Sandra Beldine Otieno, MSc

June 16, 2025

Share article

As Kenya enters the second half of 2025, the retail banking landscape is being shaped by the uneven recovery from COVID-19 and the shifting expectations of a more informed, financially aware population. The pandemic triggered widespread income shocks, weakened financial control, and exposed deep structural vulnerabilities. In the years that followed, a slow and inconsistent recovery unfolded marked by increased digital engagement and greater financial literacy, but not necessarily improved financial outcomes. While access to financial products has expanded and trust in traditional banks is improving, many Kenyans continue to face income pressure, limited savings, and uncertainty about their long-term financial wellbeing. Data from Kasi Insight’s Banking Brand Intelligence and Financial Freedom Tracker, collected annually since 2021, reveals three powerful consumer shifts that reflect this journey. These shifts signal a clear message to banks: delivering access is no longer enough.

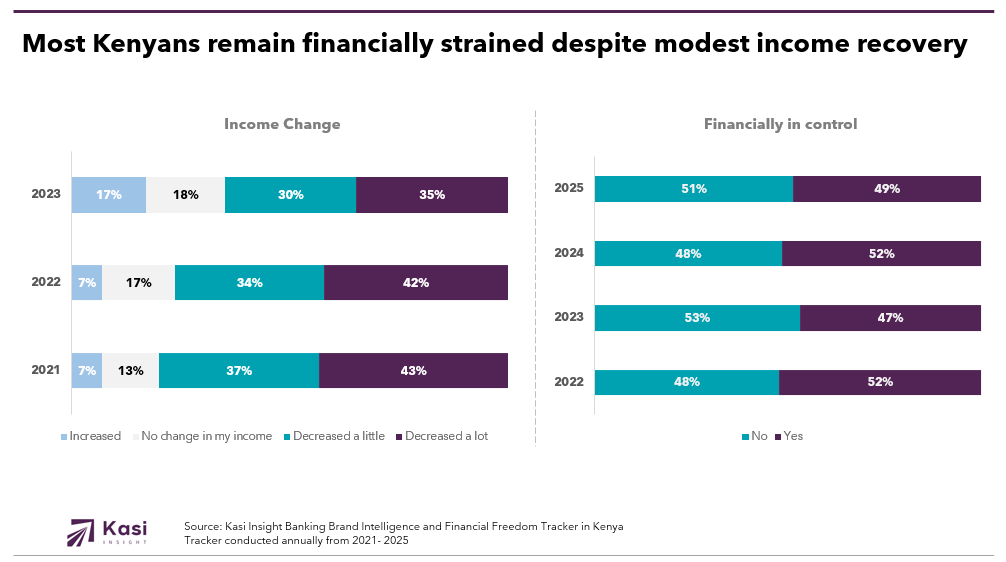

Most Kenyan consumers have yet to experience a full recovery from the financial disruption caused by the COVID-19 pandemic. In 2021, 80% reported that their income had either decreased a lot or a little compared to pre-pandemic levels. By 2023, this had declined to 65%, suggesting some early signs of rebound. However, that momentum did not continue into 2024 and 2025. Only 17% of consumers reported any income gains by 2023, and the number has not meaningfully improved since.

The inability to bounce back is reflected in weakened day-to-day financial control. As of 2025, 51% of Kenyans say they are not in control of their monthly budgets or cash flow, up from 48% in 2022. This is despite rising financial awareness. Between 2022 and 2025, more than 60% of consumers consistently reported having intermediate or advanced personal finance knowledge. The gap between awareness and action is widening.

Emergency readiness and retirement planning remain significant concerns. In 2025, 42% of consumers say they do not have enough savings to manage an unexpected expense. At the same time, 55% say they are not saving adequately for retirement, marking a reversal of the slight gains made in 2023 and 2024. These figures paint a picture of a financially strained population that is trying to stay afloat in a climate of rising cost pressures and inconsistent income streams.

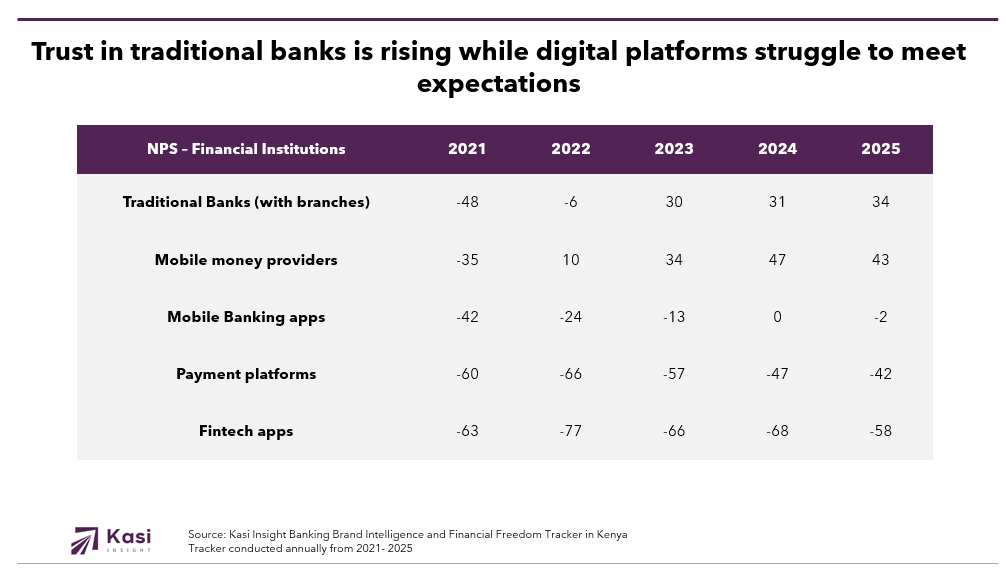

Consumers have re-established their relationship with traditional financial institutions. By 2025, 83% say they use products or services from traditional banks, up from 69% in 2021. Mobile money providers remain the most widely used, at 85%. What is more telling is how trust has evolved. Net Promoter Scores for traditional banks have improved sharply, moving from a deeply negative -48 in 2021 to a positive +34 in 2025. Mobile money services have shown a similar rise, reaching +43 in 2025 after climbing steadily from -35 in 2021.

Despite this trust resurgence, the digital banking experience is not keeping pace with consumer expectations. Banking apps, now used by 58% of consumers, have failed to translate usage into satisfaction. Their NPS stood at 0 in 2024 and slipped to -2 in 2025. Fintech applications, once seen as disruptors, have lost momentum entirely. Usage dropped from 29% in 2021 to 21% in 2025, and their NPS remains consistently negative.

This signals a growing divide between what consumers are promised and what they experience. Access is no longer the differentiator it once was. Consumers are demanding reliability, intuitive interfaces, helpful support systems, and overall digital experiences that mirror the seamlessness they have come to expect from mobile money services. The trust gained by traditional institutions must now be defended through delivery, not marketing.

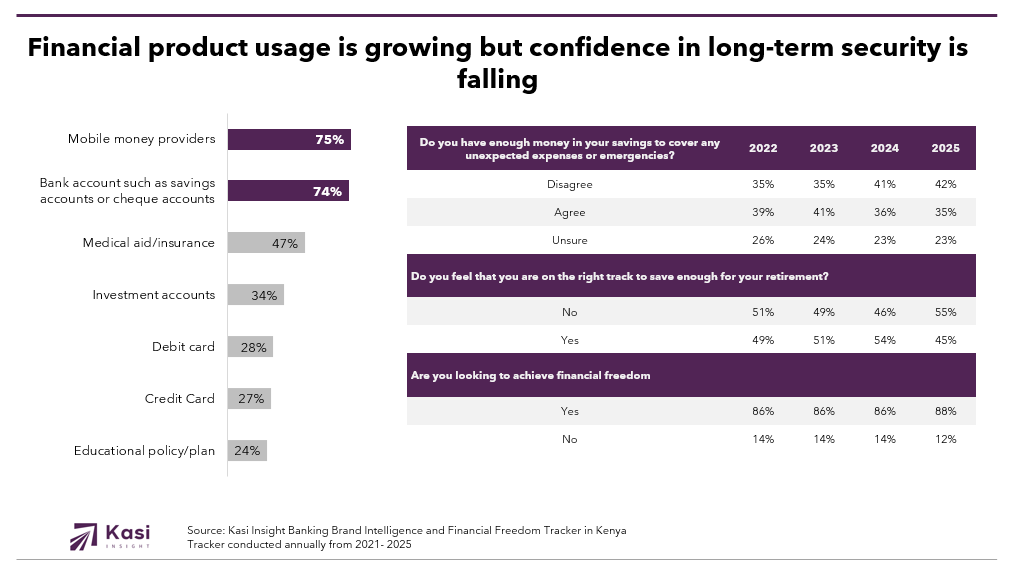

Financial product ownership has risen steadily since 2021. By 2025, 74% of Kenyan consumers say they have a bank account, up from 63% four years prior. Mobile money usage also rose from 63% to 75%. There is also a shift in borrowing and investment behaviors. Credit card ownership climbed from 20% to 27%, while investment account use increased from 19% to 34%. These changes suggest broader financial engagement and a willingness to explore more complex financial tools.

However, deeper examination reveals a troubling paradox. While product penetration is expanding, confidence in long-term financial wellbeing is not. As of 2025, more than half of consumers (55%) say they are not on track to save enough for retirement. This marks a five-year high, reversing the modest progress seen in 2023 and 2024. Insurance ownership is also in decline. Life insurance dropped from 20% in 2021 to 15% in 2025, and funeral insurance has more than halved, falling from 14% to just 6%.

At the same time, ambition remains high. In 2025, 88% of Kenyans say they are actively working toward financial freedom. Consumers are exploring more tools, but the emotional and structural support needed to feel secure is missing. This gap between usage and confidence presents a major opportunity for the banks willing to go beyond product sales and invest in guidance, education, and resilience-focused services.

Retail banking in Kenya now faces a consumer base that is digitally engaged, financially literate, and highly aspirational but still under pressure. The opportunity is not in access but in empowerment. The winners will be those that create tangible value, simplify decisions, and rebuild resilience.

Kenyan consumers have made it clear that they want more than products. They want a financial partner. They want help navigating volatility, making decisions with confidence, and achieving long-term goals. As digital tools multiply and access improves, the next frontier is emotional trust and everyday relevance.

The retail banks that lead from 2025 onward will be those that offer more than transactions. They will be the ones that simplify life, rebuild financial control, and help every Kenyan move from survival to stability. This is not just the future of banking, it is the future of value.

Share on socials using this caption: Retail banking in Kenya is shifting as consumers seek more than access, they want confidence, stability, and support 💡 trust in traditional banks is rising 🏦 but financial stress remains high and digital platforms are under pressure 📉 #RetailBanking #KenyaFinance #KasiInsight #ConsumerTrends #FinancialResilience #BankingStrategy #FintechAfrica

2804 views

Share article

Uganda Banking Sector 2025: Growth with Discipline, What Marketing Signals Reveal About Balance Sheets

Kenya Banking Sector 2025: Reading the Balance Sheet Through Marketing Signals

How Consumer Sentiment Predicts South Africa’s Credit Cycles