Yannick Lefang, Eng

April 2, 2026

Share article

In banking, strategy is often revealed too late, through earnings, asset growth, or shifts in capital allocation. In Uganda in 2025, however, the signal emerged earlier and more visibly through marketing.

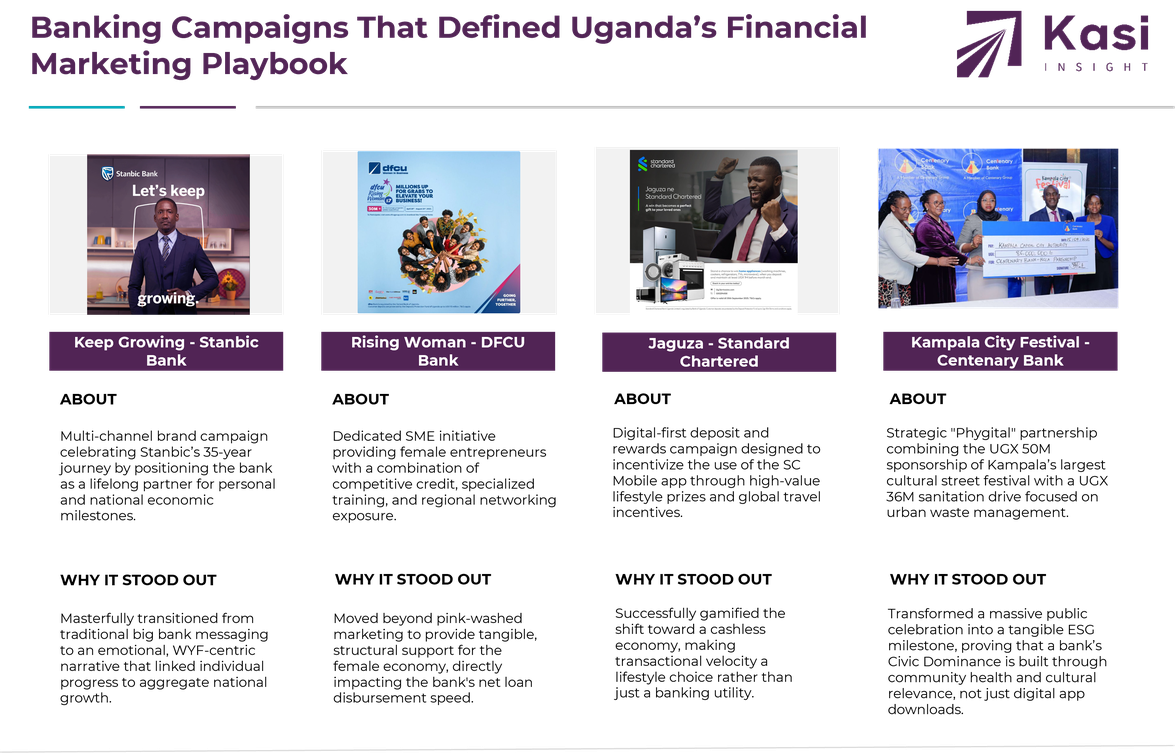

Across the sector, a consistent pattern can be observed. Banks were not retreating from growth, nor were they aggressively expanding risk. Instead, they were pursuing a more calibrated approach: strengthening deposit franchises, increasing transaction monetization, and expanding credit selectively within defined segments. Marketing campaigns: spanning cards, women entrepreneurship, salary accounts, and community sponsorships, offer a clear window into this strategy. A prime example was Stanbic Bank’s Keep Growing Campaign targeting the WYF Agenda (Women, Youth, and Farmers). It combined financial products with the "Stanbic Business Incubator" to provide investment-ready skills.

Unlike Kenya’s more defensive posture in the same period, Uganda’s banking system in 2025 appears to have entered a measured expansion phase, characterized by disciplined lending, improving asset quality, and a renewed focus on customer engagement as a driver of long-term profitability.

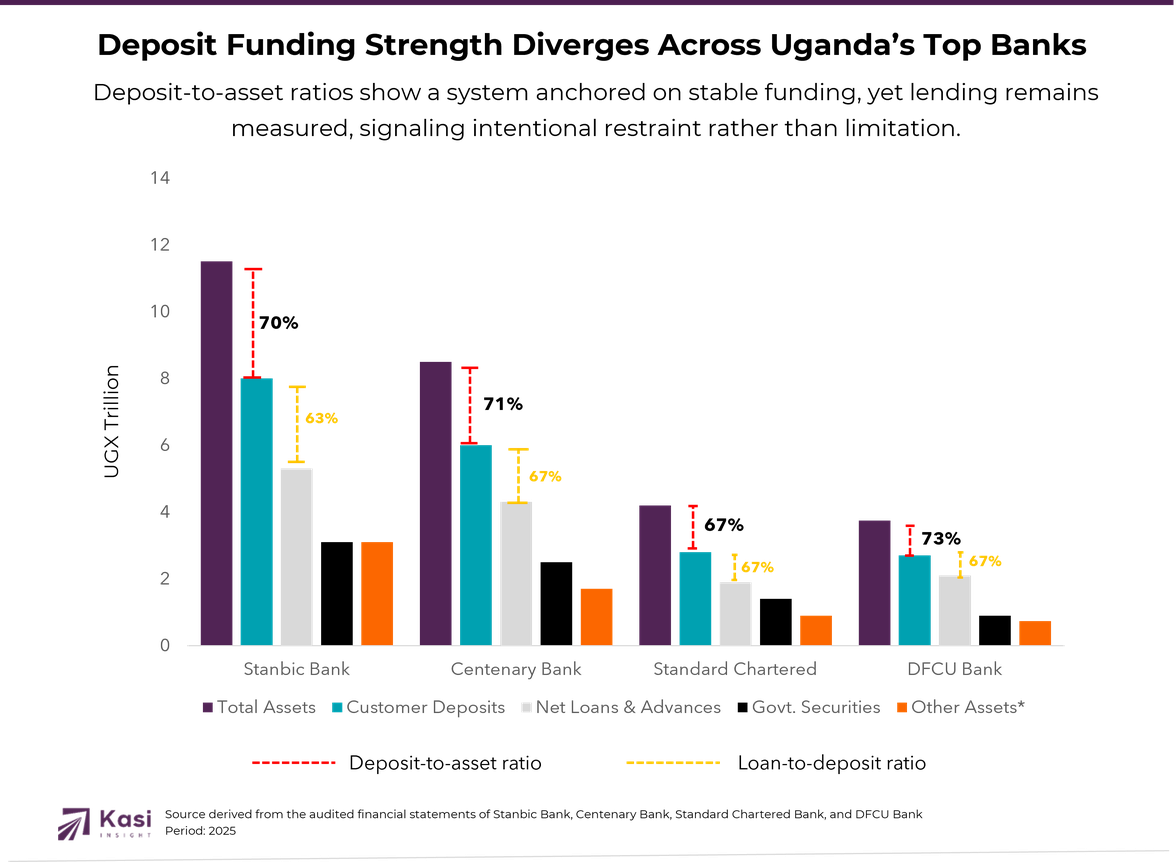

The macro-financial backdrop provides important context. Sector lending in Uganda showed moderate but steady growth through 2025, while non-performing loans improved, indicating a gradual normalization of credit conditions. At the same time, deposits expanded strongly, and profitability was supported not only by lending but also by interest income from government securities.

This combination is significant. It suggests that banks were not constrained to the same extent as in more defensive markets. Instead, they had the flexibility to grow, albeit cautiously, while maintaining a focus on risk-adjusted returns. Standard Chartered’s "Jaguza Ne Standard Chartered" promotion underscored this focus on liquidity, requiring significant "fresh fund" deposits for entry to ensure the bank’s growth was funded by stable, low-cost capital.

In such an environment, the objective is not simply to preserve capital, but to deploy it intelligently. Marketing behavior in 2025 reflects precisely this mindset.

A defining feature of Uganda’s 2025 banking landscape was the strong emphasis on payments and transaction activity. Card campaigns—particularly those linked to international schemes such as Visa—were prominent across multiple banks. These campaigns incentivized everyday spending, cross-border transactions, and digital usage, positioning banks not just as custodians of funds, but as enablers of financial activity.

This is a critical shift. In a mature banking model, revenue is no longer derived solely from lending. Instead, it is increasingly driven by the frequency and diversity of customer transactions. By encouraging card usage and digital engagement, banks were effectively expanding their non-interest income base while deepening customer relationships.

At the same time, segment-led campaigns became more pronounced. Women entrepreneurs, small and medium-sized enterprises, salary earners, and emerging middle-class households were all targeted through tailored propositions. Initiatives focused on women-led businesses, for example, combined financing with mentorship, networking, and visibility—blending commercial objectives with long-term relationship building. The "Rising Woman" initiative by DFCU Bank serves as a strategic marker here, as it moved beyond simple credit by offering mentorship and networking to de-risk the lending process for female-led SMEs

This approach reflects a more sophisticated view of growth. Rather than expanding credit indiscriminately, banks are constructing portfolios around segments that offer both scale and resilience.

These marketing signals translate directly into balance sheet strategy.

First, deposit growth remains foundational. Campaigns centered on salary accounts, savings, and financial empowerment indicate that banks are prioritizing stable, low-cost funding. This is not merely a defensive move; it is a prerequisite for sustainable expansion. A strong deposit base provides both liquidity and pricing flexibility, enabling banks to compete more effectively as lending opportunities emerge.

Second, credit growth is present, but selective. The absence of mass-market loan campaigns, combined with targeted initiatives for specific segments, suggests that banks are expanding their loan books with discipline. This aligns with the observed improvement in asset quality and indicates a deliberate effort to avoid the excesses of previous credit cycles.

Third, transaction monetization has become a central pillar of the business model. Card campaigns, merchant partnerships, and digital banking initiatives all point to a strategic shift toward capturing value from customer activity rather than solely from balance sheet exposure. In effect, banks are moving from a model based on “stock” (loans and deposits) to one that also emphasizes “flow” (transactions and usage).

Finally, the continued prominence of offline sponsorships and community engagement underscores the importance of trust and distribution in the Ugandan market. Sponsorship of cultural events, sports tournaments, and national platforms serves not only to enhance brand visibility but also to strengthen customer acquisition pipelines and reinforce credibility in a relationship-driven environment. Centenary Bank’s headline sponsorship of the Kampala City Festival highlighted this commitment to physical presence, using the "Weyonje" waste-management initiative to anchor the brand in the daily lives and values of urban consumers.

The Ugandan banking sector in 2025 can be understood as optimizing a slightly different equation from more defensive markets.

Profitability is being driven by a combination of deposit growth, selective loan expansion, transaction-based income, and continued participation in government securities, balanced carefully against credit risk.

Unlike purely defensive systems, where lending is subdued, Uganda’s model retains lending as an active, though controlled, contributor to growth. This creates a more balanced and potentially more resilient earnings profile.

What distinguishes Uganda in 2025 is not the presence of growth, but the discipline with which that growth is pursued.

Banks are simultaneously:

This multi-pronged approach reflects a sector that has learned from previous cycles. Growth is no longer pursued at the expense of asset quality; instead, it is built on a foundation of strong funding, diversified income streams, and careful risk management.

If current trends persist, the next phase for Uganda’s banking sector is likely to be one of gradual acceleration.

As macro conditions stabilize further and credit demand strengthens, banks will be positioned to scale lending more confidently. The groundwork laid in 2025—strong deposits, deepened customer relationships, and improved asset quality—will enable a smoother transition into a more expansionary phase.

Importantly, when this shift occurs, it will again be visible first in marketing. Campaigns will begin to emphasize credit products more explicitly, particularly in SME and consumer segments. Digital lending platforms may gain greater prominence, and competitive intensity around loan acquisition is likely to increase.

For investors, Uganda presents a compelling narrative of balanced growth. Banks are not only profitable but are also building the structural capacity for sustained expansion. The combination of improving asset quality, strong deposit growth, and diversified revenue streams suggests a sector with both stability and upside potential.

For policymakers, the alignment between commercial strategies and financial inclusion objectives is notable. The focus on women entrepreneurs, SMEs, and underserved segments indicates that banks are playing an active role in broadening access to financial services.

From a Kasi standpoint, the most important takeaway is that marketing once again serves as a leading indicator of strategic intent. In Uganda in 2025, that intent is clear: banks are preparing not just to grow, but to grow intelligently. This creates a significant opportunity. As lending expands, the ability to identify creditworthy segments, anticipate demand, and manage risk dynamically will become increasingly valuable. Institutions that can access high-frequency, forward-looking signals will be better equipped to allocate capital effectively and outperform competitors.

The Ugandan banking sector in 2025 is best understood as being in transition—not from growth to caution, but from indiscriminate expansion to disciplined scaling. Marketing campaigns reveal this shift with clarity. They point to a system that is building depth before accelerating, strengthening relationships before expanding risk, and positioning itself for the next phase of the cycle. The sector is not waiting. It is preparing.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

7 views

Share article

Kenya Banking Sector 2025: Reading the Balance Sheet Through Marketing Signals

How Consumer Sentiment Predicts South Africa’s Credit Cycles

How Consumer Sentiment Predicts Kenya’s Credit Cycles