Alison Okatch

April 22, 2026

Share article

For over a decade, financial inclusion across Africa has largely been defined by access; access to accounts, access to payments, access to credit. But in Ghana, the story is shifting. The post-COVID behavioral data suggests that the conversation is no longer about whether consumers can participate in the financial system, but how deliberately they are choosing to engage with it.

Ghanaian consumers are not simply adopting financial tools, they are reshaping their financial lives around control, liquidity, and resilience. This shift is subtle but profound. It signals the emergence of a more mature financial consumer, one who is less focused on expansion and more focused on discipline.

And now, a structural development, the Ghana Card becoming a payment instrument in April 2026, may accelerate this transformation even further.

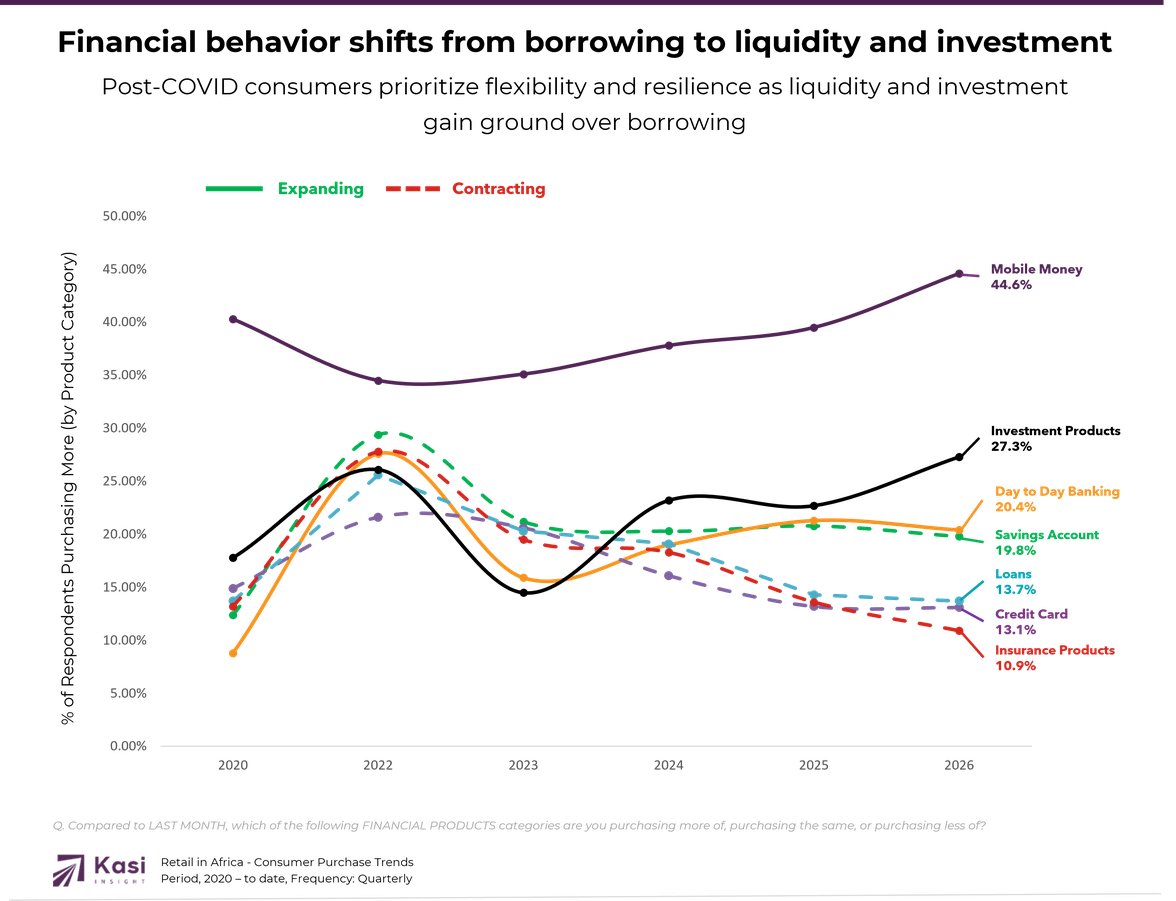

Mobile money has evolved from a convenience into the backbone of Ghana’s financial ecosystem. In 2026, 44.6% of consumers reported expanding their mobile money usage — the highest level observed in six years. At the same time, only 5.7% reported contracting their usage, signaling deepening entrenchment rather than temporary adoption.

This pattern reflects more than technology adoption. It reflects behavior. Consumers are prioritizing tools that offer speed, flexibility, and immediate control. In uncertain economic conditions, liquidity becomes more valuable than long-term returns. Mobile money satisfies this need better than traditional financial instruments.

The emergence of the Ghana Card as a payment instrument reinforces this trajectory. Built as an interoperable layer rather than a bank product, the Ghana Card wallet mirrors the attributes that have made mobile money dominant, accessibility, simplicity, and immediacy. Rather than disrupting the system, it may deepen the liquidity-first behavior already taking shape.

While liquidity tools strengthen, borrowing behavior tells a different story. Credit card expansion peaked at 21.6% in 2022 before settling at 13.1% in 2026. Loan expansion followed a similar path, rising to 25.6% in 2022 before easing to 13.7% in 2026.

This is not a collapse in credit usage. It is a recalibration. Consumers are not abandoning borrowing entirely, they are choosing not to expand their exposure. The distinction matters. It signals a population that is becoming more intentional about financial risk.

In this context, identity-based financial infrastructure such as the Ghana Card could reshape how credit is introduced. By linking transactions to verified identity, the system can create financial histories for consumers previously invisible to lenders. This opens the door to credit access without relying on traditional application-driven models, a potentially transformative shift for financial inclusion.

Brands and lenders need to recalibrate toward a more selective credit environment where growth is driven by precision rather than scale; success will depend on stronger risk intelligence, behavioral scoring, and products designed around controlled exposure rather than aggressive credit expansion.

The savings story in Ghana is no longer defined by growth, but by stability. The share of consumers holding savings pockets steady rose from roughly half of consumers in 2022 to 72.4% in 2026. Savings accounts show a similar pattern, stabilizing around 63.9%.

This behavior reflects defensive financial management. Consumers are not aggressively building buffers, but they are protecting the ones they have. It is a posture consistent with prolonged economic uncertainty and inflationary pressure.

This shift also suggests something deeper: financial maturity. Consumers who once focused on building access are now focused on maintaining resilience.

Financial institutions will need to shift from competing on savings accumulation to embedding savings into daily financial behavior, prioritizing liquidity access, trust, and seamless integration within transactional ecosystems over standalone deposit products.

Even as borrowing slows, investment appetite is strengthening. In 2026, 27.3% of consumers reported expanding investment product usage, a six-year high.

This is a critical insight. Consumers are not retreating from financial risk entirely. Instead, they are migrating toward instruments that do not create repayment obligations. In other words, the appetite for upside remains, but the tolerance for leverage is declining.

Insurance, however, tells a more fragile story. Contracting behavior rose to 30.6% in 2026, reinforcing a long-standing pattern: insurance is often the first product consumers cut when budgets tighten.

Here again, infrastructure innovation may reshape the narrative. If insurance is bundled into widely adopted platforms like the Ghana Card wallet, distribution friction could fall — potentially altering adoption dynamics.

Investment providers and insurers must adapt to a consumer who still seeks upside but avoids rigid commitments, making flexibility, low entry thresholds, and embedded distribution channels critical to sustaining engagement.

Across financial products, Millennials remain the dominant growth engine, while Gen Z is accelerating into financial participation. Meanwhile, Gen X and older cohorts are largely stabilizing or contracting.

This generational dynamic matters because it suggests that the future of Ghana’s financial system will be shaped by consumers entering adulthood in a digital-first, identity-enabled ecosystem.

The Ghana Card’s rollout therefore arrives at a pivotal moment. Capturing younger consumers early could define financial behavior for the next decade.

The next wave of financial growth will be shaped by digitally native consumers, requiring brands to build integrated, identity-led ecosystems that capture users early and sustain engagement across payments, credit, savings, and investments within a unified experience.

For financial institutions, fintechs, and policymakers, the implication is clear. The next phase of financial innovation in Ghana will not be defined by reaching the unbanked alone. It will be defined by serving a more deliberate, disciplined, and digitally anchored consumer.

Contact our team today to explore how Ghana’s shifting financial behavior can inform your strategy, product design, and market positioning. Win with confidence with Kasi Insight. https://www.kasiinsight.com

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

#GhanaEconomy #FinancialInclusion #FinancialBehaviour #DigitalFinanceAfrica #MobileMoney #FintechAfrica #ConsumerInsights #EconomicIntelligence #CreditTrends #SavingsBehaviour #InvestmentTrends #BankingAfrica #FinancialServices #AfricaFintech #BehavioralEconomics #DataAnalytics #MarketInsights #WealthManagementAfrica #GhanaFintech #EconomicTrendsAfrica

435 views

Share article

Equity leads where financial journeys begin, while the greatest opportunity lies in capturing more value as those journeys mature.

The Rise of Behavioral Intelligence in African Investing

The Signal Investors Are Missing in African Equity Markets