Yannick Lefang, Eng

March 26, 2026

Share article

In most banking systems, balance sheet strategy is revealed with a delay—through earnings releases, loan growth data, or shifts in asset allocation. In Kenya in 2025, however, the earliest and most visible signal of change did not come from financial statements. It came from marketing.

Across the sector, a consistent pattern emerged. Campaigns moved away from credit-led growth narratives and toward a different objective altogether: deposit mobilization, transaction monetization, and customer ownership. This shift was not cosmetic. It was structural. It reflected a banking system operating in what can best be described as a liquidity accumulation and risk containment phase, where the priority was no longer to expand lending aggressively, but to strengthen the foundation upon which future lending would eventually resume.

What made 2025 particularly revealing is that marketing activity—often dismissed as brand-building—functioned as a leading indicator of balance sheet intent. Banks were signaling, in plain sight, how they intended to position themselves for the next cycle.

The macro-financial backdrop explains much of this shift. Private sector credit growth remained subdued, while credit risk, although stabilizing, continued to constrain risk appetite. At the same time, banks increasingly allocated capital toward government securities, favoring predictable yields over uncertain lending returns. Profitability, in turn, was driven less by loan expansion and more by margin optimization.

In such an environment, the traditional banking growth model—lend more, earn more—becomes less viable. What replaces it is a more cautious, optimized approach: build low-cost funding, protect asset quality, and extract value from existing customer relationships.

The marketing landscape in 2025 mirrored this reality with remarkable consistency.

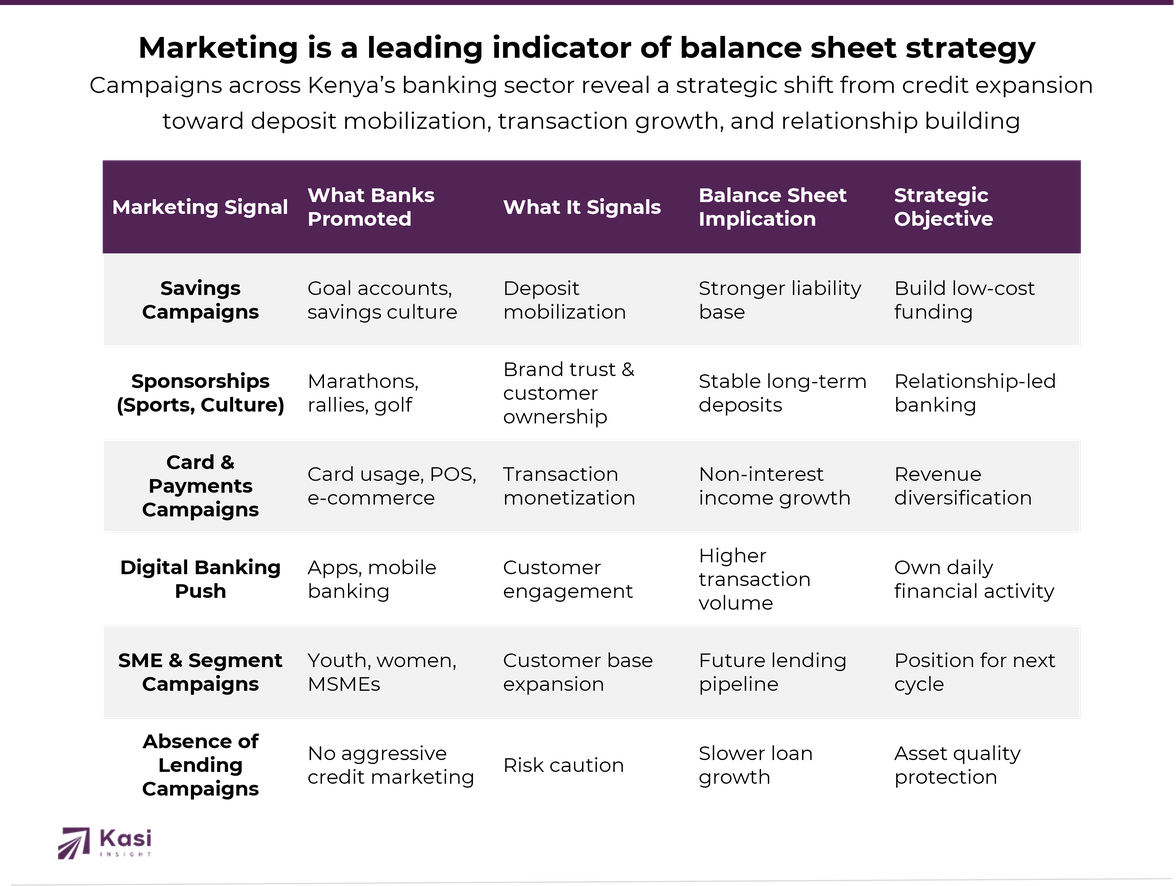

Offline campaigns were dominated by large-scale sponsorships—sports, culture, and national events. From rally championships to marathons and golf circuits, banks invested heavily in platforms that delivered mass visibility and trust. These were not short-term acquisition tactics. They were long-duration brand plays designed to anchor banks within the national psyche and strengthen emotional affinity with customers.

At the same time, digital and performance-driven campaigns told a more tactical story. Banks pushed card usage, e-commerce spending, and everyday transaction behavior. Messaging emphasized financial discipline, savings, and lifestyle integration rather than borrowing. Customer acquisition efforts became increasingly segmented, targeting youth, women, MSMEs, and affluent individuals with tailored propositions.

Taken together, these campaigns reveal a system shifting from product-led banking to relationship-led banking. The objective was no longer simply to open accounts or issue loans, but to embed the bank within the daily financial lives of customers.

The implications for balance sheet strategy are clear.

First, deposit growth emerged as the dominant priority. The prevalence of savings campaigns and financial security messaging signals an intense competition for low-cost funding. Banks were actively strengthening the liability side of their balance sheets, seeking stable and inexpensive sources of capital. In practical terms, this reflects a preference for liquidity over risk-taking.

Second, the absence of aggressive lending campaigns is equally instructive. It indicates a cautious stance toward credit expansion and a continued focus on asset quality. Rather than pushing loans into a still-fragile environment, banks opted to deploy capital into safer instruments, particularly government securities.

Third, there was a visible effort to rebalance revenue streams. With non-interest income under pressure, banks turned to payments and transactions as a key growth lever. Card campaigns, digital banking adoption, and transaction incentives all point to a strategic shift: from owning accounts to owning transactions.

This is a subtle but important transition. In a relationship-led model, the value of a customer is not defined solely by their borrowing capacity, but by the frequency and breadth of their financial interactions with the bank.

At its core, the sector in 2025 can be understood through a simple optimization framework: Profitability is being driven by a combination of low-cost deposits, yield from government securities, and transaction-based income, while minimizing exposure to credit risk.

Lending, while still central to the banking model, has temporarily taken a secondary role. It is not absent—but it is no longer the primary engine of growth.

One of the most telling aspects of 2025 is not what banks did, but what they did not do. There were no widespread unsecured lending campaigns. No aggressive “easy credit” narratives. No large-scale pushes to expand loan books at pace.

This absence is itself a signal. It suggests that banks, collectively, do not yet see the conditions required for safe and sustainable credit expansion. Instead, they are preparing—building liquidity, strengthening customer relationships, and positioning themselves for a future inflection point.

If 2025 was a year of positioning, the next phase is likely to be one of re-expansion. As interest rates stabilize and credit demand gradually recovers, banks will be better placed to deploy the liquidity they have accumulated. The shift back toward lending will likely be gradual, supported by improved asset quality and more targeted credit strategies. When this transition occurs, it will first appear in marketing. Loan campaigns will return. SME financing will be emphasized. Digital credit products will scale. And banks that have successfully built strong deposit bases and deep customer relationships will be best positioned to capture the opportunity.

For investors, the 2025 environment presents a nuanced picture. Banks are fundamentally safer, with stronger liquidity positions and more conservative risk profiles. However, growth is constrained in the absence of robust credit expansion. The key question is not whether banks will grow, but when the credit cycle will turn.

For policymakers, the alignment between marketing narratives and financial inclusion objectives is notable. Banks are actively promoting savings, financial literacy, and access for underserved segments. Yet the real test will be whether this translates into meaningful credit access over time.

From a Kasi lens, the most important insight is that marketing is not merely a reflection of current conditions, it is an early signal of future intent.

In 2025, that signal is clear. Kenyan banks are not retreating. They are recalibrating. They are building liquidity, strengthening relationships, and optimizing risk in preparation for the next phase of growth.

This creates a critical gap, and an opportunity. As banks move toward eventual credit re-expansion, the differentiating factor will not be access to capital, but the ability to deploy that capital intelligently. This requires better signals: on credit risk, on demand timing, and on segment behavior.

The Kenyan banking sector in 2025 should not be viewed as stagnant, but as strategic. Beneath the surface, a transition is underway, from credit-led expansion to relationship-led optimization. Marketing campaigns, when properly interpreted, reveal this shift with remarkable clarity. The sector is not yet in growth mode. But it is preparing for it. And in that preparation lies the clearest signal of what comes next.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

18 views

Share article

How Consumer Sentiment Predicts South Africa’s Credit Cycles

How Consumer Sentiment Predicts Kenya’s Credit Cycles

Kenya’s financial sector gains momentum as demand climbs in July 2025