Paul Cheloti Mulongo

August 18, 2025

Share article

Kasi Insight’s consumer trust survey tracks how Africans perceive trust across brands, companies, governments, and institutions. It offers valuable insight into how trust is built, where it is lost, and how it varies across markets. In Ivory Coast, the findings highlight that while financial services perform relatively well on capability, they continue to face challenges in convincing consumers that they act fairly, transparently, and in the best interests of their customers.

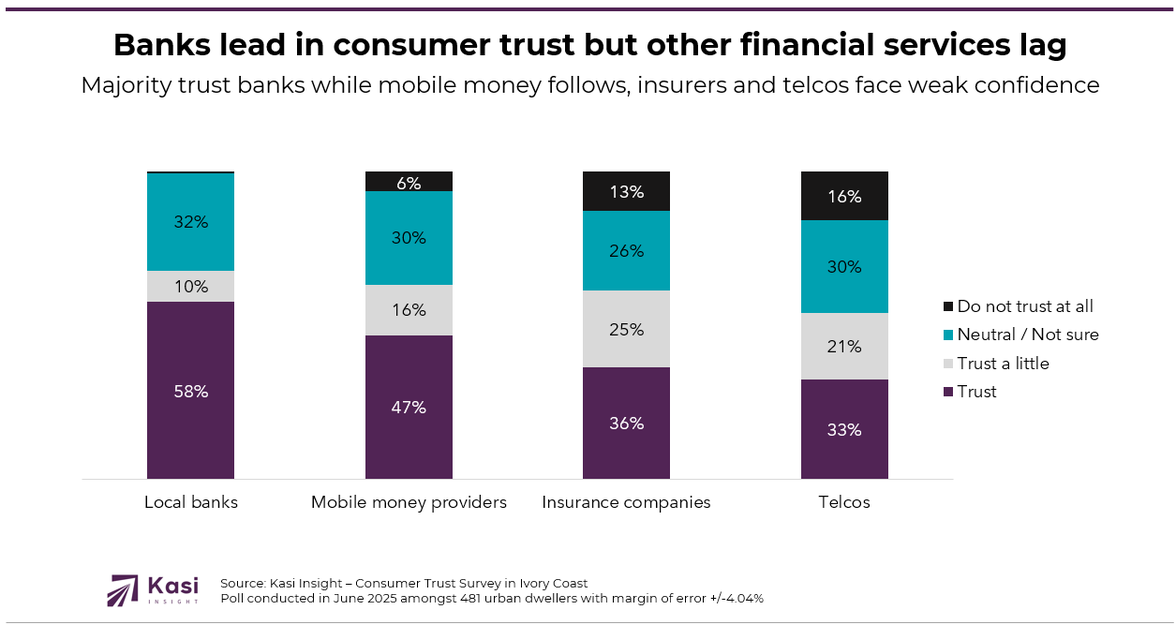

Among financial services providers, local banks lead with 58% of consumers saying they trust them to act responsibly and provide good service. This position reflects the longstanding role of banks in safeguarding deposits, enabling payments, and offering financial stability. Yet 32% of consumers remain neutral and 1% say they do not trust banks at all. Such ambivalence is a warning sign, because neutrality can quickly shift into distrust if banks fail to maintain service quality or if new entrants offer more compelling alternatives.

Mobile money providers follow with 47% of consumers expressing trust. Their importance in supporting daily transactions, remittances, and financial inclusion is evident, yet they face higher outright skepticism than banks, with 6% of respondents saying they do not trust them at all. Insurance companies and telcos struggle the most, with trust levels at only 36% and 33% respectively. Both categories face persistent reputational challenges linked to product complexity, inconsistent claims handling, service disruptions, and perceived unfairness in pricing.

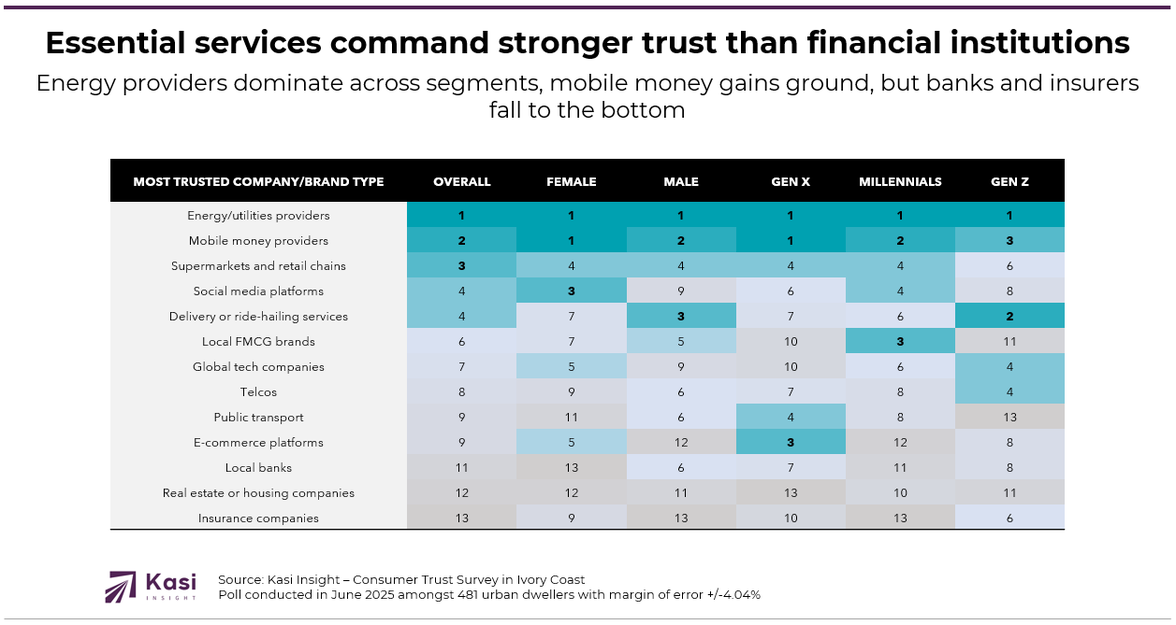

When asked to name their single most trusted company or brand, consumers consistently point to energy and utilities providers. Their ability to deliver indispensable services makes them the most trusted across genders and generations. This result underlines that trust gravitates toward providers whose value is visible, direct, and unavoidable in everyday life.

Mobile money providers rank second overall, and women place them first. Younger consumers, especially Gen Z, elevate delivery and ride-hailing services, showing that digital-first platforms that shape lifestyle experiences are gaining ground in trust rankings. Supermarkets and retail chains consistently take third place, reflecting the importance of frequent, everyday interactions. Banks, insurers, and real estate companies, by contrast, appear much lower in the rankings. For the financial sector, this signals that being central to the economy is not enough to secure reputational strength.

When consumers evaluate their most trusted providers, competence emerges as the strongest attribute. Almost 59% rate competence at 4 out of 5, and another 13% give the highest score. This shows that companies considered trustworthy are seen as effective and operationally capable. For financial services, the finding means that consumers largely accept that banks and mobile money providers can deliver on their promises and that their systems work as expected.

However, this strength does not extend to perceptions of ethics and transparency. Only 36% give high ratings for ethics and 37% for transparency, while 17% rate transparency as low as 2 out of 5. These results highlight a critical weakness: even when consumers recognize capability, they remain doubtful about whether financial providers act fairly, honestly, and openly. For banks, this can be manifested in concerns over fees and hidden charges. For mobile money, the issues often revolve around dispute resolution and fraud prevention. For insurers and telcos, the challenges are even more severe, rooted in customer frustration with claims and billing practices.

The findings underline that competence is now only the starting point. Consumers expect reliability as a given, and financial institutions cannot rely on it to differentiate themselves. What increasingly matters is visible integrity. Banks will need to build trust by being transparent about costs, communicating openly, and engaging more directly with their clients. Mobile money providers must strengthen consumer protections and show that they take customer concerns seriously. Insurers need to simplify products and deliver on claims processes to rebuild confidence, while telcos must combine service reliability with openness in pricing.

Trust is no longer just a reputational factor for the financial sector in Ivory Coast. It is becoming a source of competitive advantage. Consumers are cautious and selective, and in a market where neutrality dominates, credibility will determine which institutions secure loyalty and advocacy. The financial providers that move beyond competence to actively demonstrate fairness and transparency will not only strengthen their reputations but also position themselves to lead in a market where trust is increasingly the currency of growth.

Share on socials using this caption: 📊 In Ivory Coast, consumers trust banks and mobile money provider to deliver but remain doubtful about fairness and transparency. Energy providers top the trust rankings, proving that essential services earn the strongest confidence. For financial services, the challenge is to go beyond reliable systems and build visible integrity. 💡 #ConsumerTrust #IvoryCoast #FinancialServices #Banking #Fintech #Africa

2724 views

Share article

Equity leads where financial journeys begin, while the greatest opportunity lies in capturing more value as those journeys mature.

The Rise of Behavioral Intelligence in African Investing

The Signal Investors Are Missing in African Equity Markets