Sandra Beldine Otieno, MSc

August 19, 2025

Share article

Kasi Insight’s home ownership survey explores whether consumers across African markets aspire to own homes and the steps they are taking to achieve this goal. In Kenya, the desire to own property is evident across all age groups, but Millennials and Gen Z encounter significantly greater financial and structural barriers than Gen X. These challenges are forcing younger Kenyans to pursue slower or less conventional routes to ownership.

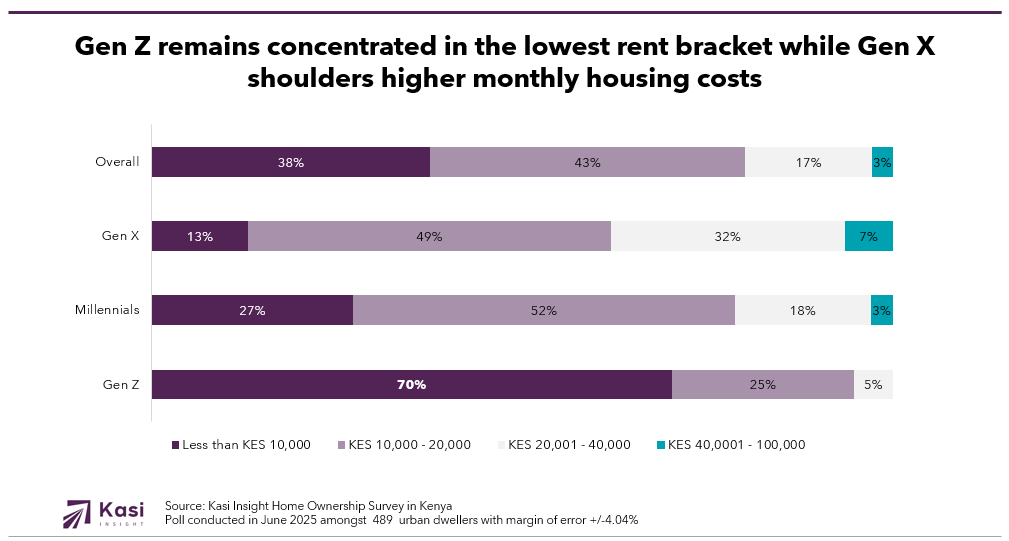

Rent patterns show younger Kenyans concentrated in the lowest cost brackets while older generations spend more on housing

Rent expenditure reveals a distinct divide between generations. Across Kenya, 38% of residents pay less than KES 10,000 per month, but this category is dominated by Gen Z, where 70% fall into the lowest bracket. Millennials and Gen X are far more likely to spend between KES 10,000 and 20,000, with 52% of Millennials and 49% of Gen X in this range. At the upper mid-range, 32% of Gen X pay between KES 20,001 and 40,000, compared to just 5% of Gen Z.

These differences reflect disparities in earnings, household sizes and housing preferences. For younger Kenyans, lower rent commitments reduce short-term financial pressure but may limit their ability to adjust to higher monthly costs such as mortgage repayments. For older generations, higher rents often correspond with established careers, larger households and a greater willingness to invest in better quality housing.

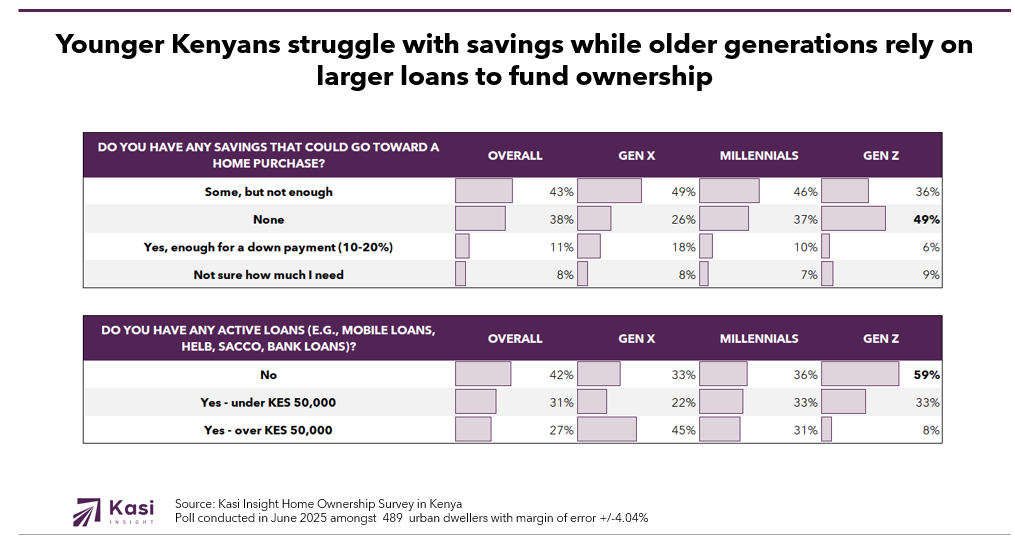

Savings shortfalls and borrowing capacity determine who is ready to buy a home

The ability to save for a deposit remains the most significant barrier to home ownership. Nationally, 43% of Kenyans have some savings but not enough for a purchase, while 38% have no savings at all. The challenge is most severe for Gen Z, where 49% have no savings, compared to 26% of Gen X. Only 6% of Gen Z have enough saved for a down payment, far behind the 18% of Gen X. Millennials are in between, with 37% reporting no savings and 10% ready to make a purchase.

Debt levels add another layer to the readiness gap. Overall, 42% of Kenyans have no active loans, a figure that rises to 59% for Gen Z. While this appears positive, it often reflects limited access to substantial credit rather than stronger financial health. Only 8% of Gen Z hold loans above KES 50,000, compared to 45% of Gen X who have greater borrowing capacity built over time. Among Millennials, 33% hold smaller debts under KES 50,000 and 31% carry larger loans that compete directly with their ability to save.

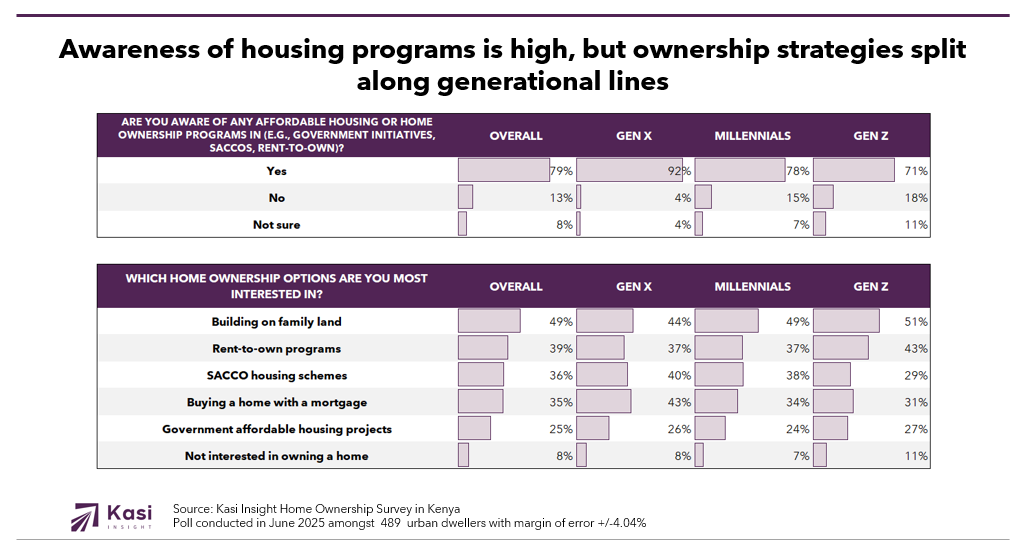

Awareness of ownership programs and choice of strategies reflect different paths to the same goal

The country records high awareness of affordable housing initiatives, with 79% of respondents familiar with government housing schemes, SACCO developments and rent-to-own arrangements. Awareness peaks among Gen X at 92%, falls to 78% for Millennials and drops to 71% for Gen Z. This gap is important because understanding available options often determines whether potential buyers take concrete steps toward ownership.

Ownership preferences further reveal how generations approach the goal. Building on family land is the most popular option at 49% overall, rising to 51% among Gen Z. Rent-to-own programs appeal strongly to Gen Z, with 43% favoring this route compared to 37% of Millennials and 37% of Gen X. Traditional mortgages are more appealing to Gen X at 43%, compared to 31% of Gen Z. SACCO housing schemes attract 36% of respondents, while 25% express interest in government affordable housing projects.

Closing Kenya’s housing gap will require tailored financing, targeted policy and stronger information access

Kenya’s housing market is increasingly split between those with the financial capacity to buy through conventional means and those who must seek alternative routes. Gen X is better able to enter the property market with mortgages and larger deposits, while Millennials and Gen Z lean toward more flexible and lower-cost solutions that fit their current financial situations. Without deliberate action, this gap could widen, leaving many younger Kenyans locked out of property ownership for years and deepening the generational wealth divide.

Addressing this challenge will require coordinated efforts across policy, finance and development. Policymakers can ease entry by lowering deposit requirements, offering government-backed guarantees and supporting matched savings schemes. Financial institutions can introduce hybrid mortgage products, micro-mortgages and more accessible rent-to-own structures that reflect the realities of younger earners. Developers need to prioritize smaller, well-located and affordable units that respond to actual market demand rather than concentrating on higher-end projects.

Improving access to information is equally critical. Younger Kenyans will only make use of affordable housing programs if they have clear, actionable guidance on eligibility, processes and benefits. Closing this awareness gap is one of the most cost-effective ways to bring more first-time buyers into the market. With the right mix of innovative financing, targeted policy and effective communication, Kenya can unlock a new wave of home ownership that bridges generations, strengthens economic stability and reshapes the housing landscape for decades to come.

Share on socials using this caption: 🏠 Kenya’s housing journey is split by generation: Gen Z pays the lowest rents but lacks savings 💰, while Gen X carries bigger loans yet stands stronger in buying power. Ownership choices diverge family land & rent-to-own for the young, mortgages & SACCOs for the older. #Housing #Kenya #GenZ #Millennials #GenX #RealEstate #AffordableHousing

2865 views

Share article

Equity leads where financial journeys begin, while the greatest opportunity lies in capturing more value as those journeys mature.

The Rise of Behavioral Intelligence in African Investing

The Signal Investors Are Missing in African Equity Markets