Mercy Cyrus

May 27, 2025

Share article

Kasi Insight's Cost of Living Tracker provides crucial insights into the shifting economic landscape across Africa. Conducted quarterly, the tracker offers a comprehensive analysis of consumer perceptions on rising costs across various sectors and how they are coping with inflationary pressures.

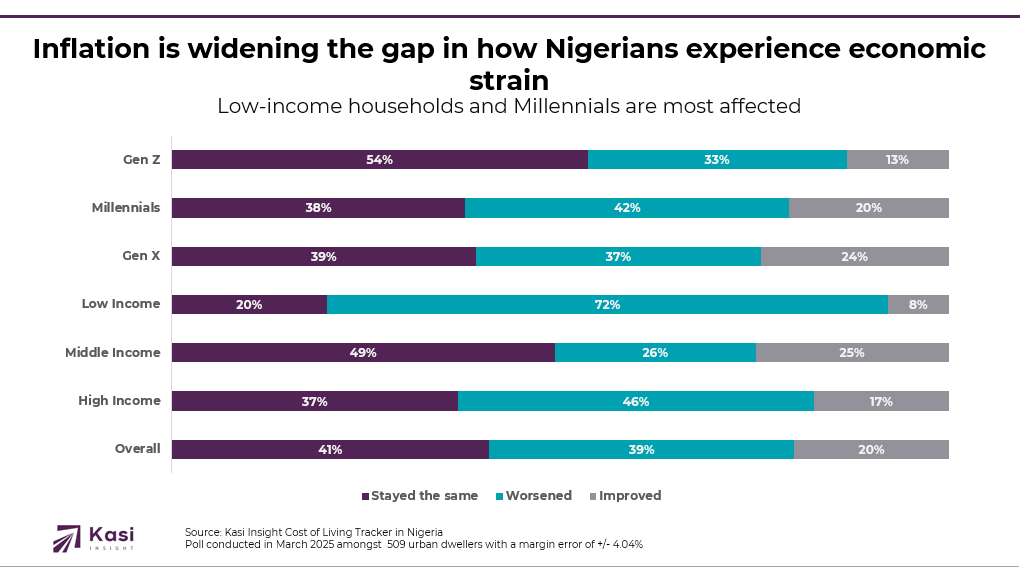

In Q1 2025, inflation continues to strain Nigerian households, making essentials like food, transport, and airtime increasingly unaffordable particularly for low-income groups. While 41% of respondents overall say their ability to meet daily expenses has stayed the same, the situation is far more concerning at the lower end of the income scale. Among low-income consumers, 72% report worsening conditions, and only 8% have seen any improvement, underscoring their heightened vulnerability. High-income earners are also feeling the pressure, though to a lesser extent, with 46% reporting a decline. In contrast, middle-income groups appear more resilient: 49% report no change and 25% note an improvement, possibly reflecting better financial buffers or access to alternative income streams.

Generational trends offer further perspective. Gen Z stands out as the most stable, with 54% seeing no change in their financial situation. However, only 13% report improvement, suggesting stability without progress. Millennials appear more affected, with 42% reporting a worsening condition. Gen X presents a more balanced picture, with 37% facing increased strain and 24% reporting some relief, highlighting a varied impact across age groups.

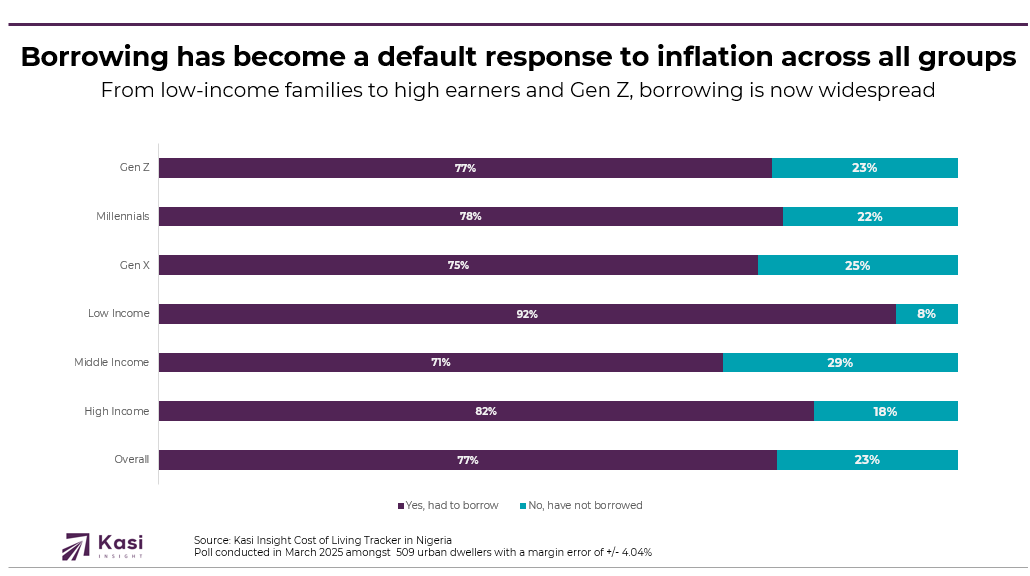

With inflationary pressures intensifying, many Nigerians are turning to borrowing as a primary means of coping with rising costs. Data reveals that 77% of respondents have borrowed money in recent months to cover daily expenses. The burden is heaviest on low-income households, where an overwhelming 92% report relying on borrowed funds underscoring their financial fragility. Even among high-income earners, 82% say they’ve resorted to borrowing, showing that the impact of inflation cuts across socioeconomic lines, though with differing intensity.

Generational patterns also shed light on this trend. Millennials (78%) and Gen Z (77%) are slightly more likely to borrow than Gen X (75%), reflecting the heightened exposure of younger Nigerians, many of whom are still building financial stability. Borrowing has become less of a last resort and more of a routine response to economic stress, fundamentally reshaping how households navigate daily life in an increasingly volatile environment.

As inflation continues to impact Nigerian households, borrowing has shifted from a fallback option to a widespread survival strategy across all income levels. This presents a timely opportunity for financial institutions and consumer brands to respond with tiered solutions that address the specific needs of different segments. For low income households, where 92% report borrowing, products such as affordable microloans, low interest credit options, and targeted savings plans for essentials like education and healthcare can offer critical support. These tools can help alleviate financial strain while building long term resilience.

High income earners are also feeling the pressure, with 82% reporting borrowing behavior. This group may benefit more from liquidity focused offerings such as short term credit buffers, premium financial tools, and wealth preservation services that help maintain their standard of living during periods of economic turbulence. Among younger Nigerians, particularly Millennials at 78% and Gen Z at 77%, borrowing is slightly more common than among Gen X. This highlights the need for youth focused solutions. Digital first credit products, combined with financial literacy programs on budgeting, debt management, and long term planning, can help younger consumers navigate uncertainty. Tailored interventions across income and age groups not only improve financial outcomes but also strengthen consumer trust and brand loyalty in a rapidly changing economic environment.

Share on socials using this caption: 💸 Inflation is driving Nigerians to borrow just to get by, with borrowing now common across all segments. Low-income households are the hardest hit, but even wealthier groups and younger generations are feeling the pressure. Financial solutions must reflect this new reality. #NigeriaInsights #CostOfLiving #InflationImpact #FinancialInclusion 📊

1549 views

Share article

Uganda Banking Sector 2025: Growth with Discipline, What Marketing Signals Reveal About Balance Sheets

Kenya Banking Sector 2025: Reading the Balance Sheet Through Marketing Signals

How Consumer Sentiment Predicts South Africa’s Credit Cycles