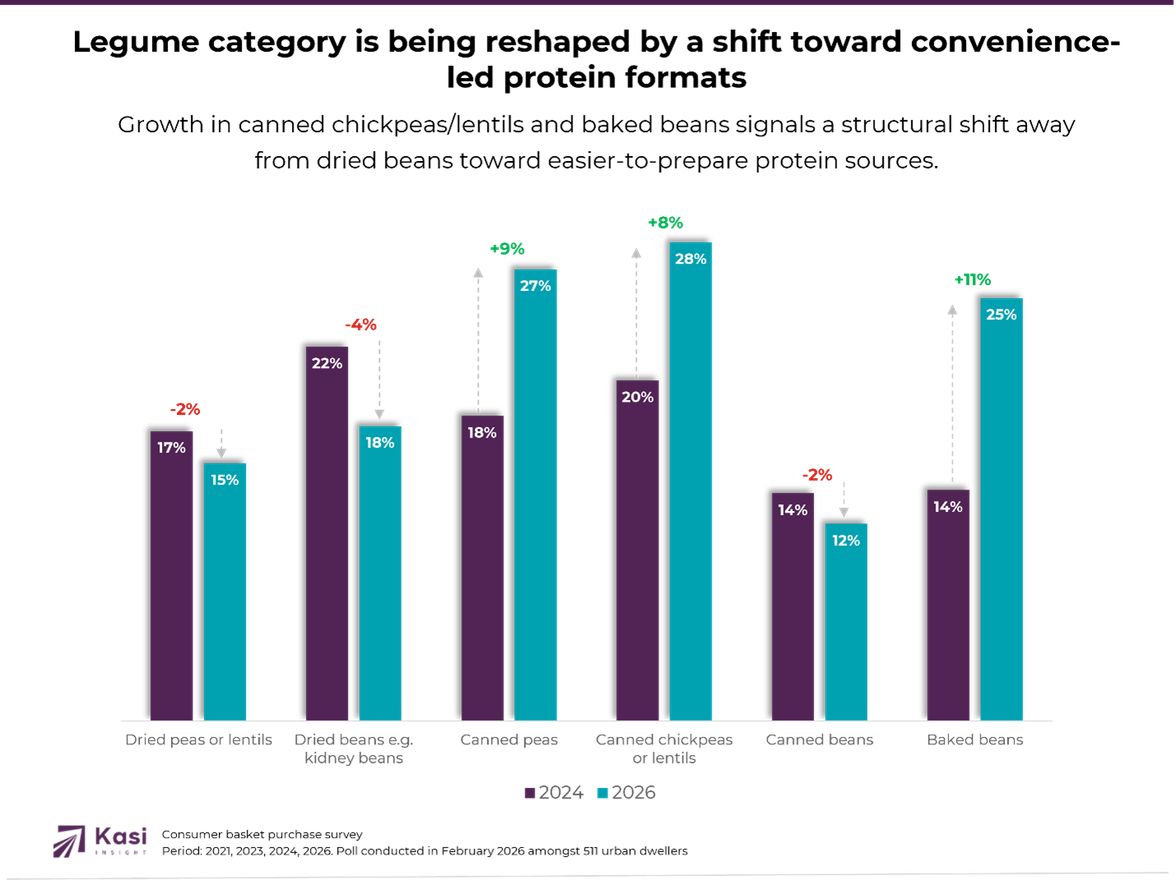

Extenders are being redefined, while high-frequency consumption falls from 37.1% in 2024 to 24.6% in 2026, purchase behavior reveals a more nuanced shift. High-frequency consumption drops significantly from 37.1% in 2024 to 24.6% in 2026, while low-frequency rises to 24.3%, indicating that extenders are also being deprioritized.

Between 2024 and 2026, there is a clear move away from preparation-intensive formats like dried peas (17% to 15%) and dried beans (22% to 18%), and a strong increase in ready-to-use formats such as canned peas (18% to 27%), canned chickpeas (20% to 28%), and baked beans (14% to 25%).

The opportunity for brands lies in reducing friction, through pre-cooked, packaged, or hybrid solutions that make beans easier to integrate into modern, time-constrained meal patterns.

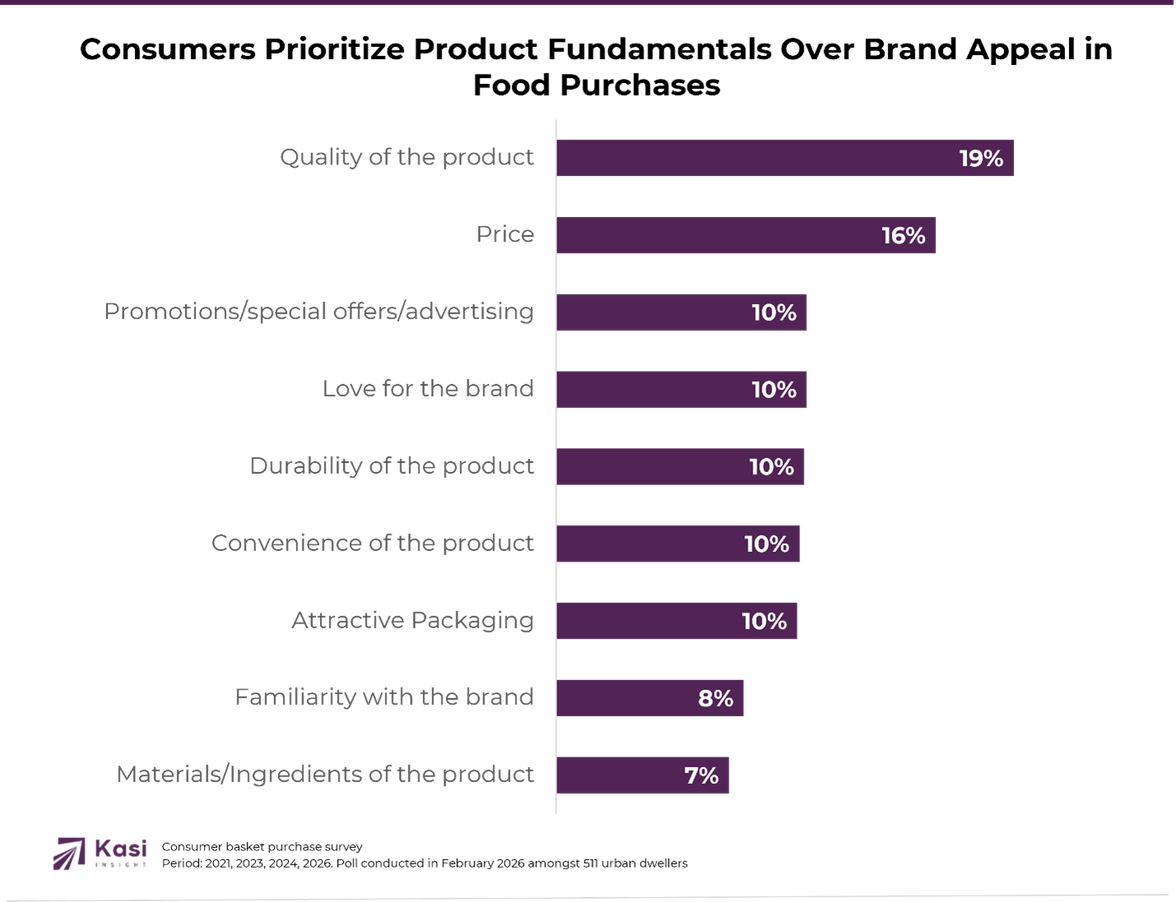

When it comes to decision-making, consumers consistently prioritize quality (18.8%) and price (15.6%), followed by promotions, brand affinity, and convenience. However, in the current context, these factors are interpreted through a more practical lens. Quality is not about premium positioning, but about reliability and nutritional value; price is not just about being cheap, but about enabling repeat purchase. Convenience, packaging, and familiarity all play supporting roles, but only when they reinforce the core value equation. This means that brands must deliver a clear, tangible benefit that fits within constrained budgets.

The opportunity lies in translating these drivers into actionable propositions — products that are affordable, easy to use, and trusted to deliver consistent value over time.

For brands, this shifts the focus from driving volume to enabling participation within this new rhythm. Success will come from products that fit into weekly consumption patterns, offer flexibility in portioning, and align with the economic realities consumers face. Meat brands must embrace their role as scheduled proteins, supplemental brands must either align with or complement eggs, and bean brands must reduce preparation barriers to regain frequency. Across all categories, the brands that win will be those that understand that protein consumption has not disappeared—it has been disciplined, structured, and redefined by the consumer.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

#Cameroon #ConsumerInsights #AfricaConsumer #FMCG #FoodTrends #MarketInsights #KasiInsight #ConsumerBehavior #CostOfLiving #AfricaMarkets #RetailInsights #ProteinMarket

501 views

Share article

Consumer Choices Post COVID-19 Are Redefining Kenya’s Beverage Landscape

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories

Fresh staples stay strong as Nigeria’s food market splits between value seekers and quality spenders