Sandra Beldine Otieno, MSc

August 5, 2025

Share article

Kasi Insight’s Share of Wallet provides a view of how consumers distribute their spending across various consumer-facing categories in African markets. In Kenya, data from H2 2024 to H1 2025 reveals a telecom sector in transition. Consumers are thinking more critically, spending more deliberately, and demanding stronger performance from brands.

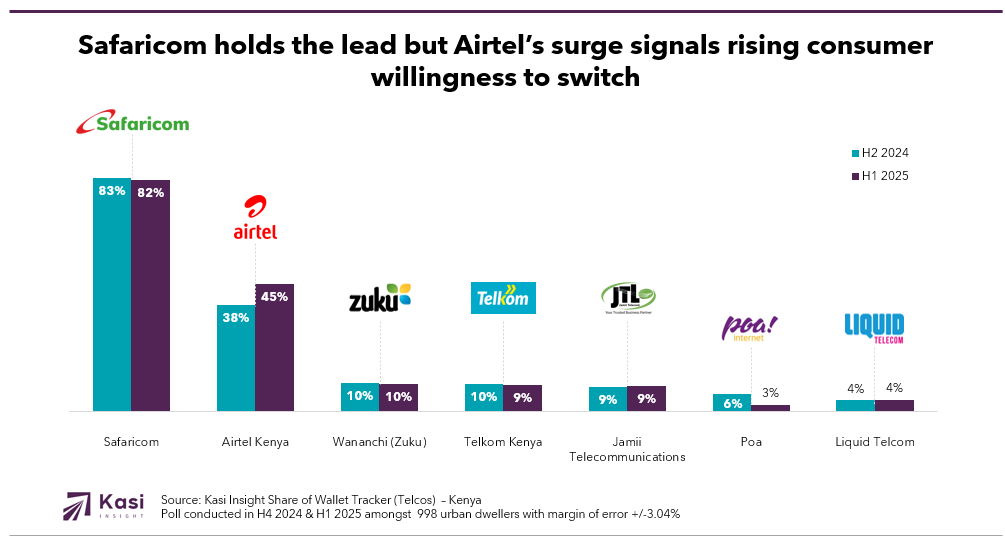

Safaricom continues to hold the largest share of primary telecom users in Kenya, with 82% of consumers naming it as their main provider in H1 2025. This figure represents only a slight drop from 83% in H2 2024, but even a small dip matters in a market where alternative options are gaining traction. Airtel Kenya has made significant progress, rising from 38% to 45% within the same timeframe. This upward shift reflects growing consumer openness to switching providers when better value is perceived, especially in terms of affordability and network performance.

Other providers have maintained modest shares or experienced slight declines. Zuku held steady at 10%, while Telkom Kenya declined from 10% to 9%, and Jamii Telecommunications remained unchanged at 9%. Poa experienced a more noticeable drop from 6% to 3%, potentially due to service limitations or increased competitive pressure. Liquid Telecom remained consistent at 4%. These figures suggest that although Safaricom continues to dominate, Airtel’s growth shows that brand strength is not static.

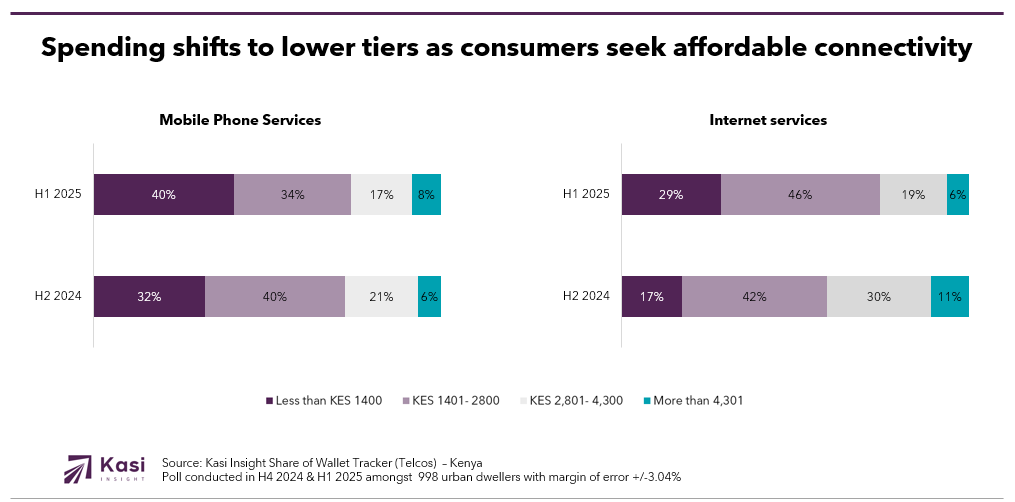

The data also reveals how telecom spending is evolving, with a visible shift toward lower monthly expenditure across both mobile and home internet services. In H2 2024, 32% of consumers spent less than KES 1400 per month on mobile services. By H1 2025, that number had risen to 40%, indicating a significant move toward cost-conscious usage. The mid-tier spending group, those allocating between KES 1401 and 2800, fell from 40% to 34%, and those spending between KES 2801 and 4300 dropped from 21% to 17%. Interestingly, the highest spending group, those allocating over KES 4301, rose from 6% to 8%, suggesting that while many are cutting back, a smaller segment is still willing to invest in premium telecom services.

Similar patterns are reflected in home internet usage. In H2 2024, only 17.4% of consumers spent less than KES 1400 monthly, but this rose sharply to 28.5% in H1 2025. At the same time, those spending over KES 4301 declined from 11% to 6.3%. The KES 1401 to 2800 range remains the most popular, growing from 41.9% to 45.7%. This shift signals that consumers are recalibrating rather than disconnecting. Many are opting for plans that provide good-enough service at a price that matches tighter household budgets.

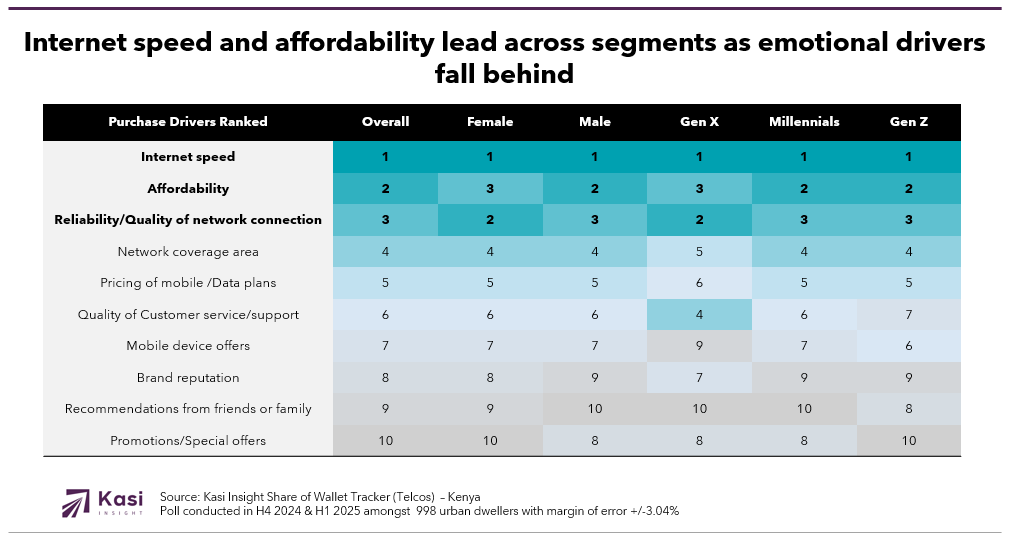

When it comes to choosing a telecom provider, consumers across all groups are aligning around a clear set of priorities. Internet speed ranked as the number one factor for every demographic segment. This consistency signals that reliable and fast connectivity is now viewed as a fundamental utility. Affordability follows closely behind, especially for younger users and males, while Gen X and female respondents placed more weight on reliability and quality of network connection. These rankings show that consumers are choosing telecom services based on practical needs, not perceived brand strength or advertising visibility.

Other factors rank far lower in importance. Brand reputation, mobile device offers, peer recommendations, and promotional campaigns are consistently at the bottom of the list. Gen Z showed slightly more interest in device bundles and recommendations from friends, but not enough to change their top priorities. Customer service ranked higher among Gen X respondents, suggesting that older users still value support and responsiveness. Ultimately, the market is rewarding telcos that focus on core performance attributes, speed, affordability, reliability over flashy marketing or promotional tactics that do not address essential service needs.

The evolving patterns in spending, provider preference, and purchase drivers point to a telecom market that is entering a more competitive and discerning phase. Consumers are thinking carefully before committing to a provider, and they are willing to move when expectations are not met. Safaricom still benefits from scale and trust, but Airtel’s strong growth shows that momentum is shifting toward brands that compete aggressively on price and performance. A failure to adapt to these new consumer expectations could result in lost relevance and eroding share.

To win in this environment, telecom brands must sharpen both their product strategy and their value communication. That means designing mid-tier bundles that align with consumer budgets, ensuring fast and reliable connections across the country, and addressing segment-specific needs with tailored experiences. Gen Z and Millennials want flexibility and affordability, while Gen X values customer support and consistent performance. Brands that can strike the right balance between price, speed, and service will be best positioned to capture a growing share of consumer wallets and stay ahead in a market that no longer rewards presence without performance.

Share on socials using this caption: 📊 Kenyan consumers are rethinking their telecom spend 💰 with Airtel gaining ground and Safaricom under pressure to prove its value 📉 Speed tops all priorities 🚀 while brand reputation and promos fall flat 🎯 #Telecom #ConsumerTrends #InternetSpending #DataPlans #CX #ShareOfWallet #KasiInsight

2173 views

Share article

Starlink’s Global Outage Reveals Fragility in Africa’s Connectivity Progress

Mobile money outpaces fintech in Ghana’s digital finance

Starlink in Africa: Two years later, the promise is visible but so are the cracks