Yannick Lefang, Eng

April 9, 2026

Share article

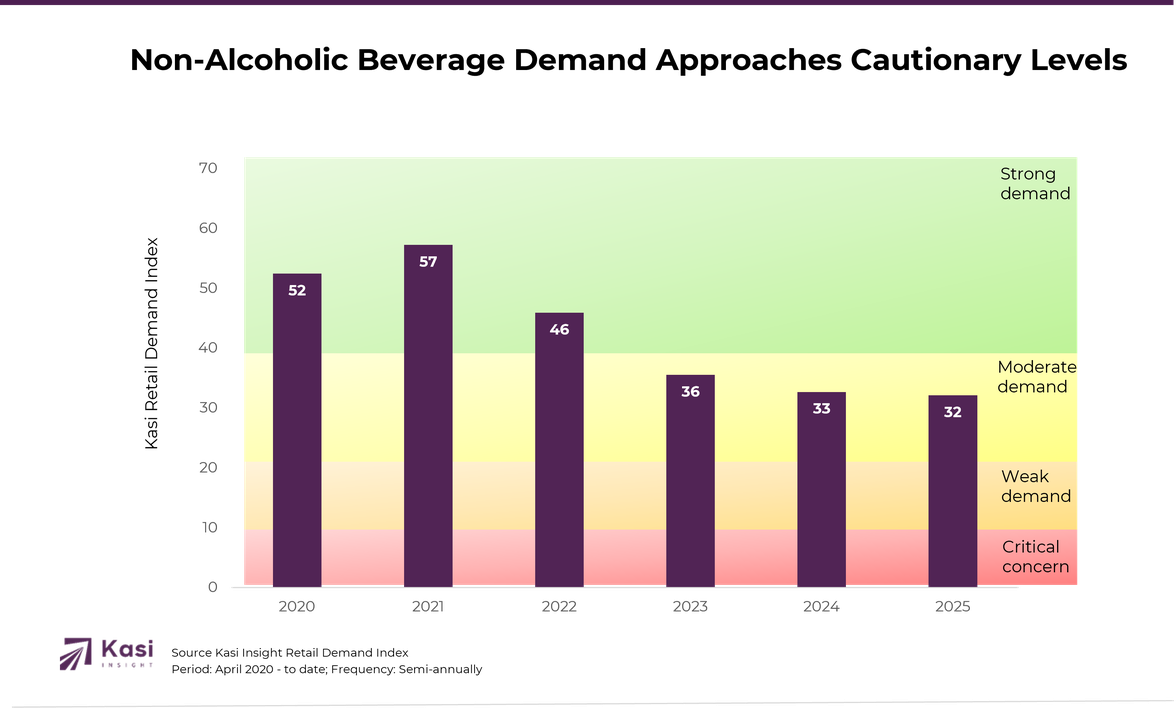

Kasi Insight’s Retail Demand Index (RDI) tracks consumer interest, showing how demand evolves across categories over time. In Beverage Demand, while scores rarely dip below zero, even positive numbers can mask stress in key segments. By integrating thresholds based on real market performance, the Kasi RDI identifies when demand is truly weak. Strong demand is reflected above 40, moderate demand falls between 20 and 40, weak demand is under 20, and levels below 10 signal urgent concern.

Over the past five years, Kenya’s non-alcoholic beverage sector has seen a gradual moderation in demand, driven largely by declines in discretionary categories such as energy drinks, regular soft drinks, diet soft drinks, and some juice segments, while essentials like tea, milk, and bottled water remained resilient. Overall, Kasi RDI scores fell from 52 in 2020 to 32 by 2025.

Tea, milk, and bottled water remain resilient. Tea held Kasi RDI scores above 70 in 2020–2021, dipping slightly to 71.9 by 2025, while milk stayed above 45 and bottled water above 50. These foundational categories continue to anchor consumer demand.

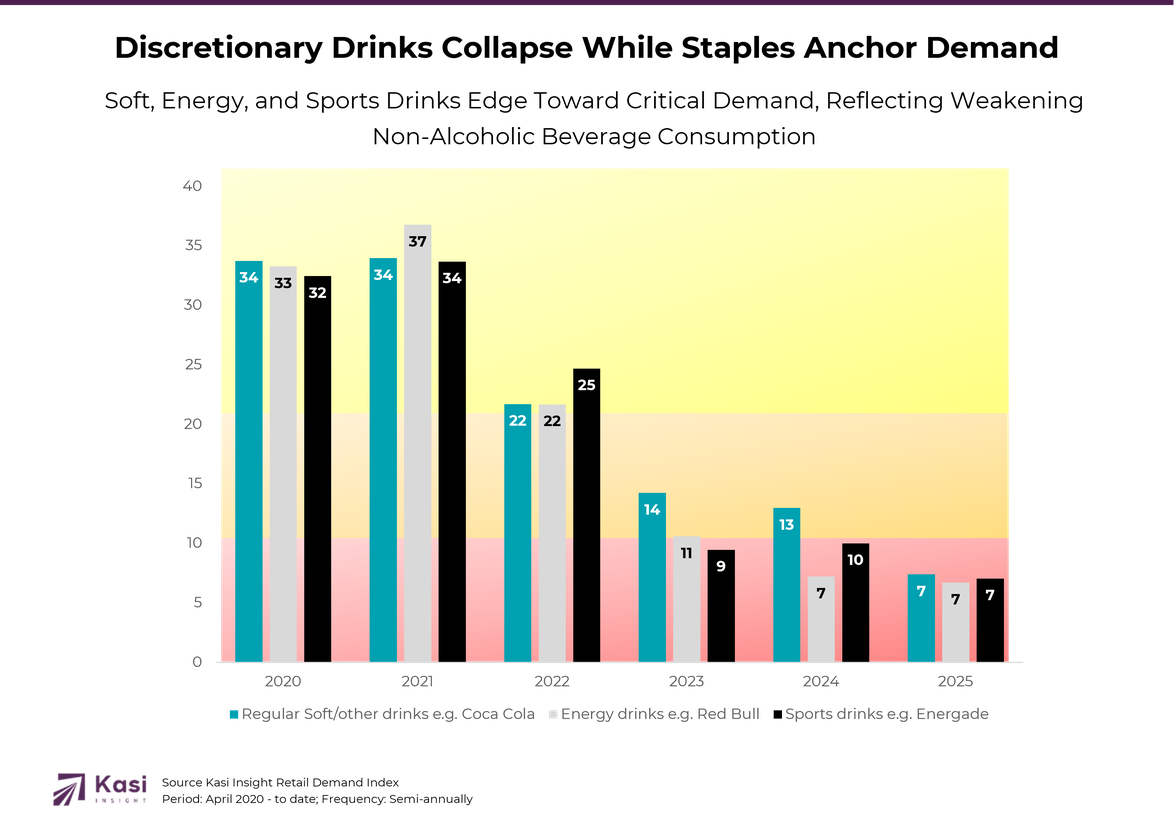

Discretionary segments tell a different story. Energy drinks dropped from 33.3 in 2020 to 6.7 in 2025, regular soft drinks fell from 33.7 to 7.4, and diet soft drinks declined from 36.5 to 15.3. Fruit juice declined from 59.7 to 42.6, slower than the discretionary drinks but still below staple performance. The data highlights a clear consumer pivot: essentials and functional products remain robust, while indulgent or non-essential drinks face meaningful pressure.

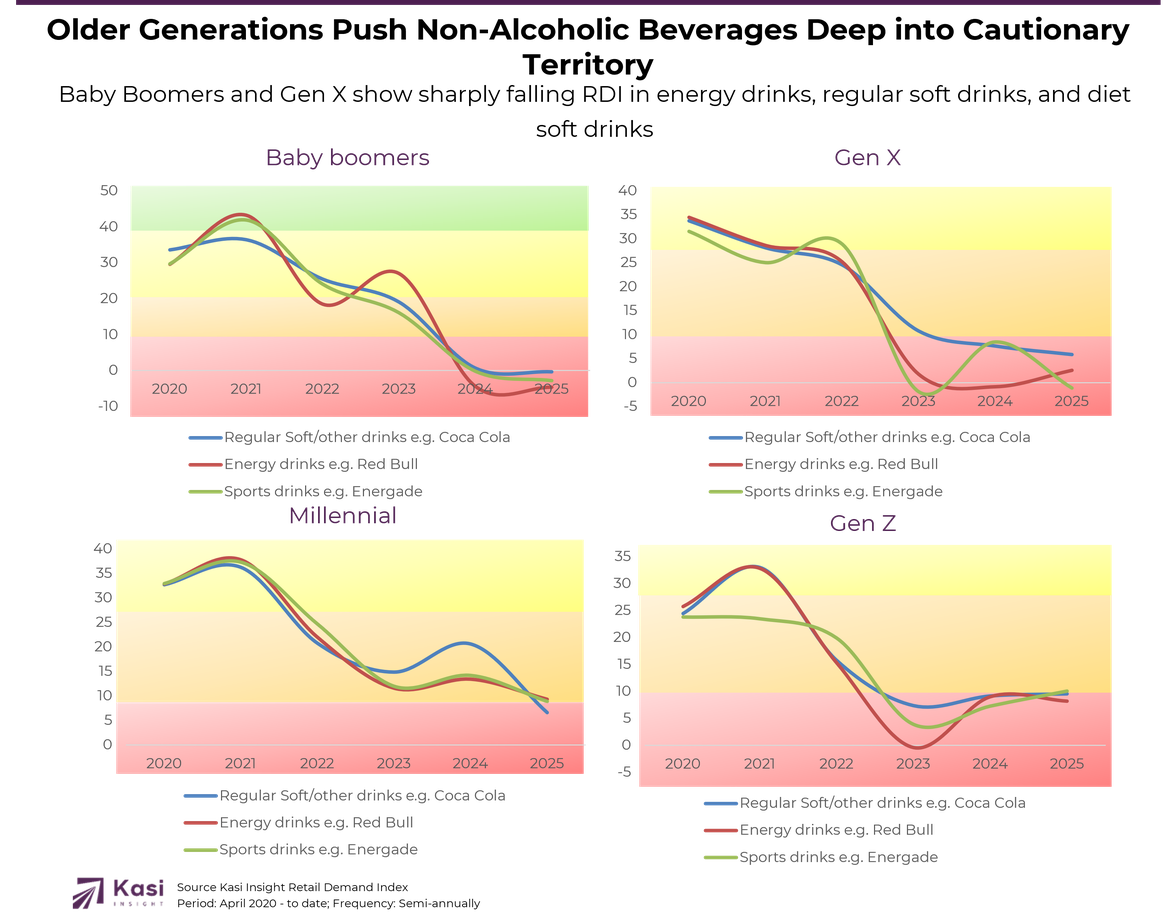

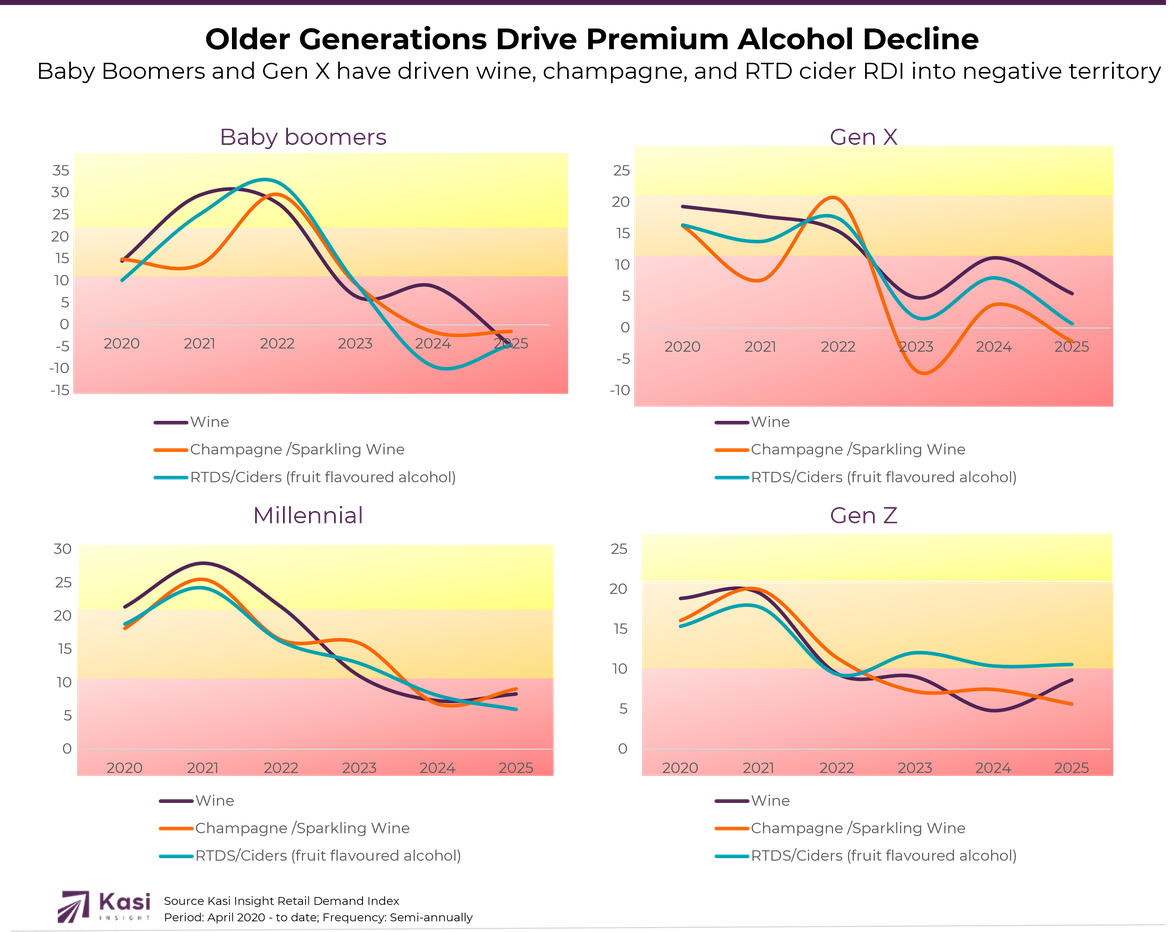

Kasi RDI by consumer segments reveals that older generations, Gen X and Baby Boomers, have been the largest drivers of declining demand in non-alcoholic beverages. Their scores in energy drinks, sports drinks, and regular soft drinks turned negative in recent years, signaling that reduced consumption among these established consumers is a major factor in the overall slowdown.

For brands, strategy should focus on hydration, wellness, and functional products. Bottled water, healthier juices, and ready-to-drink functional beverages show durable consumer engagement. Energy drinks and sugary soft drinks require repositioning, reformulation, or marketing innovations to regain relevance.

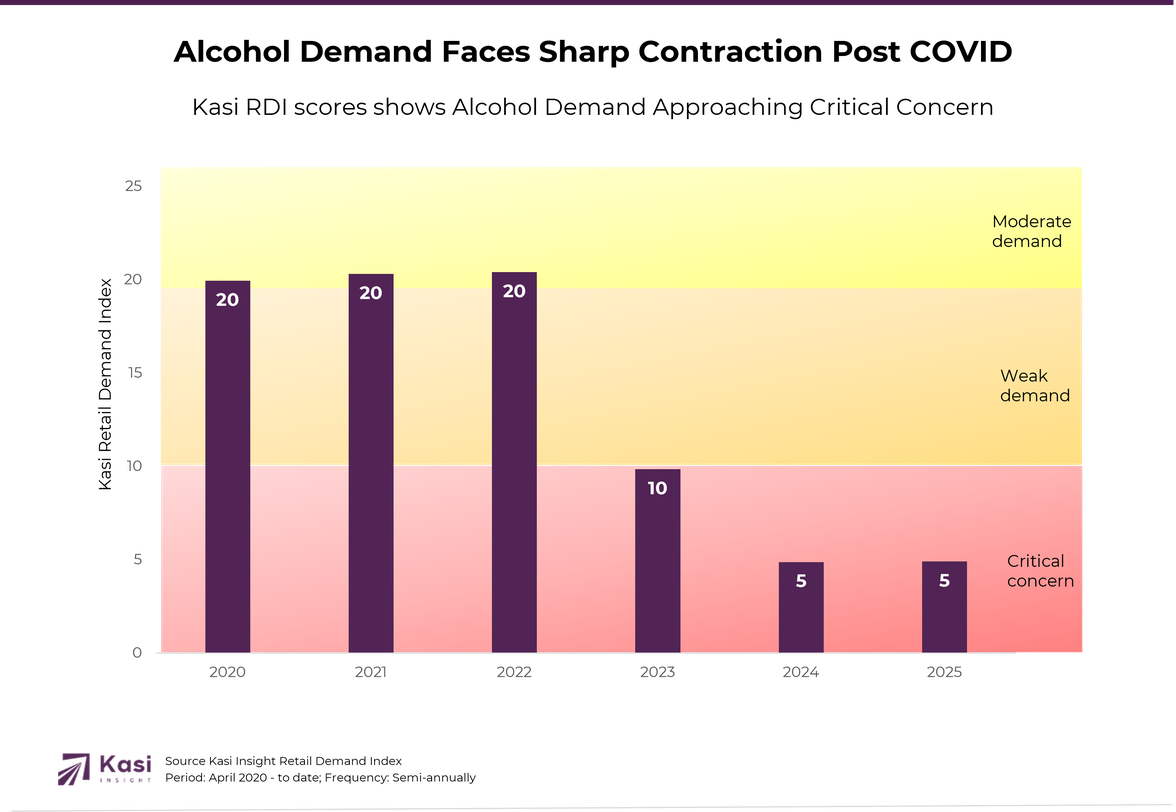

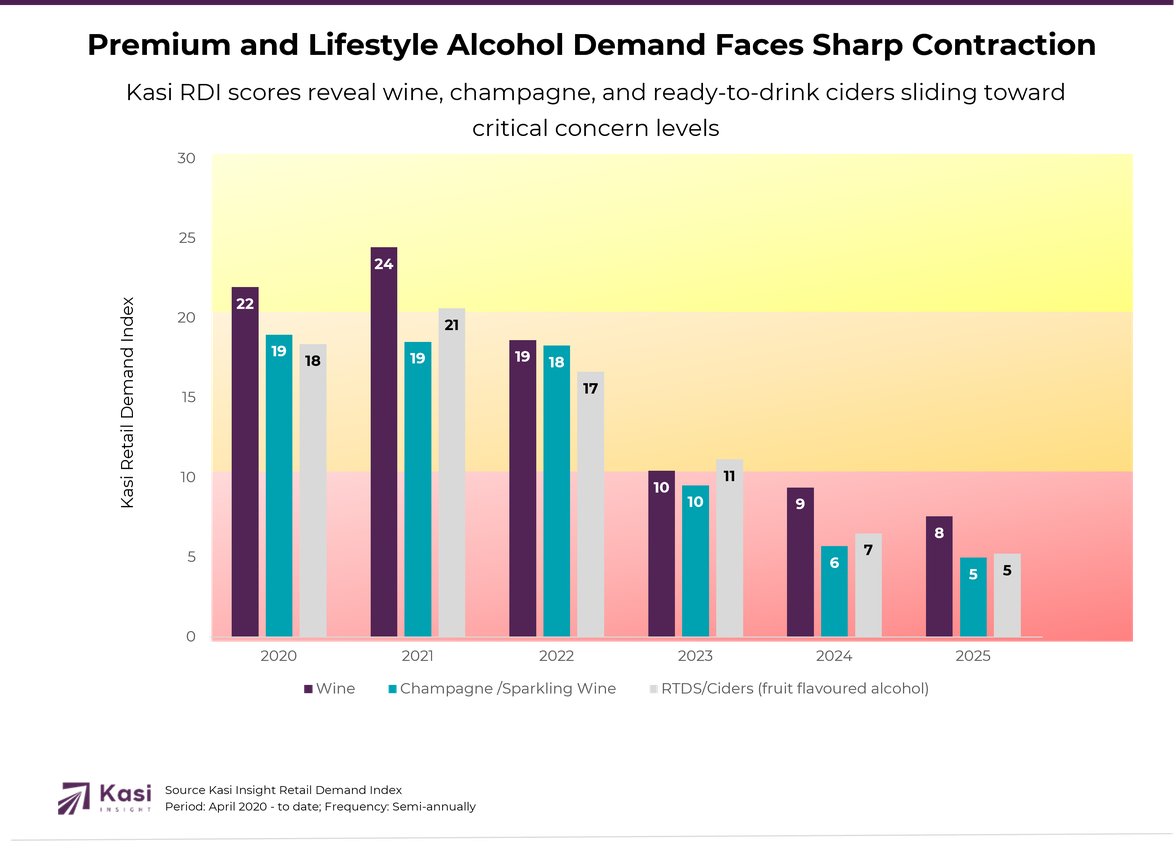

Since the pandemic, overall alcoholic beverage consumption in Kenya has fallen sharply. Total demand dropped from 20 in 2020–2022 to just 5 by 2025. Premium categories took the brunt of this decline: wine fell from 22 to 8, champagne and sparkling wine from 19 to 5, and ready-to-drink ciders from 18 to 5. In contrast, more accessible categories like beer showed comparatively better resilience.

Beer has proven comparatively resilient. Its Kasi RDI remained in positive territory, dropping from 24 in H1 2020 to 7.56 in H1 2025 before rebounding slightly to 10.91 in H2 2025. Premium categories, however, have suffered significantly. Wine fell from 12.18 to 2.16, champagne and sparkling wine declined from 14.1 to 0.77, and ready-to-drink ciders dropped from 11.19 to 1.92. Vodka, whisky, and other spirits mirrored this trend. The data reflects a clear consumer preference for value and social utility over aspirational and luxury products.

Alcoholic beverage brands face a dual reality. Beer remains the backbone of the market, and campaigns that emphasize social occasions, community events, and cultural experiences will resonate. Premium segments require a clear value proposition; aspirational products struggle without strong quality perception or lifestyle alignment. Targeted promotions and experience-led marketing can help mid-priced and premium categories recover, especially among urban and affluent consumers

In Kenya’s alcoholic beverage market, Baby Boomers and Gen X have been the main drivers of decline, with demand for premium categories such as wine, champagne, and RTD ciders falling into negative RDI territory post-COVID. This indicates a sharp pullback in discretionary and aspirational consumption among older consumers, while younger and middle-income groups maintain moderate interest in accessible options like beer. The divergence underscores how generational behavior is reshaping the market, signaling that brands must realign strategies to address both declining older segments and the steady preferences of younger audiences.

By combining Kasi RDI thresholds, actual category data, and broader market research, brands can move beyond reacting to short-term fluctuations. Understanding which products genuinely maintain consumer interest allows for smarter investment, protected market share, and positioning for long-term growth, even amid economic pressures and shifting lifestyle priorities.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

15 views

Share article

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories

Fresh staples stay strong as Nigeria’s food market splits between value seekers and quality spenders

Ugandans are loyal to beer but wine captures the biggest spend