Sandra Beldine Otieno, MSc

June 4, 2025

Share article

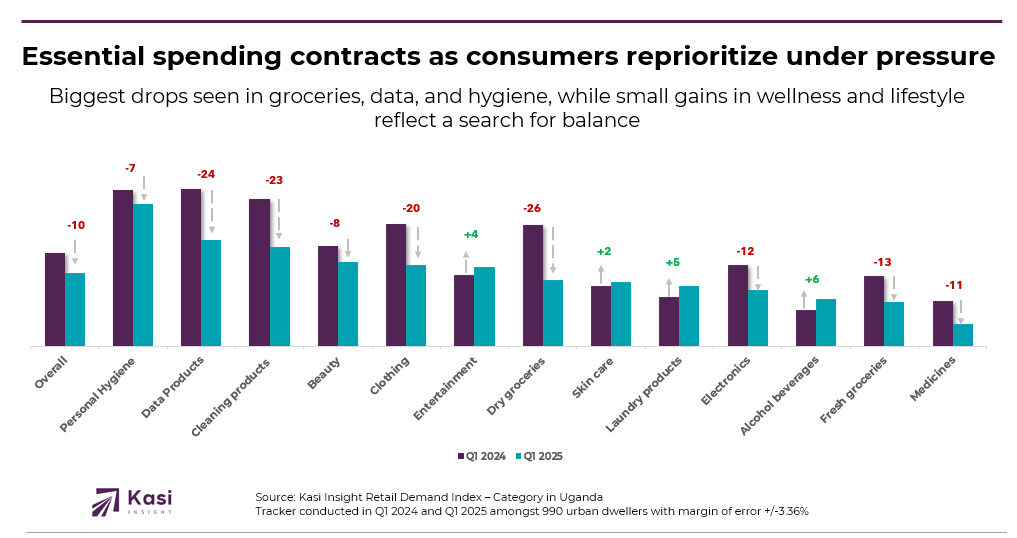

Kasi Insight’s Retail Demand Index (RDI), tracked quarterly, captures how consumer demand is evolving across key consumer facing sectors. Ranging from +100 to -100, the index reflects shifts in consumer interest, with +100 indicating peak demand and strong purchasing intent. As of the first quarter of 2025, Uganda’s retail outlook showed a broad decline in demand, with consumers adjusting their priorities in response to sustained economic pressures.

Year-on-year, the overall category demand index fell from 45 in Q1 2024 to 35 in Q1 2025. This 10-point decline highlights a softening in consumer activity and signals a more cautious approach to spending across both essential and discretionary categories. The most significant declines occurred in daily essentials. Dry groceries dropped by 26 points to an index of 32, indicating a major shift in how households manage food staples. Data products, once among the most resilient segments, fell by 24 points to 51. Cleaning products followed closely with a 23-point drop to 47, reflecting changes in hygiene-related consumption.

Other categories tied to everyday routines also saw marked reductions. Clothing decreased by 20 points to 39, while fresh groceries fell to 21 after a 13-point decline. Medicines dropped by 11 points, and personal hygiene, although still relatively high, declined by 7 points to an index of 68. Together, these shifts reflect a broader reordering of household priorities in response to ongoing cost pressure. Despite the broader slowdown, a few categories showed modest growth. Alcoholic beverages rose by 6 points to 23, and entertainment increased by 4 points to 38, suggesting that even in a constrained environment, consumers continue to seek out small moments of enjoyment and connection.

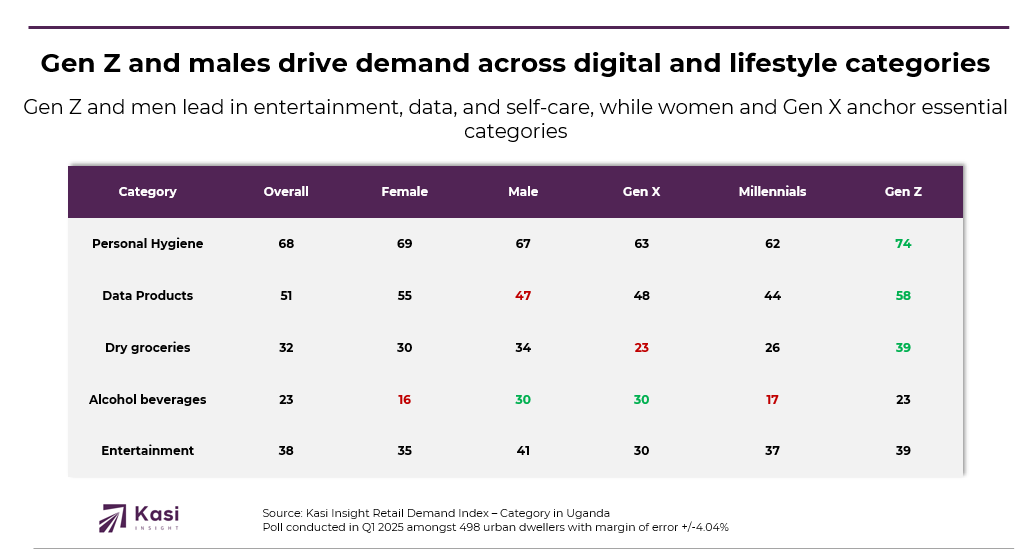

Q1 2025 data also highlights meaningful generational and gender-based differences in consumer behavior, particularly across essentials and discretionary categories. While female consumers maintained strong engagement in categories like personal hygiene, where they scored 69 on the index, Gen Z outperformed across several segments, highlighting their growing influence in shaping retail demand.

In essentials, Gen Z led demand for personal hygiene with a score of 74, reinforcing their continued attention to wellness and daily care. They also recorded the highest demand for dry groceries at 39, ahead of Gen X and millennial segments, suggesting that younger consumers are actively participating in household provisioning. Interestingly, male consumers showed slightly higher demand than females in dry groceries and significantly higher scores in alcoholic beverages and entertainment, pointing to shifting gender roles in spending patterns.

Discretionary categories were led by male consumers and Gen Z. Males topped entertainment demand at 41, followed closely by Gen Z at 39 and millennials at 37. A similar trend appeared in alcoholic beverages, where males and Gen X each scored 30, ahead of their female and younger peers. Data products followed the same generational gradient, with Gen Z leading at 58, followed by female consumers at 55, reinforcing the strong role of youth in sustaining digital consumption.

Uganda’s shifting retail landscape calls for a renewed understanding of consumer intent. The broad decline in category-level demand reflects not disengagement but a deliberate move toward prioritizing what truly matters. Brands operating in essential categories such as dry groceries, cleaning products, and personal hygiene must respond with accessible value. Consumers are stretching their budgets carefully, and product formats, pricing, and availability must reflect this new reality. Trust and consistency remain critical for retaining relevance in these everyday routines.

Beyond essentials, pockets of growth in entertainment, alcohol, and personal care show that consumers are still seeking balance and joy. These categories represent small but meaningful expressions of lifestyle and self-preservation, even in constrained conditions. Brands that offer experiences, comfort, and affordable indulgence stand to connect more deeply with consumers looking for moments of relief. Creative campaigns that celebrate community, routine, and optimism can inspire loyalty and spark renewed engagement.

Shifting generational and gender dynamics unlock new growth paths for brands. Gen Z is actively shaping demand across essentials and digital products, while male consumers are shaping demand in entertainment and social categories. This signals a shift in influence that requires more targeted brand communication. Strategies must be informed by who is spending, what they value, and how they want to be reached. Brands that stay agile, read these signals clearly, and respond with relevance and empathy will find space to grow even as the broader market resets.

Share on socials using this caption: Ugandans are spending less on basics but still investing in wellness, entertainment, and self-care 💆♀️🎮. Gen Z and men are driving demand shifts in 2025, are brands ready to adapt? #ConsumerTrends #RetailInsights #Uganda2025 #GenZ #KasiInsight #BrandStrategy

1515 views

Share article

Kenyan consumers are shifting from survival to intentional living reshaping value wellness and brand responsibility

Inflation fatigue is deepening financial stress for consumers in Ivory Coast

Cameroonians appetite for staples and fresh produce grows while demand for proteins dips