Sandra Beldine Otieno, MSc

June 18, 2025

Share article

As Kenya enters the second half of 2025, the food and beverage market is being reshaped by persistent financial pressure and a shift in how households define value. Food remains an essential category, but it is no longer protected from budget cuts or lifestyle tradeoffs. For more than two years, household sentiment and spending have remained negative. In May 2025, the Consumer Sentiment Index stood at -6 while the household spending index fell to -13. These figures reflect not a temporary dip but a long-term reset in behavior.

Data from Kasi Insight’s Consumer Sentiment Index, Share of Wallet Tracker, and Cost of Living Tracker shows that people are no longer waiting for recovery. Instead, they are building new routines, rethinking consumption, and reassessing what matters in their daily food decisions. Three powerful shifts now characterize how food and beverage choices are being made in 2025.

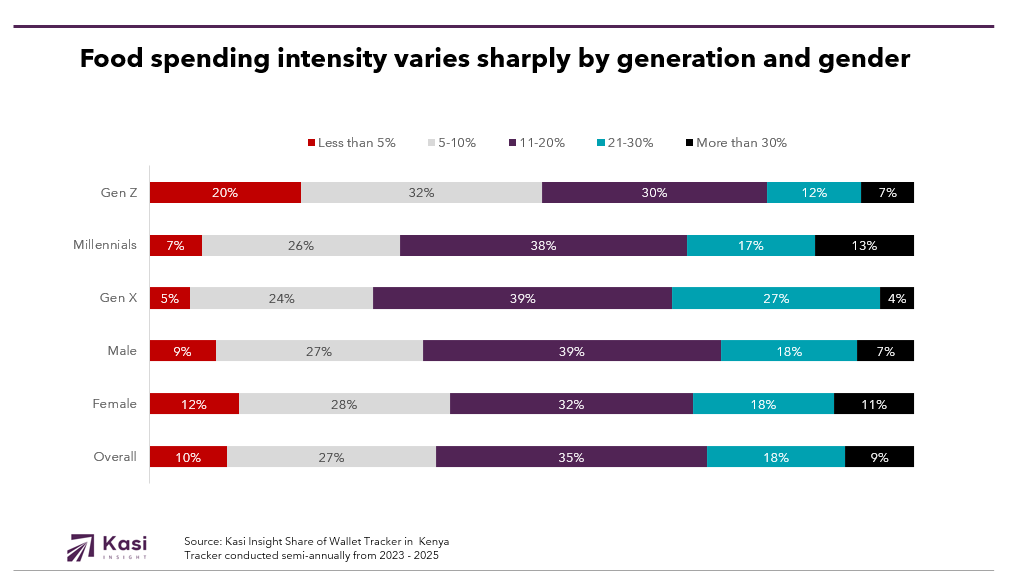

Food continues to occupy a significant share of monthly household budgets. In Q1 2025, 35% of consumers said they spend between 11% and 20% of their income on food and beverages. Another 18% said their spending falls between 21% and 30%. Among Millennials, 13% now spend more than 30% of their income on food, a sharp contrast to only 4% of Gen X.

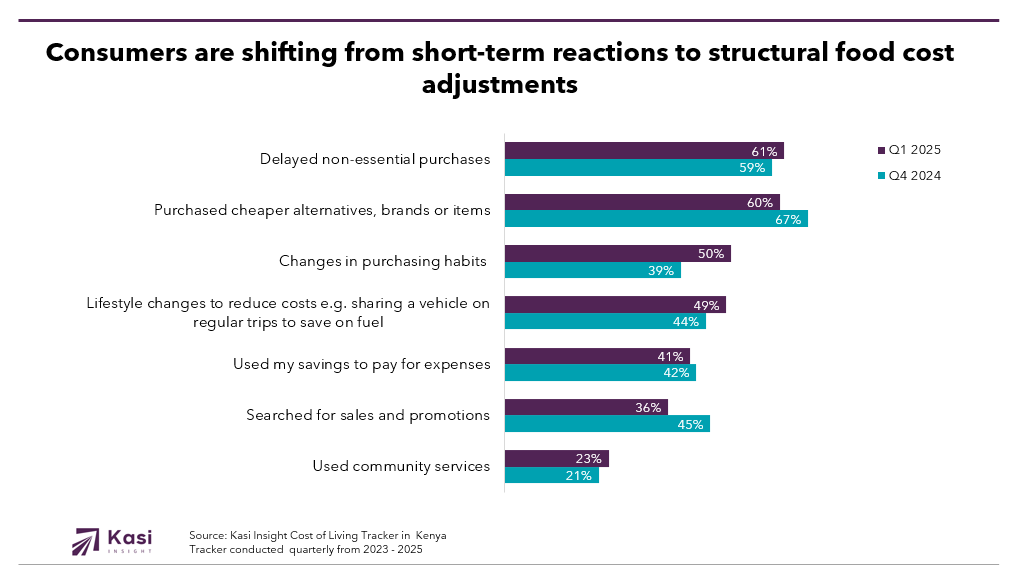

Despite this financial commitment, spending is under increasing scrutiny. In both Q4 2024 and Q1 2025, 80% of respondents reported that food prices had increased. Only 3% said prices had gone down. This sustained cost pressure has shifted food decisions from habitual to intentional. Shoppers are evaluating not just how much they spend but how far that spend can stretch. Portions are adjusted, frequency is reduced, and every item in the basket must justify its value.

Price sensitivity is only the beginning. In Q1 2025, 60% of consumers said they were purchasing cheaper brands or product alternatives. However, the adjustment goes deeper than brand choice. Half of all respondents reported reducing their overall consumption of certain foods. This includes eating out less often, limiting meat or snack purchases, and eliminating non-essential categories altogether.

Another 49% said they had made lifestyle changes to lower food costs. This includes walking to nearby markets instead of using transport or switching from formal supermarkets to informal vendors. These behaviors reflect a new kind of control. People are not just reacting to price hikes. They are designing new systems of consumption that align with their income realities.

The use of sales and promotions has also declined. In Q1 2025, only 36% said they actively searched for offers, compared to 45% in Q4 2024. This suggests that many no longer see discounts as a reliable strategy. Instead, they are building food routines that are simpler, leaner, and easier to maintain.

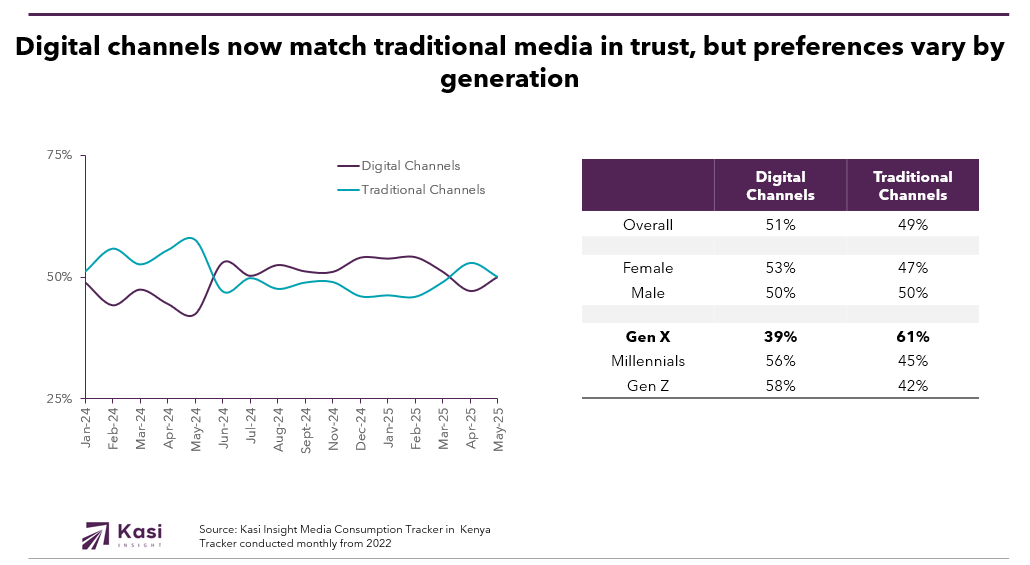

As food spending becomes more deliberate, so does the search for information. Between January and March 2025, 54% of consumers said they trusted digital channels more than traditional ones. In April and May, digital and traditional sources were equally trusted at 50% each. This marks a clear shift in influence, but the picture becomes more nuanced when viewed by generation and gender.

Among Millennials and Gen Z, trust in digital is dominant. In the most recent wave, 56% of Millennials and 58% of Gen Z reported that digital platforms are their most trusted source of information. In contrast, 61% of Gen X continue to place more trust in traditional media such as television and radio. There is also a gender gap, with 53% of women favoring digital channels compared to 50% of men.

Social media platforms, WhatsApp groups, and local food influencers are playing a larger role in shaping perception. Consumers are looking for advice that is grounded in shared experience, not just promotional messaging. Traditional media still has visibility but is no longer the sole source of authority. Trust is now earned through proximity, relevance, and relatability.

Moving to H2 2025, the food and beverage market is no longer defined by aspiration or indulgence. It is shaped by discipline. Households are still dedicating a significant share of their income to food, but they expect more from that spend. What was once a habitual category is now governed by strategy. People are making deliberate choices, refining routines, and applying pressure on brands to deliver value that is tangible, repeatable, and fair.

This shift demands a new approach. Price matters, but not at the expense of trust. Consumers are not asking for more, they are asking for what fits. They want reliable options, honest communication, and products that adapt to their changing consumption rhythms. Format, portioning, and pricing must be designed around planning, not impulse. Brand communication must feel grounded in the same realities consumers face every day.

To succeed in this climate, food and beverage brands must stop assuming relevance and start earning it. The future will not be won by presence alone. It will belong to companies that show up with consistency, operate with empathy, and deliver solutions that feel local, manageable, and built for life under pressure.

Share on socials using this caption: 🍽️ Kenya’s food economy is shifting fast. Households are cutting back, planning smarter, and trusting digital voices more than ever. Brands must meet rising expectations with consistency, empathy, and value that fits. #Kenya2025 #ConsumerTrends #FoodAndBeverage #SmartSpending #ValueDriven #KasiInsight 🛒📊💬

1347 views

Share article

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories

Fresh staples stay strong as Nigeria’s food market splits between value seekers and quality spenders

Ugandans are loyal to beer but wine captures the biggest spend