Sandra Beldine Otieno, MSc

June 2, 2025

Share article

Kenya’s consumer landscape reflects a shift from crisis response to intentional adaptation. After years of economic pressure and structural change, consumers are spending more strategically, prioritizing balance in wellness, embracing digital tools, and expecting real environmental accountability from brands. These shifts mark a deeper recalibration of values and trust. Kasi Insight identifies four trends shaping this transformation: Strategic Resilience, Holistic Vitality, Emerging Reality, and Eco-Powered Living.

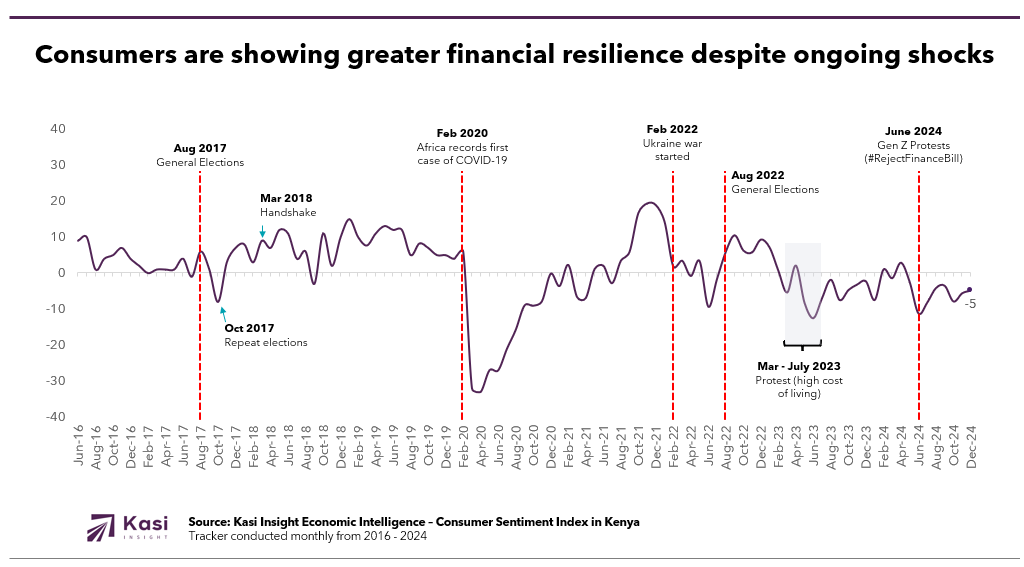

Faced with prolonged financial strain, many households across the country are shifting from reactive cutbacks to thoughtful control. Throughout 2024, overall consumer sentiment remained subdued, hitting a low of -13 in June before rising to -5 by December. Still, 40% of people reported being able to meet their regular expenses by year-end, a sign of stabilizing financial routines. More than half (52%) focused their spending strictly on essentials such as food, rent, and education. This marks a behavioral shift where stability, not abundance, defines financial wellbeing.

Different groups are adapting in different ways. Gen X and those in higher income brackets are using digital tools to track prices, delay purchases until post-payout periods, and trade down to affordable brands when necessary. Millennials and Gen Z are also becoming more cautious, with 36% reporting they postponed purchases and 33% relying on apps to evaluate products before committing. While inflation eased toward the end of the year, people did not revert to impulse spending. Instead, they made calculated decisions based on timing, value, and necessity, signaling a more mature and deliberate mindset.

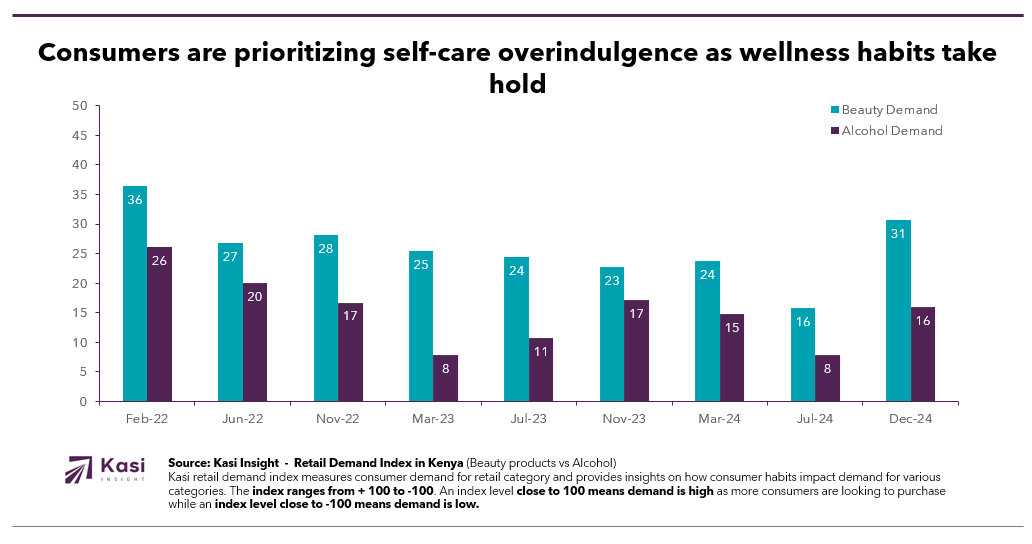

Health is no longer defined by gym visits or medical checkups. People are embracing a broader sense of wellbeing that includes emotional balance, social connection, financial control, and personal care. In 2024, 91% rated their overall health as good or excellent, and 30% reported improvements in physical health within the past six months. Eating habits are shifting too, with 50% saying they consume at least two servings of fruits or vegetables daily. At the same time, personal care and beauty product demand nearly doubled from mid-2023 to late 2024, driven by the growing importance of self-esteem and everyday routine.

Even with rising interest, wellness decisions remain grounded in affordability. Nearly half (46%) cited cost as a key obstacle to healthier living. Despite this, 39% said they had adopted home-based practices such as walking, cooking healthier meals, and simplifying routines. This signals a departure from aspirational wellness trends in favor of practical solutions that fit real budgets. Mental health is also rising on the agenda, with more people seeking tools and products that support emotional calm and daily consistency.

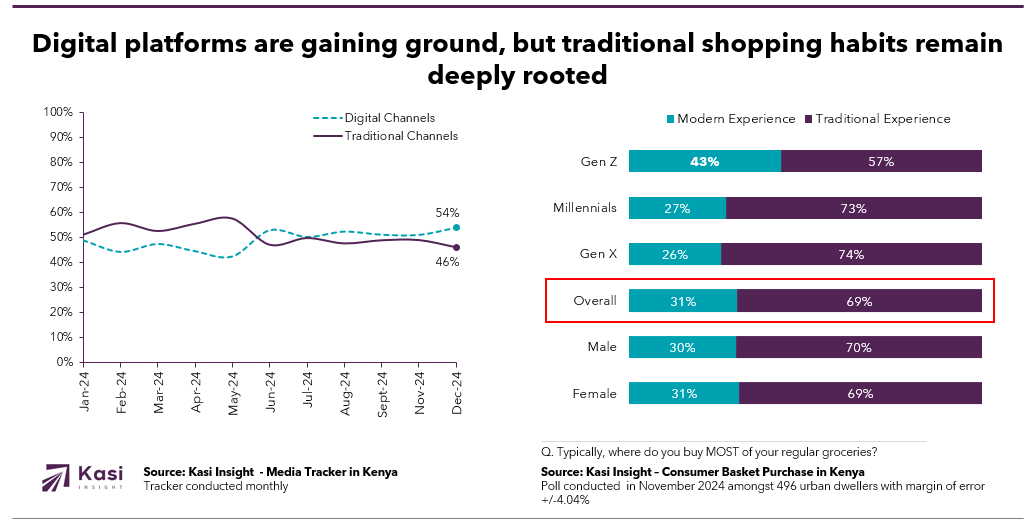

Shopping journeys are becoming less linear and more blended, as people combine physical retail with digital tools to explore, compare, and purchase. Although 69% still preferred in-person shopping in 2024, digital platforms are increasingly influencing decision-making. Mobile money now facilitates 60% of transactions, and most individuals use four or more digital touchpoints including apps, USSD, SIM menus, and agency banking. Nearly half (49%) browse online before buying in-store, while 35% do the reverse illustrating a complex but purposeful flow between channels.

Generational habits show clear contrasts. Gen Z is driving digital adoption, with 43% regularly shopping online for its speed and variety. In contrast, Gen X still values physical stores for trust, face-to-face interaction, and pricing clarity. Media usage follows similar lines: younger groups lean on social media and streaming, while older adults rely on television, newspapers, and radio. Across all groups, expectations have converged online messaging must match offline experiences. A disconnect between what is promised and what is delivered creates friction.

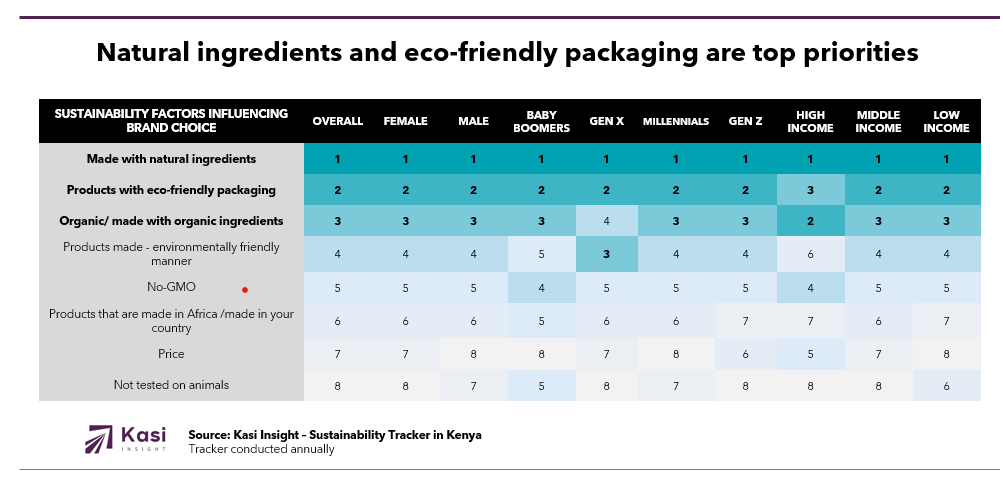

Environmental awareness is no longer the concern of niche segments. It has become a default consideration in purchase behavior. In 2024, 97% of respondents considered at least one sustainability factor when choosing a product. Natural ingredients topped the list at 53%, followed by recyclable packaging (48%) and plastic reduction (41%). Moreover, 59% expressed a preference for locally made products when price and environmental impact were aligned suggesting that sustainability and affordability are no longer in conflict but often reinforce each other.

Value systems are evolving, with younger audiences especially attuned to ethical sourcing and social responsibility, while older consumers prioritize ingredient transparency and reduced packaging waste. Yet trust remains a critical barrier. Nearly half (45%) said they were skeptical of sustainability claims without visible proof such as certification or sourcing disclosures. What people want is clarity and action. Brands that invest in community-based initiatives like tree planting, recycling, or local employment build stronger credibility. Sustainability is no longer an afterthought or seasonal campaign. It is a fundamental lens through which value, loyalty, and relevance are judged.

As consumers shift from crisis response to intentional living, brands must move beyond visibility and offer value that is timely, personal, and grounded in real needs. People are planning their spending around income flows, prioritizing essentials, and using digital tools to guide their decisions. This new pattern calls for strategies that reflect how people actually live and buy. Timely offers, flexible product bundles, and simplified choices can help brands stay relevant. Gen X and higher-income groups respond well to tools that offer financial control, while younger consumers prefer mobile platforms that deliver clear and honest value.

Wellness has become broader and more practical. It now includes emotional wellbeing, financial balance, and daily confidence, not just physical fitness. Consumers are choosing routines that support calm and consistency over perfection. Brands have an opportunity to meet these needs with products that fit into everyday life and support long-term balance. Offering simple, affordable solutions that promote ease and emotional resilience will resonate more than high-performance claims. Loyalty will come from helping people feel steady and supported rather than pressured to achieve an ideal.

At the same time, the consumer journey now cuts across digital and physical spaces. People expect a consistent experience from browsing to purchase to follow-up. Mobile money, social media, and in-store shopping are all part of one flow, and any break in that experience weakens trust. Environmental responsibility is also becoming a basic expectation. Most consumers now consider sustainability when making choices and want to see proof through packaging, sourcing, or community investment. Brands that show real action, communicate clearly, and embed purpose into their core will be better positioned to build lasting trust in this more deliberate and values-driven market.

Share on socials using this caption: As Kenyans embrace 🧠 mindful living and 💰 smarter spending, brands must respond with ✅ authenticity, 💡 practical innovation, and 📊 proof of impact to build lasting trust. #KenyaTrends #ConsumerShift #PurposeDrivenBrands #KasiInsight #SustainableLiving #WellnessDriven

1479 views

Share article

Uganda’s retail sector shows early 2025 fatigue as consumers cut back on essentials but remain engaged in wellness and lifestyle choices

Inflation fatigue is deepening financial stress for consumers in Ivory Coast

Cameroonians appetite for staples and fresh produce grows while demand for proteins dips