Sandra Beldine Otieno, MSc

April 11, 2025

Share article

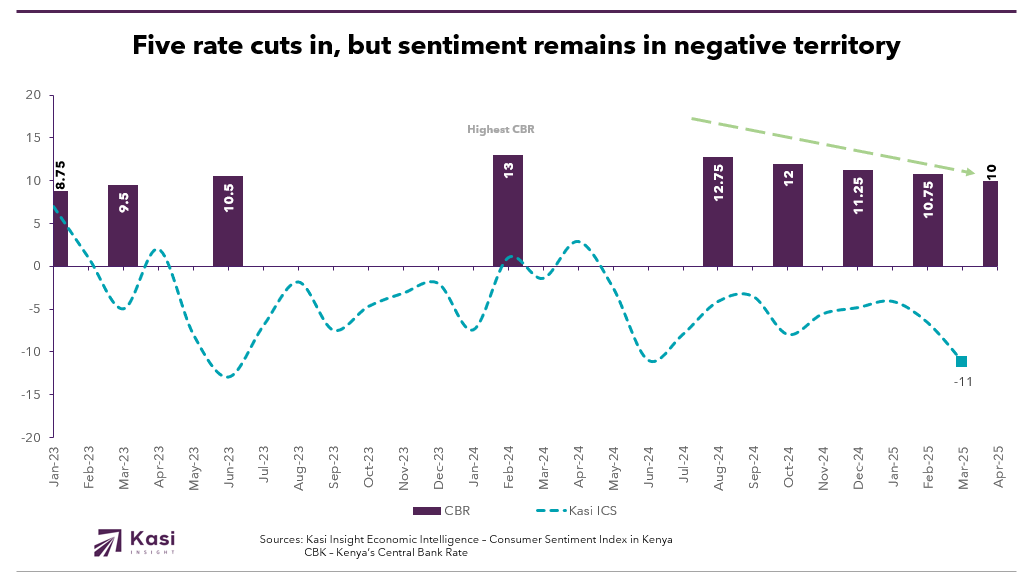

On April 8, 2025, the Central Bank of Kenya (CBK) reduced its policy rate by 75 basis points to 10.00 percent. It was the fifth consecutive cut since August 2024. The decision was positioned as part of a broader effort to stimulate private sector lending and revive economic activity. But the context surrounding the move tells a different story. The MPC is not cutting because confidence has returned, but because confidence remains low. The macroeconomic outlook is still fragile. Private investment is tepid, and consumer sentiment remains weak. The current easing path is necessary, but it is not yet sufficient. Kenya’s central bank may need to go further, faster, and rethink how monetary policy reaches the ground.

Between November 2022 and February 2024, the CBK raised the Central Bank Rate from 8.25% to 13.00% to contain inflation and defend the currency. This was one of the most aggressive monetary tightening cycles in Kenya’s recent history. It helped stabilize macro indicators but came at a steep cost. Lending rates rose above 17% by the end of 2023, pricing many consumers and businesses out of the credit market. Household spending contracted, and private sector credit growth stalled.

By mid-2024, inflation had eased, and the exchange rate stabilized. With external pressures receding, the CBK began to shift. Rate cuts followed in August (12.75%), October (12.00%), December (11.25%), February (10.75%), and now April (10.00%). These actions also included narrowing the interest rate corridor and adjusting the discount window to better align with market pricing. Inflation expectations had improved significantly, reaching 3.6% in March 2025.

But even after a cumulative 300 basis point reduction in the policy rate, credit conditions remain tight, and the intended stimulus has yet to materialize. The CBK has changed direction, but the speed and depth of the adjustment remain insufficient to fully revive activity.

Kasi Insight’s Index of Consumer Sentiment (ICS), which tracks household economic confidence each month, consistently shows that monetary easing has yet to reach the public. In January 2023, the ICS stood at +7. But confidence deteriorated quickly. The index dropped to +1 in February, then to -5 in March and -8 in May. By June 2023, it had reached -13, the lowest point in the 24-month cycle.

The second half of 2023 offered little relief. The ICS rose slightly to minus 7 in July and -2 in August but fell again to -7 in September and minus 5 in October. It closed the year at -2 in December, suggesting that even as inflation eased, confidence did not rebound. In January 2024, the ICS stood at -7. In February, it reached +1, a brief and shallow improvement before falling again to -1 in March and -11 in June.

In the second half of 2024, sentiment remained volatile. The ICS registered -8 in July, -4 in August, -8 in October, and -6 in November. By January 2025, it was at minus 4. In February it declined to -7 and in March 2025 it fell again to -11. This latest reading came even as average commercial lending rates dropped from 17.2% in November 2024 to 15.8% by March 2025. The persistence of weak sentiment despite falling interest rates suggests that the effects of monetary easing have not yet reached consumers.

The problem is not that the CBK is easing too slowly. The problem is that its actions are not being transmitted effectively. In Kenya, banks do not automatically adjust lending rates after a policy cut. Most wait for extended periods, and even then, may only make partial adjustments. Many loans are fixed-rate or repriced infrequently. Even borrowers on variable terms only benefit if their lenders actively reset the terms of their loans, which is not always guaranteed.

Only new borrowers or refinanced loans reflect the new benchmark rates. But refinancing is often out of reach for highly leveraged households and small businesses. Many are unable to meet collateral requirements, or do not qualify under current credit scoring models. Others are discouraged by documentation burdens and the complexity of accessing formal credit. As a result, most existing borrowers are locked out of relief.

Loan maturity dynamics also limit the reach of policy. While a portion of consumer and SME loans are structured to roll over within 12 to 36 months, these cycles are staggered. Few borrowers benefit immediately. Some trade finance and working capital facilities may reset in the coming quarters. But unless banks adopt faster repricing frameworks or are pushed to act, the monetary easing will remain contained at the institutional level.

CBK has taken important steps to support the economy, but the response has been too gradual to shift expectations or spending behavior. A deeper cut in the policy rate could send a clearer signal, prompt faster adjustments in lending markets, and force greater alignment across the banking system. With inflation well within target and credit growth lagging, the CBK still has room to act more decisively.

At the same time, Kenya must improve how policy is delivered. Faster loan repricing, more flexible refinancing terms, and improved bank responsiveness are essential to ensuring that monetary policy reaches borrowers. Without these changes, easing will remain a paper exercise, disconnected from real outcomes. Structural fixes are just as important as interest rate levels.

The CBK has made the right pivot. But if the goal is to restore demand and rebuild economic confidence, this is not the time for caution. The case for a lower rate is well supported by data, and the urgency to fix transmission is mounting. Until households feel tangible relief and borrowing conditions ease, confidence will remain fragile, and the real economy will continue to fall short of policy goals.

Share on socials using this caption: Kenya’s Central Bank has cut rates five times to revive the economy, but credit remains tight, and confidence is low. The easing must go deeper and reach further to make a real impact. 🇰🇪📉💸 #KenyaEconomy #CBK #InterestRates #ConsumerConfidence #MonetaryPolicy

1883 views

Share article

A Strategic Material for Development Sustainable Roads in Africa

Foresight Is No Longer Optional: Why Africa’s Decision Makers Must Move From Insight to Intelligence

Africa’s Data Dilemma: Waiting for the Porsche While Refusing the Bicycle