Claudine Linda Wa Nciko

June 10, 2025

Share article

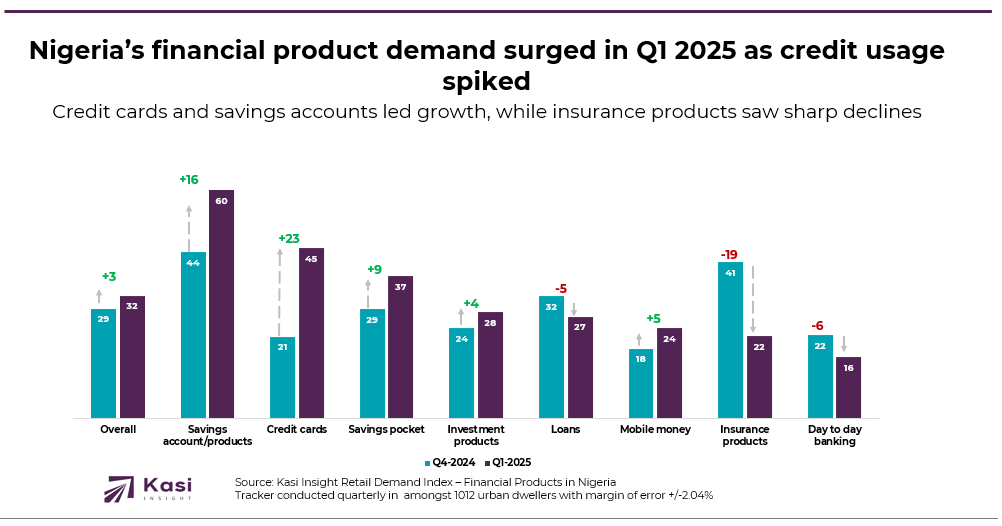

Kasi Insight’s Retail Demand Index (RDI), tracked quarterly, measures how consumer interest evolves across key financial products. The index ranges from +100 to -100, capturing changes in purchasing intent. In the first quarter of 2025, Nigeria recorded a modest 3-point rise in overall demand, moving from 29 in Q4 2024 to 32.

The strongest gains were seen in savings accounts, which climbed 16 points to reach 60, reflecting a renewed focus on secure financial habits. Credit cards followed with a 24-point increase, rising from 21 to 45, driven by growing interest in accessible credit and financial flexibility. Additional gains were noted in savings pockets, which rose 8 points to 37, while mobile money improved from 18 to 24 and investment products ticked up from 24 to 28. In contrast, demand for loans dropped by 5 points to 27, and day-to-day banking declined by 6 points to 16. Insurance registered the steepest fall, dropping 19 points from 41 to 22, signaling reduced interest in financial protection during this period.

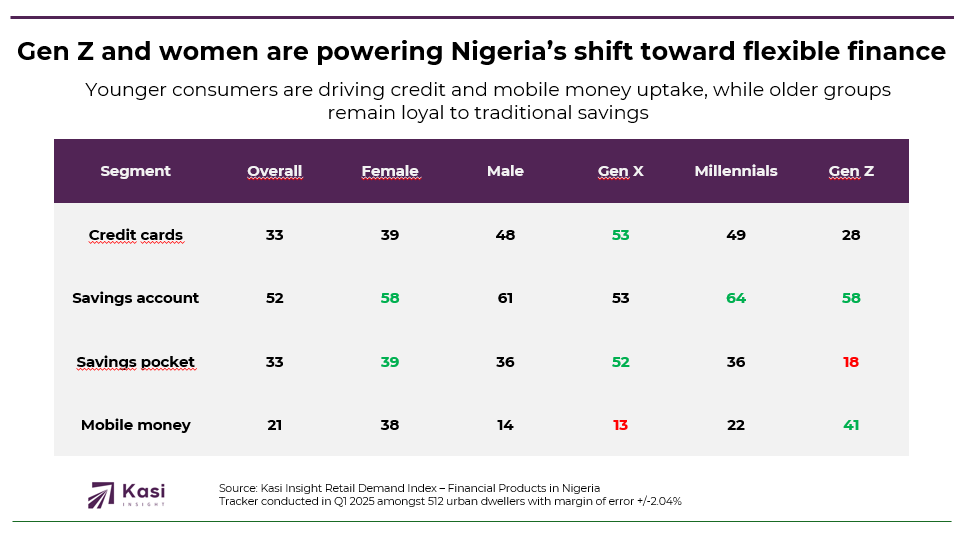

The surge in credit card demand in the first quarter was driven primarily by older male consumers. Gen X recorded the highest index at 53, followed by Millennial men at 49. Women also showed strong engagement at 39, while Gen Z remained lower at 28. This pattern indicates that credit-based financial tools are gaining more traction among older age groups. Savings accounts, which registered the highest overall gain, maintained broad appeal across the board. Millennials led with an index of 64, followed by Gen Z at 58 and Gen X at 53. Gender use was nearly equal, with men at 61 and women close behind at 58, reflecting the widespread adoption of formal saving options.

Savings pockets experienced moderate growth, peaking among Gen X at 52. Women scored slightly higher than men at 39 versus 36, while Gen Z recorded a much lower index of 18. These results suggest that informal saving tools resonate more with older and value-focused consumers. Mobile money continued its upward trend, led by Gen Z at 41. This was nearly double the index for Millennials at 22 and far ahead of Gen X at 13. Gender differences were even more pronounced, with women at 38 and men at 14. The data points to a clear preference for mobile-first financial solutions among younger and female consumers.

To remain competitive in Nigeria’s evolving financial landscape, financial service providers must adapt their offerings to reflect the shifting behaviors observed in the first quarter of 2025. The rise in credit card adoption and the sustained strength of savings products point to renewed consumer demand for control, security, and flexibility, particularly among Gen X and Millennials. Traditional banks have an opportunity to rebuild trust by improving the digital experience around core products such as savings accounts. This includes removing hidden fees, streamlining platforms, and offering practical incentives that reward consistent use. At the same time, the decline in insurance demand highlights a critical gap. There is a growing need for more accessible and digitally supported insurance solutions that appeal to younger consumers who remain less engaged with traditional risk protection products.

For fintechs and digital lenders, the strongest momentum is coming from Gen Z and female users. These groups are leading adoption of mobile money and showing increased interest in informal savings tools. They expect more than just functionality. They are drawn to mobile-first platforms, culturally relevant communication, and tools that reflect their everyday financial needs. Personalization is no longer optional in this environment. With clear generational and gender differences across product categories, providers must move beyond generic solutions and invest in strategies that are rooted in segmentation, trust, and user relevance. The patterns observed in early 2025 are not short-term shifts. They signal a deeper transformation in how Nigerians are choosing to engage with financial services, and the brands that respond with clarity, agility, and consumer insight will be best positioned to grow.

Share on socials using this caption: 📈 Nigerian consumers are rethinking money in 2025—credit card demand is up, mobile money is booming, and savings remain strong while insurance loses steam 💳📱💰 #NigeriaFinance #ConsumerTrends #FintechAfrica #RetailBanking #KasiInsight

1856 views

Share article

Uganda Banking Sector 2025: Growth with Discipline, What Marketing Signals Reveal About Balance Sheets

Kenya Banking Sector 2025: Reading the Balance Sheet Through Marketing Signals

How Consumer Sentiment Predicts South Africa’s Credit Cycles