Sandra Beldine Otieno

August 25, 2022

Share article

Financial institutions in Nigeria should consider coming up with affordable packages that will ensure that even the low-income earners are able to save for emergencies.

Ideally, what does financial freedom mean to Nigerian consumers? A poll conducted by Kasi Insight in March 2022 identified that majority of the consumers surveyed (44%) believe that financial freedom is being on track to meet financial goals like buying a house or starting a business. They are followed by those who believe that financial freedom is all about being flexible to make lifestyle choices like working less or taking vacations (28%). Only 20% of the consumers surveyed believe that financial freedom is feeling in control about their day-to-day expenses like paying bills, rent and food.

Further, the poll revealed that majority of the Nigerian consumers surveyed are looking to achieve financial freedom. 72% want to achieve financial freedom, 5% are unsure while only 23% are not looking forward to achieving financial freedom. Interestingly, Gen Zers are leading when it comes to their willingness to achieve financial freedom. 92% of Gen Zers want to achieve financial freedom, 79% Baby Boomers, 70% Millennials and 67% Gen Xers.

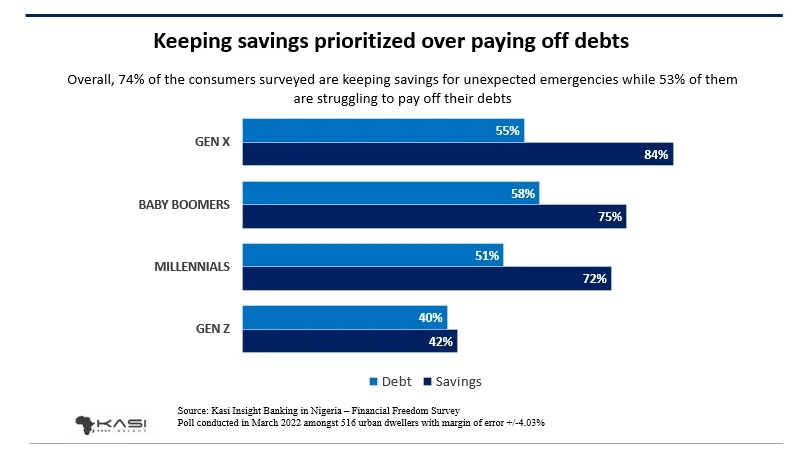

When it comes to whether consumers in Nigeria are able to clear their business, personal and credit card loans, majority of those surveyed (53%) are struggling to pay off their debts while 47% are not. There is a 4% gap between the segments (Males - 54% and females - 50%) indicating that males are struggling to pay off their debts slightly more than females.

Across consumer segments struggling with debt, the older generation is finding it harder compared to the younger ones which is clearly demonstrated by the findings where Baby Boomers are at 58%, Gen Xers at 55%, Millennials 51% and Gen Zers at 40%.

The majority of consumers surveyed (74%) agreed that they have enough savings to cover unexpected events while only 26% did not. Gen Zers are the least prepared for unexpected emergencies at 42% in comparison to Gen Xers 84%, Baby Boomers 75%, Millennials at 72% who have adequate savings to cover such scenarios. Across income levels, the high-income earners are the most prepared to deal with emergencies at 70% while low-income earners are the least prepared to deal with such issues (40%).

Financial institutions in the country, should pay keen attention to consumers’ loan eligibility criteria. For example, though older people may be considered credible to take up loans, they would take these loans and struggle to pay back. In order to guarantee that loans are not defaulted, young people should be allowed to take up loans with strict repayment policies. Additionally, these institutions should consider coming up with affordable packages that will ensure that even the low-income earners are able to save for emergencies.

Our data intelligence platform can provide more insights to help your business make informed decisions in Nigeria and elsewhere in Africa.

Contact our team today to explore how our consumer intelligence can empower your decision-making process. Win with confidence with Kasi insights https://www.kasiinsight.com/thehub

#Nigeria #Savings #Debts #Financialinstitutions #Africa #Kasiinsight

1693 views

Share article

Equity leads where financial journeys begin, while the greatest opportunity lies in capturing more value as those journeys mature.

The Rise of Behavioral Intelligence in African Investing

The Signal Investors Are Missing in African Equity Markets