Sandra Beldine Otieno

March 14, 2024

Share article

Earlier this month, a second international rating agency reaffirmed its 'B' rating for Kenya's banking sector, coupled with a negative outlook due to the persistent challenge of high Non-Performing Loans (NPLs). The 'B' rating signals a speculative investment risk level, indicating that while banks are meeting their financial obligations, their stability is threatened by potential economic downturns. Fitch Ratings Limited pinpointed the sector's significant exposure to overdue public sector payments as a primary vulnerability, noting the ripple effect of government payment delays on contractors, which, in turn, has hampered their ability to repay bank loans. This bottleneck has directly impacted loan quality, propelling the sector's NPL ratio up by 170 basis points in the first nine months of 2023, reaching a concerning 15% by the end of the third quarter.

Central Bank of Kenya (CBK) figures revealed an alarming climb in NPLs to a record Sh634 billion by the end of October last year, with the default rate escalating to 15.3%, up from 13.8% in the previous year. Amidst these challenges, the leading tier-one commercial banks have significantly increased their loan-loss provisions, setting aside Sh55.57 billion in the first three quarters of the year, a hefty 48% jump from Sh37.55 billion in the prior year. This increase in provisions has nibbled away at bank profits, which slightly decreased to Sh199.6 billion in the first ten months from Sh204.7 billion in the corresponding period in 2022, despite an uptick in interest income, underscoring the profound impact of loan-loss provisions on the sector's earnings.

Moreover, CBK reports have identified trade, manufacturing, and real estate as the sectors most affected by defaults, constituting 58% of the total NPLs as of June, with manufacturing experiencing the most significant default increase. The Credit Report Survey indicated that 45% of lenders forecasted an uptick in defaults towards the end of 2023 and into the early this year, highlighting a continued cautious outlook for Kenya's banking sector amidst these financial strains.

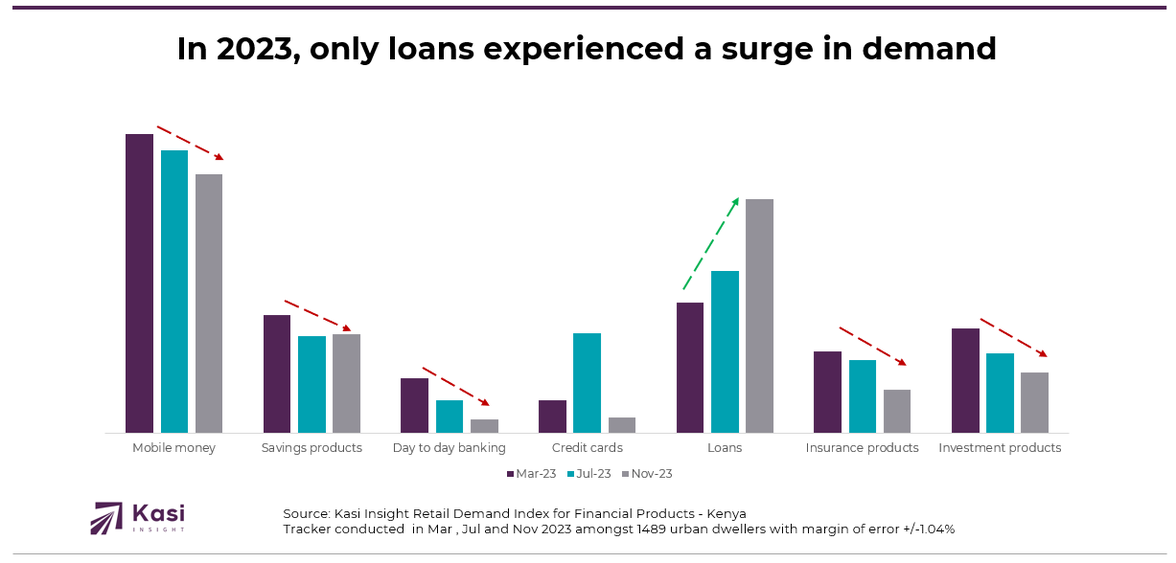

Kasi Insight’s Retail Demand Index reveals a nuanced picture of Kenya’s financial products demand throughout 2023, with an overall dip of three points from the year's start to end. The data shows a steady decline in mobile money, with figures retreating from 55 to a lower 48. While savings products showed resilience, holding steady at 22 before leveling off at 18, day-to-day banking faced a significant downturn, collapsing from 10 to a mere 3. Credit card usage witnessed a mid-year surge, peaking at 18 in July, only to taper off to 3 by November. The insurance and investment sectors weren’t immune to this downward trajectory, decreasing from 15 to 8 and 19 to 11, respectively.

In contrast, the loans category bucked the overall negative trend, charting a remarkable rise from 24 to 43 points through the year. Despite the economic pressures and the banking sector's cautious stance prompted by rising loan defaults and increased loan-loss provisions, the Kenyan populace's inclination towards borrowing suggests an adaptive response to financial challenges, possibly driven by the need to manage immediate financial pressures or seize growth opportunities through credit.

For banks in Kenya, the reaffirmed 'B' rating with a negative outlook due to high Non-Performing Loans (NPLs) signifies a precarious situation requiring strategic adaptation. The surge in NPLs to a record high and the subsequent increase in loan-loss provisions signals a tightening of credit conditions and a shift towards more conservative lending practices. This situation could lead banks to reassess their risk management strategies, enhance their credit monitoring processes, and possibly recalibrate their approach to loan provisioning to better align with the evolving risk landscape.

Furthermore, the consistent increase in loan demand, as evidenced by the rise in the loans category from 24 to 43 points through 2023, despite the overall dip in demand for other financial products, indicates a growing consumer reliance on credit. For banks, this trend presents both a challenge and an opportunity. On one hand, the increased demand for loans amidst rising NPLs necessitates a cautious approach to lending to mitigate risk. On the other hand, it offers an opportunity to expand their credit portfolios, provided they implement robust risk assessment and management strategies to safeguard against potential defaults.

Additionally, the decline in demand for savings products, day-to-day banking services, and other financial instruments, juxtaposed with the rising loan demand, suggests a shift in consumer financial behavior that banks need to address. They may need to innovate their product offerings and enhance their service delivery to meet changing consumer needs while also educating their customers on prudent financial management to mitigate the risk of defaults.

The reaffirmation of Kenya's banking sector with a 'B' rating amid high Non-Performing Loans (NPLs) highlights the critical challenges and opportunities facing financial institutions. With NPLs reaching record highs and impacting bank profits due to increased loan-loss provisions, banks are navigating a tightrope between maintaining financial stability and responding to the growing demand for loans. This scenario underscores the urgent need for banks to refine their risk management practices and lending strategies. Moreover, the contrasting trends in financial product demand, particularly the surge in loan demand against a backdrop of declining usage of other financial services, reflect a significant shift in consumer behavior. Financial institutions must adapt by innovating their product offerings and enhancing customer education to navigate this complex landscape.

Share on socials using this caption: 🚀 Dive into the heart of Kenya's banking sector as we explore the tightrope walk between soaring non-performing loans and a burgeoning demand for loans. Discover how financial institutions are navigating these choppy waters to fuel growth and maintain stability. 💼📈 #KenyaBanking #FinancialResilience #LoanDemand

2107 views

Share article

A Strategic Material for Development Sustainable Roads in Africa

Foresight Is No Longer Optional: Why Africa’s Decision Makers Must Move From Insight to Intelligence

Africa’s Data Dilemma: Waiting for the Porsche While Refusing the Bicycle