Sandra Beldine Otieno, MSc

July 17, 2025

Share article

Kasi Insight’s Share of Wallet Tracker provides a view of how consumers allocate their spending across various consumer-facing categories in different African markets. In Q2 2025, the data revealed a changing relationship between Kenyans and alcohol. While overall engagement with the category remains steady, how people drink, what they choose, and how much they spend is shifting. Drinking is no longer a uniform habit but an intentional act shaped by personal values, lifestyle, and occasion. These shifts are not subtle. They are clear signals of a market evolving toward more expressive, controlled, and segmented consumption.

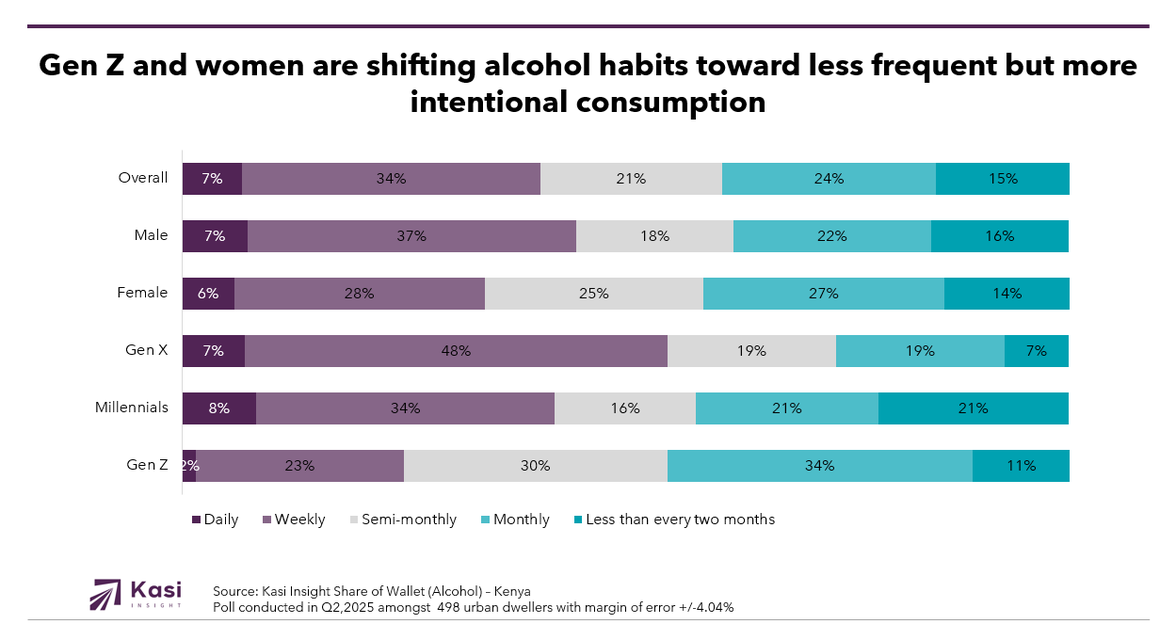

Alcohol is purchased weekly by 34% of Kenyan consumers, making it the most prevalent buying frequency. Another 24% report purchasing monthly and 21% drink semi-monthly. Only 7% of consumers report drinking daily while 15% say they purchase alcohol less often than once every two months. This pattern confirms that alcohol remains part of everyday life, though not excessively. Most consumption is moderate and anchored in rhythm rather than spontaneity.

Digging deeper reveals that this rhythm is not uniform. Gen X stands out as the most regular group, with 48% buying weekly and just 7% drinking less than once every two months. Millennials follow a similar pattern, but Gen Z tells a different story. Only 23% of Gen Z consumers buy weekly while 34% purchase monthly and 30% semi-monthly. This signals a shift toward occasion-based or socially curated consumption. Gender trends show a similar divide. While 37% of men buy alcohol weekly, only 28% of women do. Women lean more toward monthly and semi-monthly purchasing, suggesting a more selective and deliberate relationship with alcohol. Together, these groups are redefining alcohol as a conscious choice rather than a habitual reflex.

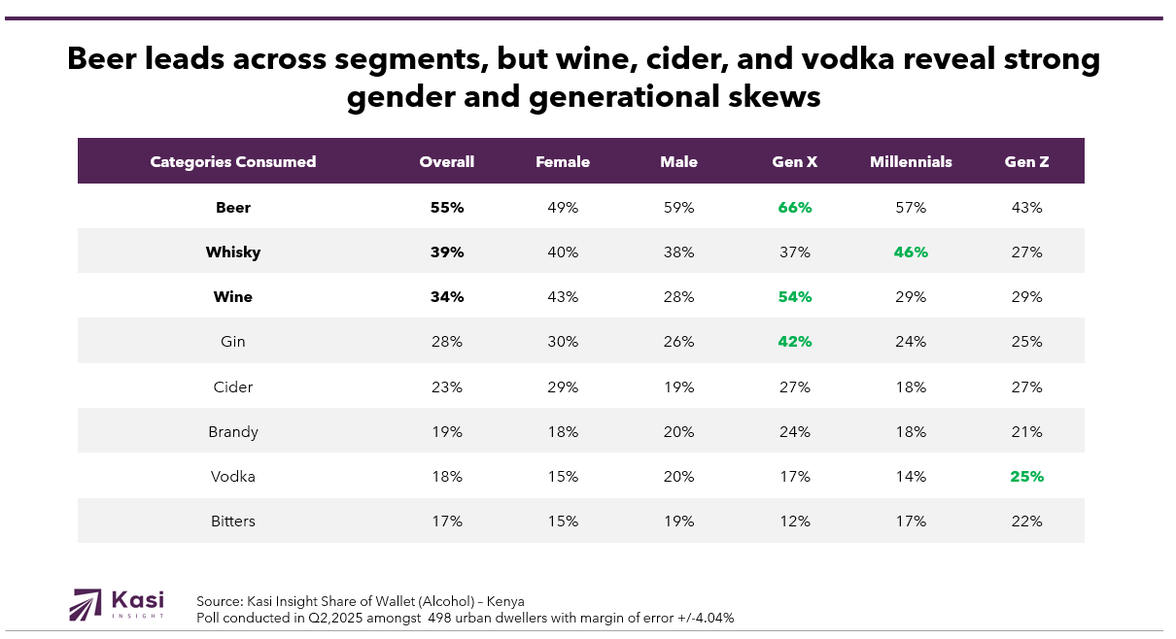

Beer continues to be the most consumed alcohol category in Kenya, with 55% of consumers including it in their drinking routine. Whisky follows at 39% and wine at 34%, while other categories like gin at 28%, cider at 23%, brandy at 19%, vodka at 18%, and bitters at 17% round out the market. At first glance, beer’s lead appears unshaken, but the story becomes more dynamic when viewed through the lens of gender and age.

Women are broadening the definition of what alcohol consumption looks like. Wine is consumed by 43% of women compared to 28% of men and cider follows a similar trend with 29% of women drinking it compared to 19% of men. Gin also performs slightly better among women at 30%. Among age groups, Gen X continues to lead in traditional categories with 66% consuming beer and 54% drinking wine. Gen Z, however, is less engaged with beer at just 43% and shows greater interest in vodka at 25% and bitters at 22%. These trends reflect a shift in taste toward flavor-driven and emotionally expressive drinks that support lifestyle identity rather than routine refreshment.

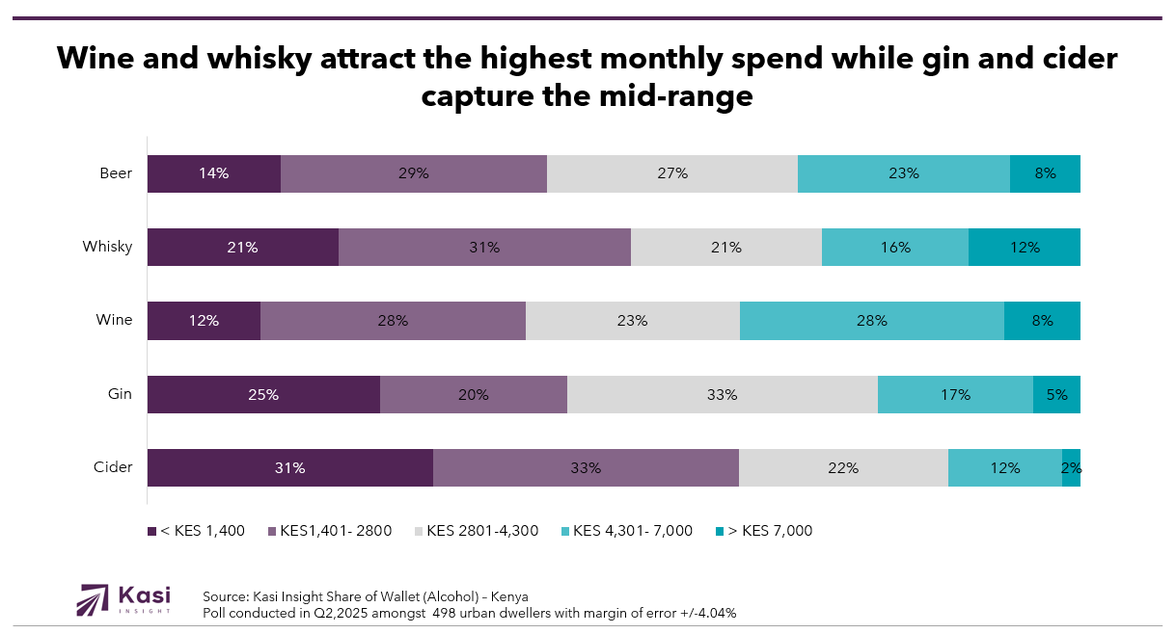

Alcohol spending varies not just by income but by mindset. Cider is the most affordable category, with 31% of drinkers spending less than KES 1,400 monthly and another 33% spending between KES 1,401 and 2,800. Gin spans a wider range, with 25% spending under KES 1,400, 20% between KES 1,401 and 2,800, and 33% spending between KES 2,801 and 4,300. These figures point to gin and cider as accessible, socially shareable drinks that meet consumers in the middle.

In contrast, wine and whisky signal a stronger pull toward premium consumption. Among wine drinkers, 28% spend between KES 4,301 and 7,000 monthly the highest across any category while another 23% spend between KES 2,801 and 4,300. Whisky sees 21% spending in this same middle tier and 12% spending more than KES 7,000 per month. Beer sits between the two extremes, with 29% of consumers spending between KES 1,401 and 2,800 and 27% spending between KES 2,801 and 4,300. These splits confirm a two-speed market. One group leans on affordability and routine while the other seeks indulgence, sophistication, or experience, often anchored in fewer but more meaningful occasions.

The Kenyan alcohol consumer is not walking away from the category. They are simply making sharper and more values-driven decisions. This shift presents an opportunity for brands that are prepared to segment carefully and speak with relevance. Gen X continues to anchor the core market with frequency and scale, but younger consumers and women are shaping the future. These groups may drink less often, but they bring higher expectations, stronger opinions, and greater sensitivity to occasion, taste, and brand purpose.

Brands must adjust their portfolios and messaging to reflect these differences. Wine, cider, vodka, and bitters are rising not just because of flavor but because they align with new moments and new identities. Whether it is socializing, relaxing, celebrating, or self-expression, consumers are asking what the drink says about them. For brands, this is an invitation to innovate. Smaller pack sizes, lighter alcohol content, flavor infusions, and refined design are not just nice to have. They are now expected.

Above all, alcohol brands must move closer to the lives and emotions of the people they serve. This means recognizing that a product consumed weekly may be less influential than one chosen for a special occasion. It means investing in storytelling, relevance, and flexible formats that move with people’s lives. In a market where the drink is no longer the destination but part of a personal journey, the brands that listen and adapt will be the ones that grow.

Share on socials using this caption: 🍷🍺 Kenyans are drinking less often but with more intention. Gen Z and women are driving a shift toward lifestyle-led choices, favoring wine, vodka, and bitters over routine beer. It’s no longer just about what you drink. It’s about why, when, and with whom. #AlcoholTrends #KenyaInsights #KasiInsight #GenZConsumers #SmartDrinking #ShareOfWallet2025

1213 views

Share article

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories

Fresh staples stay strong as Nigeria’s food market splits between value seekers and quality spenders

Ugandans are loyal to beer but wine captures the biggest spend