Yannick Lefang, Eng

March 19, 2026

Share article

In the world of macroeconomics and high finance, consumer sentiment is often treated as background noise - useful for context, but rarely central to decision-making. It is typically viewed as a lagging reflection of economic reality rather than a predictor of what comes next.

But over the past decade, that assumption has been quietly overturned.

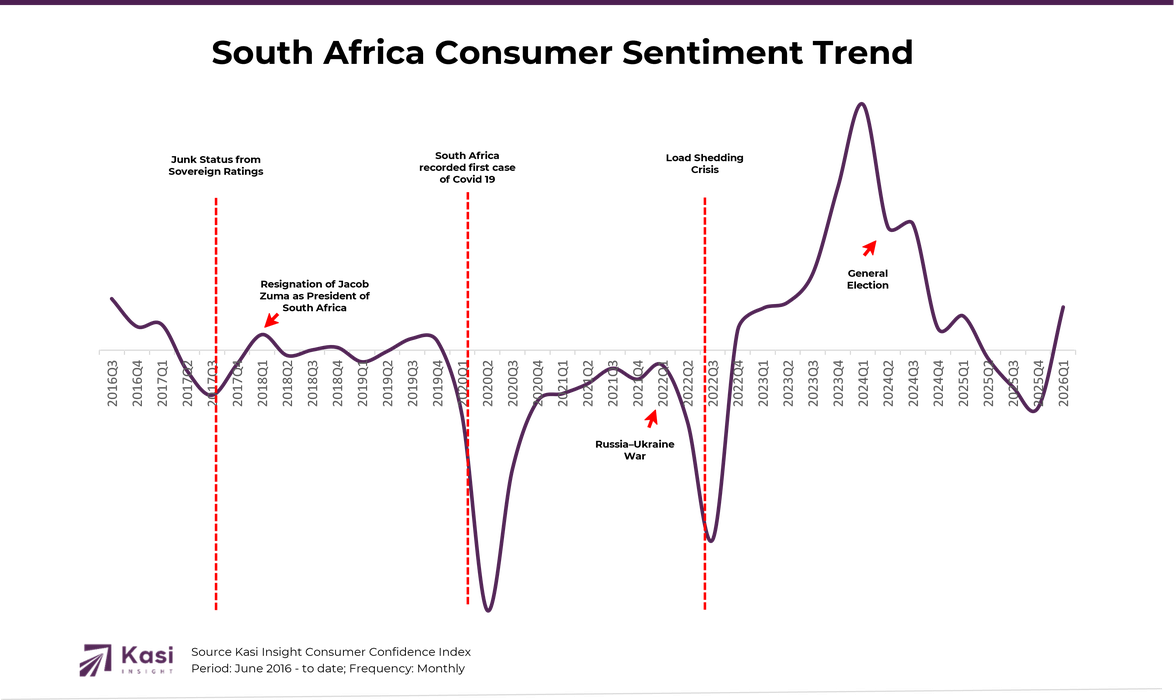

Longitudinal data from the Kasi Index of Consumer Sentiment (ICS) reveals something far more powerful: consumer sentiment is not just reactive - it is predictive. Between 2016 and 2026, the Kasi ICS has consistently acted as an early warning system, anticipating shifts in credit quality, banking profitability, and market performance well before they materialize in traditional financial indicators.

At the heart of this insight is what can be called the Kasi Credit Stress Signal, a repeatable pattern that gives leaders a one-to-two-quarter lead time to act.

The Kasi Signal is triggered when consumer sentiment drops below a critical threshold of -10. Once breached, a chain reaction begins to unfold across the economy. What follows is not random, it is structured, measurable, and consistent:

Fuel and FX volatility → ICS collapse → Rising NPLs → Slowing banking profits → Market instability

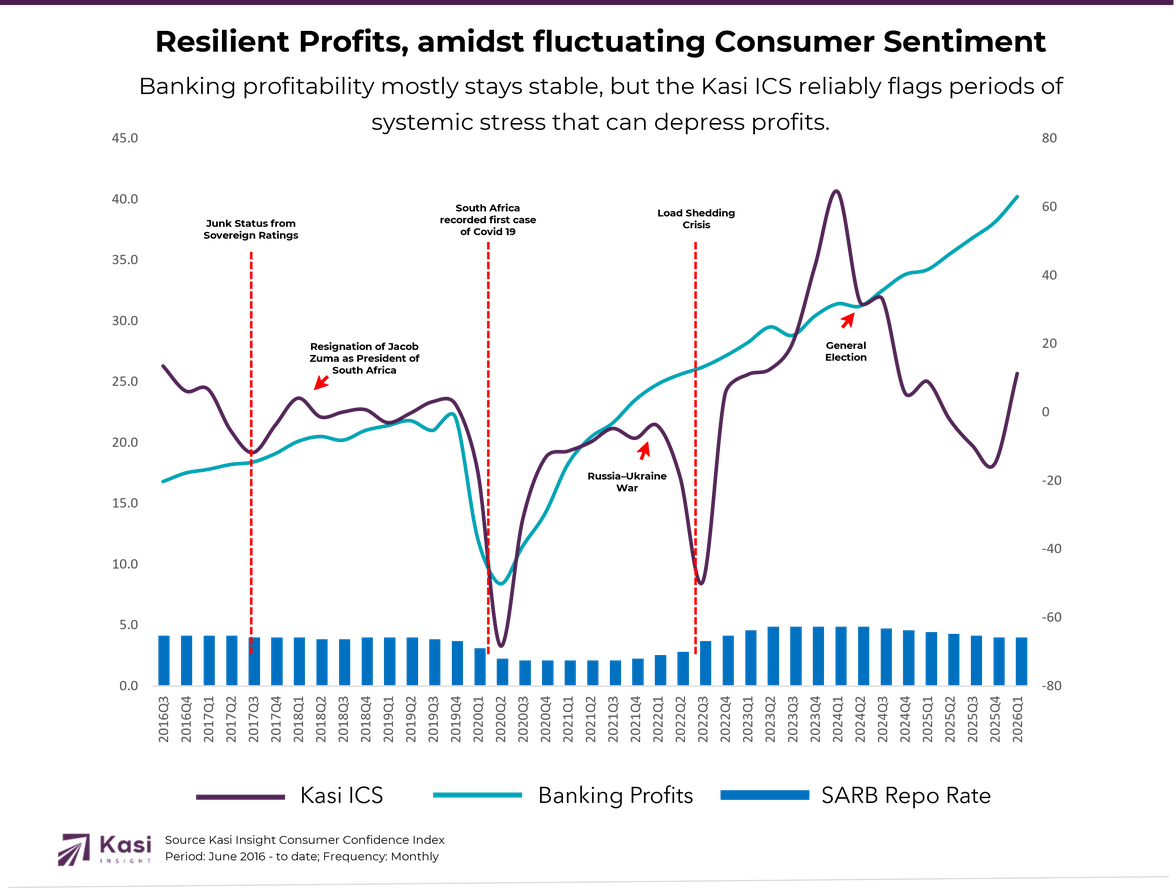

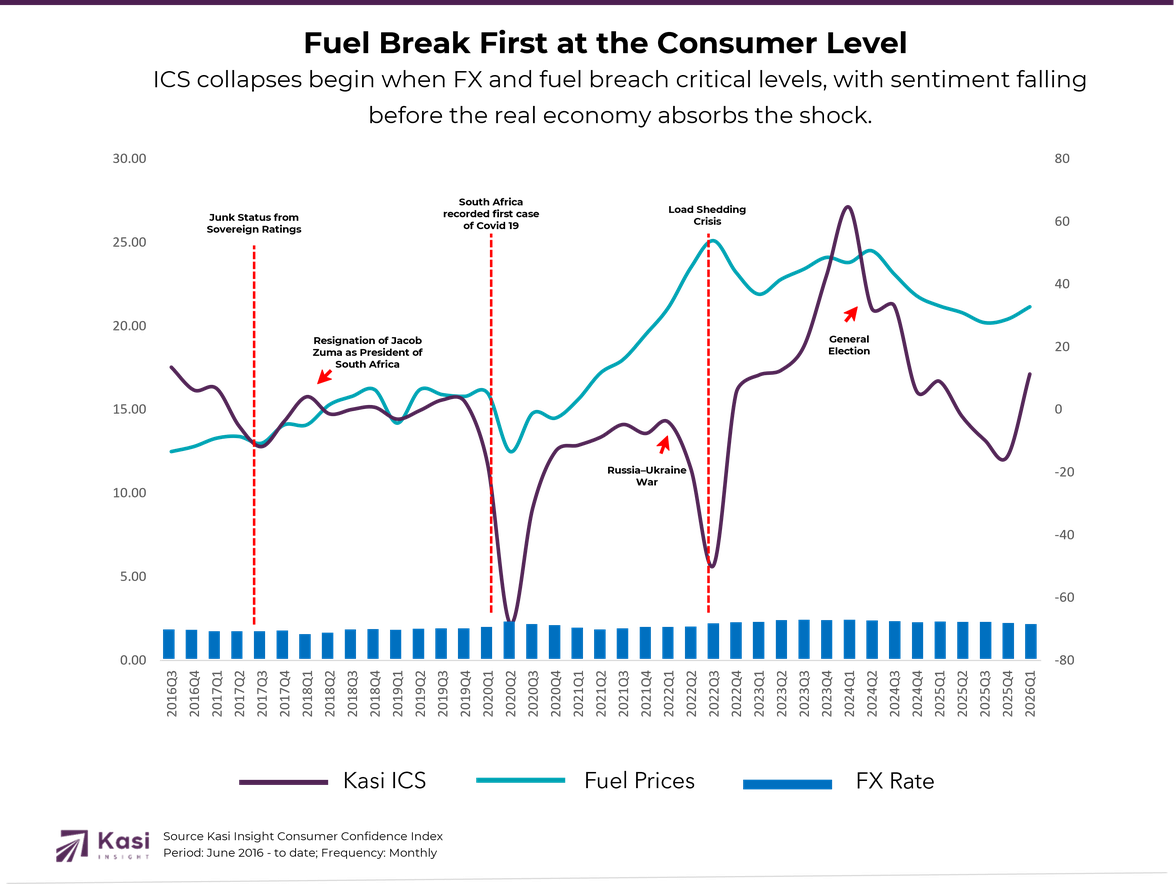

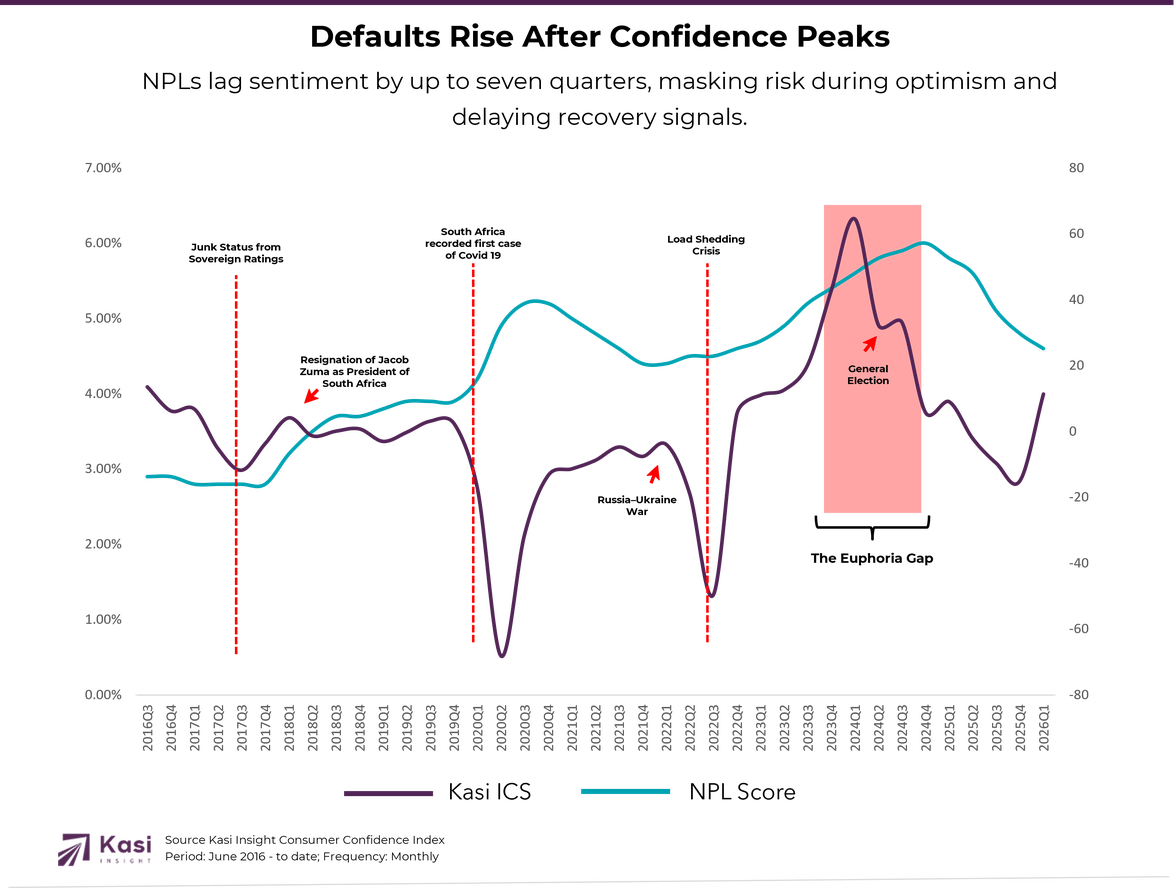

This sequence has repeated across multiple economic cycles, with the Kasi ICS acting as the first observable break in the system. The data reinforces this role. Over time, the Kasi ICS has shown meaningful lagged relationships with key financial indicators: a 0.41 correlation with banking profits, 0.34 with fuel prices, and 0.21 with non-performing loans (NPLs). More importantly, it leads them. Sentiment shifts happen first; financial outcomes follow.

The predictive power of the Kasi ICS becomes most visible during periods of structural stress, proving its ability to flag inflections before they hit the balance sheet.

The 2020 Pandemic: The ICS plummeted to -68.19 in 2020Q2. This wasn't just a mood shift; it was a total freeze in consumer confidence that foreshadowed a devastating crash in banking profits from 12.1 to 8.4.

The 2022 Energy & Load-Shedding Crisis: By 2022Q3, South Africa faced a severe energy crisis. The ICS hit a massive low of -49.66. This sentiment collapse happened right as fuel prices peaked at 25.10 ZAR, signaling an economy under extreme duress before NPLs began their steady climb throughout 2023.

The 2025 Reversal: In 2025Q4, the ICS dropped to -15.03, accurately flagging the JSE pullback from its peaks as consumers tightened their belts amidst high living costs.

One of the more nuanced dynamics revealed by the data is the relationship between consumer sentiment, interest rates, and banking profitability.

At first glance, rising interest rates should benefit banks by widening lending margins. And in the short term, they do. But the Kasi ICS reveals a constraint: profitability cannot be sustained without consumer confidence.

When sentiment weakens, borrowing slows, defaults rise, and the underlying demand for credit erodes, eventually offsetting the gains from higher rates. This creates a sweet spot. The most favorable conditions for banking profitability occur when: consumer sentiment is positive, and interest rates are stabilizing or declining

This exact combination emerged in early 2026. The ICS rebounded to +11.3, while the repo rate eased from 7.8% to 6.8%. The result was a surge in banking profits to 40.2, marking a cyclical high.

The implication is clear: sentiment is not just a supporting variable—it is the foundation. Without it, monetary policy alone cannot sustain growth.

If the Kasi ICS is the signal, then fuel prices and foreign exchange movements are often the trigger.

In South Africa, the ZAR/USD exchange rate and Fuel Prices are the most aggressive sentiment killers. When fuel prices spike or the currency weakens, the impact is felt directly through higher living costs. The ICS captures this transmission almost instantly. A consistent pattern emerges when the exchange rate breaches critical levels; such as the 17.00 ZAR/USD mark seen in 2022Q3 during the load-shedding crisis, consumer sentiment enters a sharp decline. The drop to -49.66 was a direct response to the Rand hitting 17.06 and fuel reaching 25.10 ZAR. By the time fuel prices peak, the damage to household confidence has already been done leading to the delayed NPL spikes we see quarters later.

For policymakers. Traditional indicators like inflation or credit data often respond with a delay. But sentiment reveals stress in real time, offering a forward-looking view of economic strain.

Non-performing loans are among the slowest indicators to adjust, which makes them particularly dangerous for reactive decision-making.

The Kasi data shows that NPLs typically lag sentiment shifts by up to seven quarters. This delay creates a blind spot: by the time credit deterioration becomes visible, the underlying cause is already in the past.

A clear example is the 2024 “euphoria gap.” During this period, the ICS reached a record high of 64.51, suggesting strong consumer confidence. Yet NPLs continued to rise, eventually hitting 6.00% by the end of the year.

This apparent contradiction reflects the lag effect. The rising defaults were not driven by current optimism, but by the stress of earlier shocks.

By contrast, the decline in NPLs to 4.60% in early 2026 is not simply a present-day improvement, it is the delayed result of sentiment stabilization that began in late 2025.

For risk managers, the lesson is critical: the ICS signals when the “fever” breaks, long before the credit data confirms recovery.

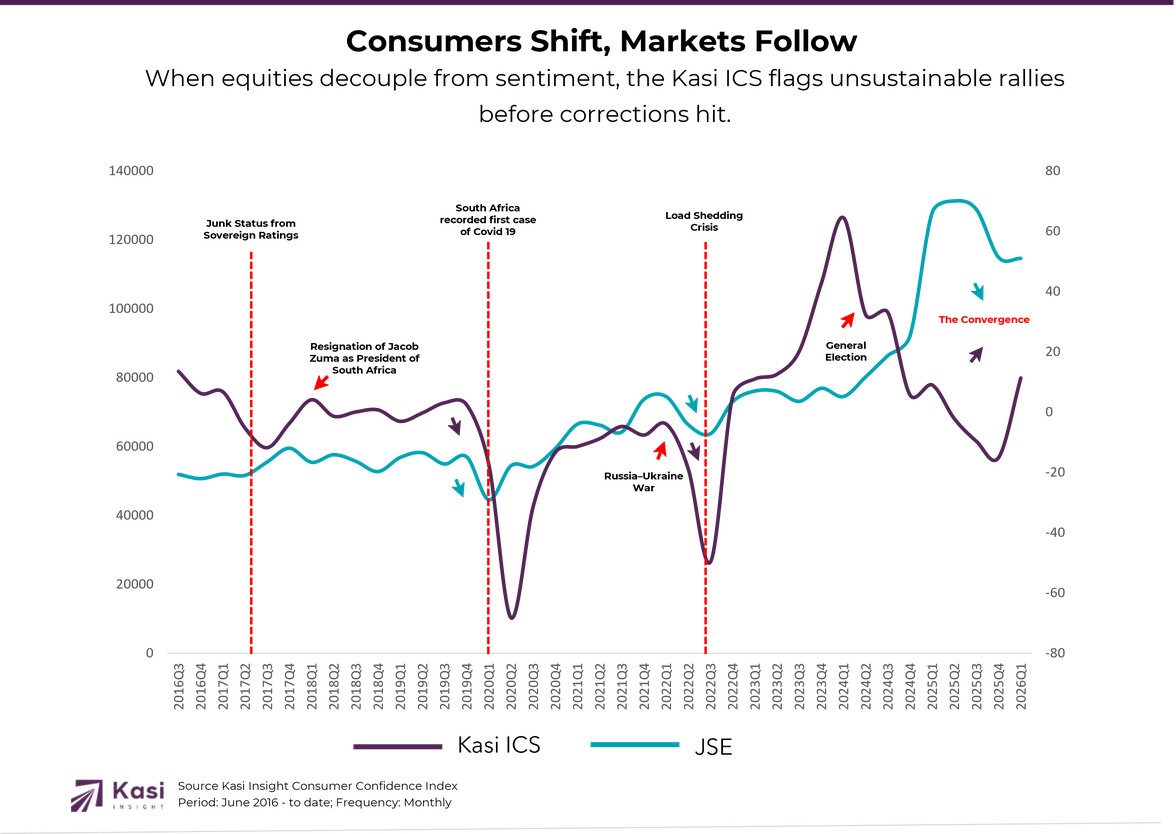

Equity markets, influenced by institutional flows and global liquidity, can often drift away from underlying economic reality. But the Kasi ICS provides a boundary, a set of guardrails that define what is sustainable.

When markets rise alongside improving sentiment, the trend is typically stable. But when they diverge, risk builds. This divergence was evident in 2025, when the JSE Index reached record highs even as the Kasi ICS turned negative. The signal was subtle but clear: consumers were under pressure, even as markets appeared strong. The eventual correction in early 2026 confirmed what the sentiment data had already suggested.

For investors, this creates a powerful lens. The ICS does not predict exact market movements, but it identifies when valuations are no longer supported by the consumer base that ultimately drives the economy.

The Kasi Credit Stress Signal transforms consumer sentiment from a passive indicator into a strategic tool.

For risk managers, a drop below -10 is not just a warning, it is a trigger to begin provisioning for future credit deterioration.

For banking executives, aligning profit expectations with both sentiment and interest rate dynamics becomes essential. Growth is only sustainable when consumers are confident enough to participate in the credit cycle.

For investors, divergences between sentiment and market performance offer early signals of overextension and potential correction.

What the past decade makes clear is that economic cycles do not begin in boardrooms or markets. They begin in households. The Kasi ICS captures this reality with unusual clarity. It measures not just how consumers feel, but how they are likely to behave, and in doing so, it reveals the direction of the broader economy.

In an environment defined by volatility, whether from fuel shocks, currency swings, or global disruptions, the ability to see these shifts early is no longer optional. It is a competitive advantage.

The signal is already there. The question is whether decision-makers are listening.

Kasi Insight. (2026). Consumer Intelligence & Innovative Research Solutions: Index of Consumer Sentiment (ICS) Methodology and Data [White paper]. Nairobi, Kenya: Kasi Insight Africa. Consumer Intelligence | Innovative Research Solutions | KASI - Kasi Insight

FTSE Russell. (2026). FTSE/JSE All Share Index (J203) Factsheet: Quarterly Performance and Volatility Analysis (2016-2026). London: London Stock Exchange Group. https://research.ftserussell.com/Analytics/FactSheets/Home/DownloadSingleIssue?issueName=J203

PwC South Africa. (2025). South Africa Major Banks Analysis: Resilience and Strategic Evolution (Reporting on Absa, Capitec, FirstRand, Nedbank, and Standard Bank). Johannesburg: PricewaterhouseCoopers. https://www.pwc.co.za/en/publications/major-banks-analysis.html

Republic of South Africa: Department of Mineral and Petroleum Resources. (2026). Official Adjustment of Fuel Prices: Historical Monthly Archive (2016-2026). Pretoria: Government Communications (GCIS). https://www.gov.za/news/media-statements

S&P Global Ratings. (2026). South African Banking Outlook 2026: Stronger Economy Lifts Growth and Performance Prospects. New York: S&P Global. https://www.spglobal.com/ratings/en/

South African Reserve Bank. (2026). Selected Statistics: Money and Banking Data (Repo Rates, NPL Ratios, and Exchange Rate Averages). Pretoria: SARB Publications. https://www.resbank.co.za/en/home/what-we-do/statistics/releases/selected-statistics

South African Reserve Bank. (2026, January 26). Statement of the Monetary Policy Committee (MPC). https://www.resbank.co.za/en/home/publications/publication-detail-pages/statements/monetary-policy-statements/2026/january

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

#CreditRisk #BankingInnovation #KasiICS #FinancialIntelligence #NPLs #KenyaBanking #RiskManagement #ConsumerSentiment #EconomicForecasting #DecisionIntelligence

209 views

Share article

Uganda Banking Sector 2025: Growth with Discipline, What Marketing Signals Reveal About Balance Sheets

Kenya Banking Sector 2025: Reading the Balance Sheet Through Marketing Signals

How Consumer Sentiment Predicts Kenya’s Credit Cycles