Sandra Beldine Otieno, MSc

February 14, 2025

Share article

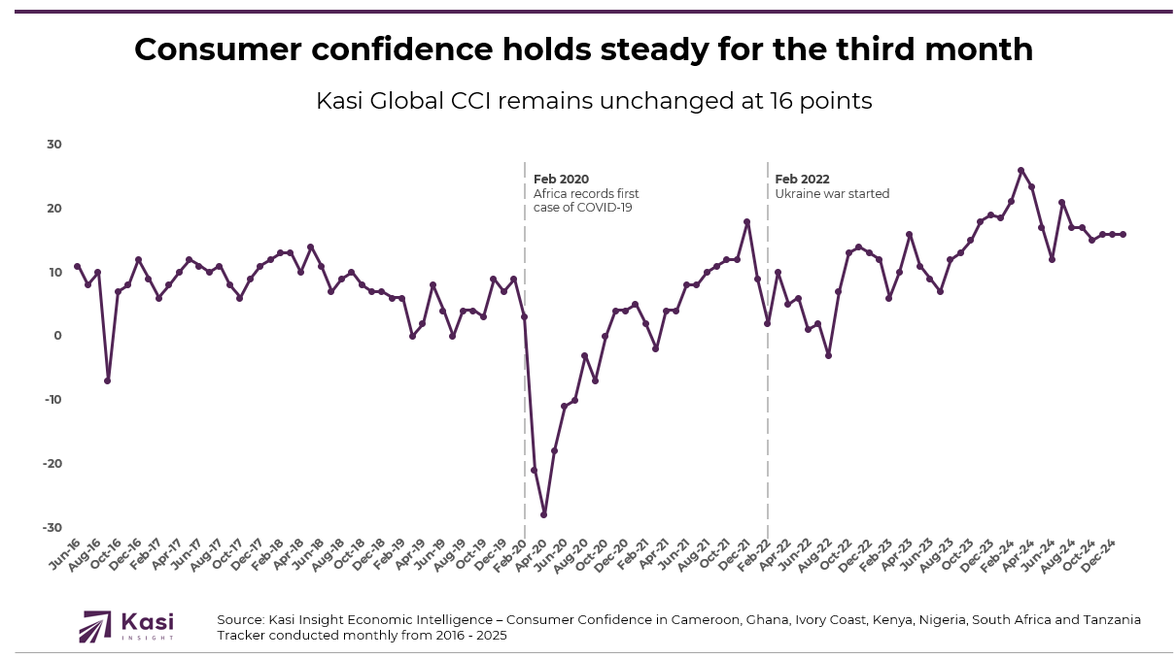

In January, consumer confidence in Africa held steady at 16 points, marking a third consecutive month of stability. This stagnation was driven by the unchanged current conditions and future expectations indices. While improvements in job prospects and personal finances signaled cautious optimism, declines in discretionary and household spending offset these gains. The overall sentiment remained unchanged, reflecting a balanced mix of economic resilience and financial uncertainty.

Household indices presented a mixed picture, with gains in some areas overshadowed by significant declines in others. The personal finance index edged up by 2 points, indicating slight improvements in individual financial stability, while the job prospect index surged by 8 points, suggesting renewed optimism about employment opportunities. However, household income remained unchanged at 35 points, signaling persistent financial pressure despite improved job expectations.

Spending patterns reflected this financial strain, with both discretionary and household spending indices declining sharply. The discretionary spending index dropped by 7 points, while household spending saw an even steeper decline of 14 points, highlighting consumer hesitation in non-essential purchases. These declines suggest that while individuals may feel more secure about future employment, financial constraints continue to limit spending, reinforcing a more cautious approach to household finances.

Despite these financial pressures, broader economic sentiment showed signs of recovery. The general country economic conditions index rose by 3 points, while the general city economic conditions index climbed by 8 points, pointing to a more positive perception of the overall economy. However, this optimism has yet to translate into increased household spending, reflecting ongoing economic uncertainty that continues to shape consumer behavior.

January’s consumer confidence remained stable at 16 points, but spending patterns revealed that consumers remain financially cautious despite signs of economic optimism. While the personal finance index rose by 2 points and the job prospect index surged by 8 points, these gains did not translate into increased spending. Household spending dropped sharply by 14 points, and discretionary spending fell by 7 points, indicating that consumers are still prioritizing necessities over non-essential purchases. With household income unchanged at 35 points, financial pressure is keeping many from spending freely. To drive engagement, brands must shift their approach—offering practical affordability, flexible payment options, and value-driven bundles that help consumers justify their purchases without straining their budgets.

At the same time, broader economic sentiment showed improvement, with the general country economic conditions index rising by 3 points and the general city economic conditions index climbing by 8 points. However, this optimism is not equally distributed across regions. Ghana, Ivory Coast, Kenya, Nigeria, and South Africa recorded increases in consumer confidence, signaling potential opportunities for brands to lean into aspirational messaging and future-focused marketing. In contrast, Cameroon and Tanzania saw declines, with Tanzania experiencing a sharp 23-point drop, reflecting heightened financial distress. This divide presents a clear arbitrage opportunity—brands can capture demand in optimistic markets by linking products to progress and long-term benefits, while in more cautious markets, the focus should be on affordability, reliability, and financial security.

To succeed, brands must do more than offer discounts—they need to help consumers feel financially empowered in their spending choices. This means introducing installment payment plans, loyalty programs that reward consistent purchases, and bundling products to create cost-effective solutions. Messaging should align with consumer sentiment, emphasizing economic growth and opportunity in more confident markets while reassuring financially strained consumers with practical, savings-focused offerings. By bridging the gap between sentiment and spending behaviors, brands can reinforce trust, drive engagement, and position themselves for sustained growth in an evolving economic landscape.

Share on socials using this caption: 📉 Consumer confidence in Africa remained stable at 16 points in January! While job prospects and personal finances improved, sharp declines in household and discretionary spending highlight ongoing financial caution. Brands must bridge the gap between optimism and spending by offering affordability, flexibility, and value-driven solutions. 💡💰 #ConsumerConfidence #AfricaEconomy #SmartSpending

1536 views

Share article

Trust Is Becoming Economic Infrastructure

Consumer confidence loses momentum in October

Confidence plateaus in September as caution defines household behavior