Yannick Lefang, Eng

March 11, 2026

Share article

Kenya’s banking sector has demonstrated remarkable resilience in recent years, reporting record profitability even as households face rising financial pressure. Beneath this apparent strength, however, lies a deeper signal about the health of the economy—consumer sentiment.

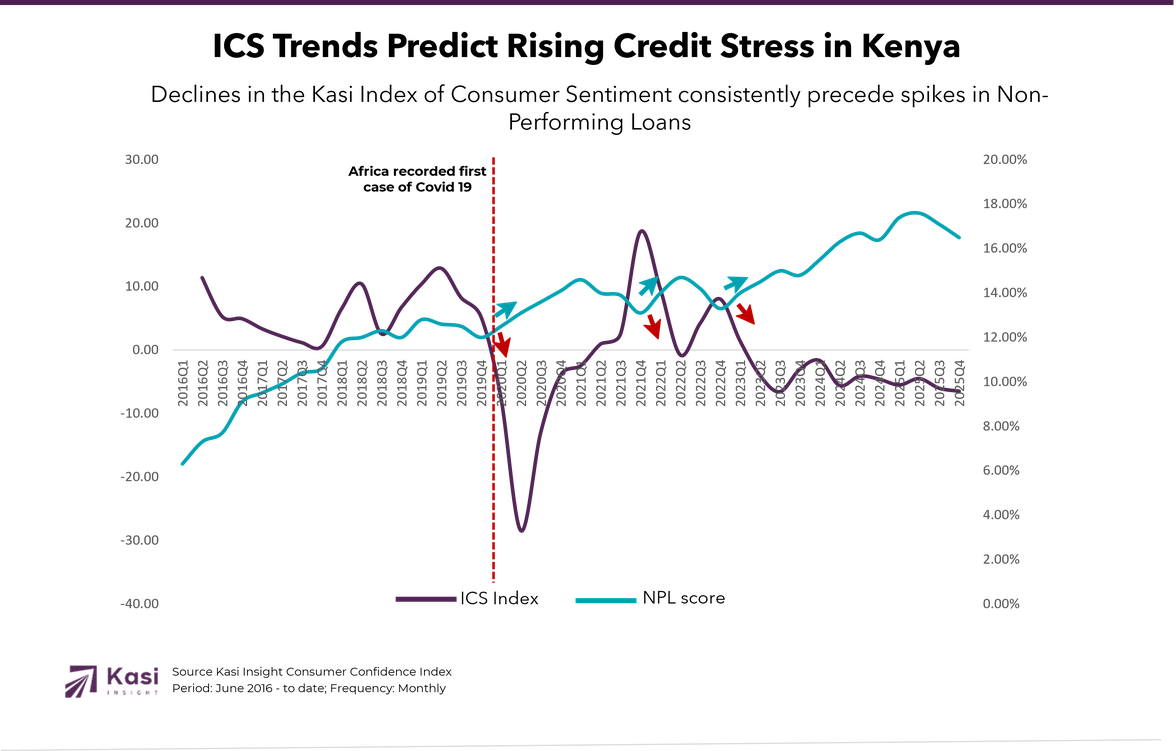

Using data from the Kasi Index of Consumer Sentiment (ICS), this analysis shows that shifts in household confidence consistently precede changes in credit quality in Kenya’s banking system. When consumer sentiment weakens, non-performing loans (NPLs) typically rise one to three quarters later, offering financial institutions an early warning signal of emerging credit stress. This finding has profound implications for financial institutions, investors, and policymakers. Traditional macroeconomic indicators often capture economic stress only after it has begun affecting markets. Consumer sentiment, by contrast, captures the household-level experience of economic change, revealing pressures before they become visible in bank balance sheets.

Three key episodes illustrate this relationship:

The 2020 COVID-19 shock, where sentiment collapsed months before loan defaults increased.

The 2022–2023 inflation cycle, where persistent pressure on household budgets gradually translated into rising credit stress.

The 2024–2025 negative plateau, where prolonged pessimism signaled growing financial strain even without a dramatic economic shock.

These patterns demonstrate that consumer sentiment is not merely a reflection of the economy—it is often the first indicator of financial stress within it.

The health of a banking system ultimately rests on the financial capacity of households and businesses. While banks operate with sophisticated risk models and strong capital buffers, the underlying ability of borrowers to repay loans depends on the economic realities faced by consumers. The Kasi Index of Consumer Sentiment provides a window into those realities.

Our analysis finds that the Kasi ICS leads changes in Kenya’s non-performing loan ratio by approximately one to three quarters, with the strongest correlation observed at a three-quarter lag. This lag reflects the natural progression of financial stress: Households first become cautious about their financial outlook then spending patterns begin to change. As budget pressures accumulate, loan repayments eventually deteriorate. By the time non-performing loans rise, the underlying financial strain has often been present for months. For banks and investors, this means consumer sentiment provides a critical early signal of credit risk.

The COVID-19 pandemic offers one of the clearest examples of sentiment acting as a leading indicator. Between the first and second quarters of 2020, consumer sentiment collapsed dramatically as households anticipated the economic impact of lockdowns and business disruptions. The Kasi ICS dropped from –7.52 to –28.42 in just one quarter. At the time, the banking sector in Kenya remained relatively stable. Loan defaults did not rise immediately. However, over the following year, the effects of the shock began to materialize. Kenya’s non-performing loan ratio gradually increased from 13.1% to 14.6%, reflecting the delayed financial consequences of the pandemic. This episode demonstrates a critical insight: consumer sentiment responds instantly to economic shocks, while credit deterioration appears later. For financial institutions, this gap represents a valuable window of opportunity to adjust lending strategies and risk exposure.

While the pandemic created a sudden shock, the inflationary cycle that followed was more gradual. Between 2022 and 2023, rising food prices, fuel costs, and interest rates placed sustained pressure on Kenyan households. During this period, the Kasi ICS declined from 9.65 to –0.75, signaling growing financial strain among consumers. Unlike the rapid deterioration during the pandemic, credit stress during the inflation cycle emerged slowly. Non-performing loans increased steadily, reaching 15.0% by mid-2023. This pattern highlights an important feature of consumer sentiment data: it captures both sudden shocks and gradual economic erosion. In environments where economic pressures accumulate over time, sentiment becomes a valuable tool for identifying emerging vulnerabilities before they appear in formal financial indicators.

The most recent reading from Kasi ICS data from 2024 and 2025 suggests that Kenya may be entering a new phase of economic risk. Rather than experiencing a dramatic decline, consumer sentiment has remained consistently negative, fluctuating between –1.6 and –5.6. At the same time, non-performing loans have continued to rise, reaching 17.6% by mid-2025. This pattern suggests that prolonged pessimism can be as damaging as a sudden economic shock. When households remain uncertain about the future for extended periods, they often delay major purchases, reduce discretionary spending, and become increasingly cautious about financial commitments. Over time, this environment can gradually weaken the repayment capacity of borrowers—even if macroeconomic conditions appear stable.

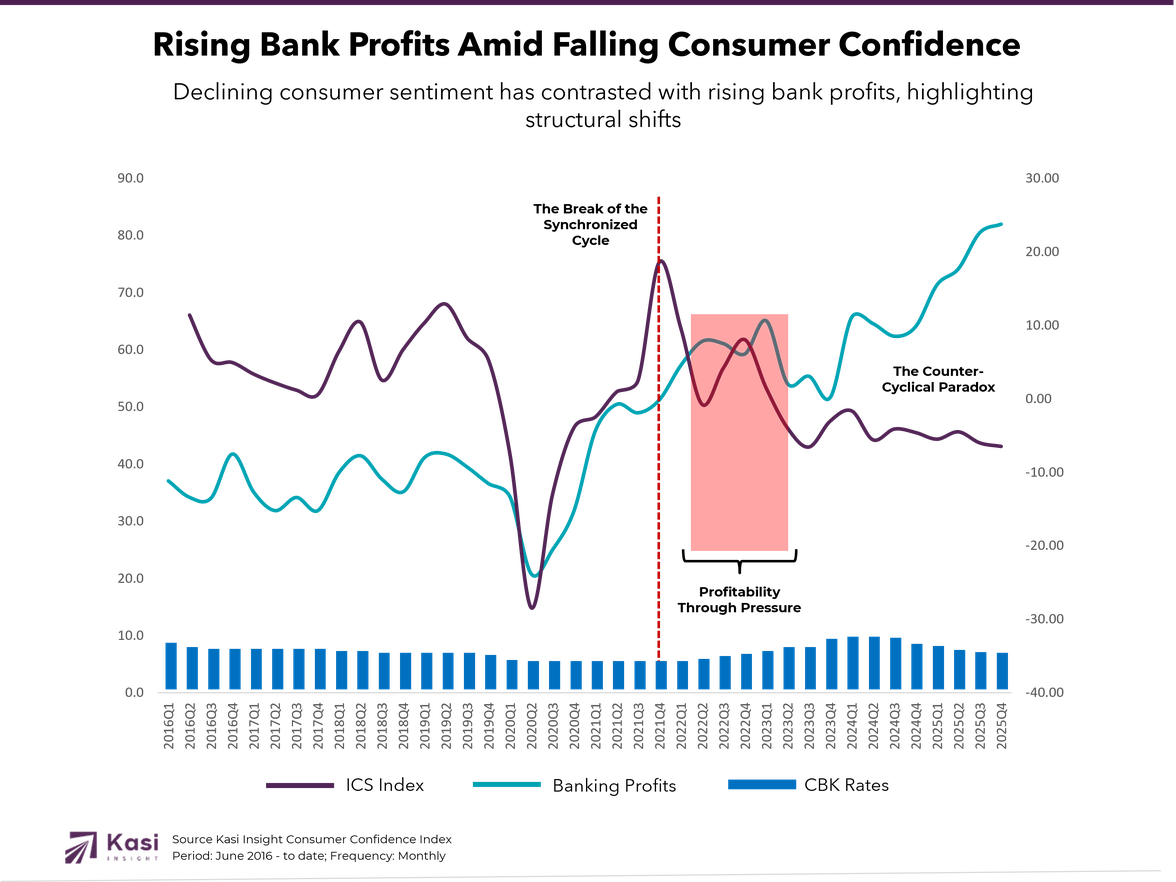

One of the most striking developments in Kenya’s financial system since 2021 is the divergence between bank profitability and consumer financial health.

Historically, bank performance and consumer sentiment tended to move in the same direction. A stronger economy lifted both banks and households. However, recent years have revealed a different dynamic. Even as consumer sentiment declined due to rising living costs, Kenyan banks reported strong and often record-breaking profits. Banking sector earnings increased significantly, reaching approximately KSh 82 billion in recent reporting periods. Several factors explain this divergence including higher interest rates improved net interest margins, risk-based pricing increased lending spreads and banks tightened credit conditions, reducing exposure to weaker borrowers. These changes have allowed banks to remain profitable even in an environment of growing consumer financial strain. For policymakers and investors, this divergence suggests that bank profitability alone is no longer a reliable indicator of overall economic health.

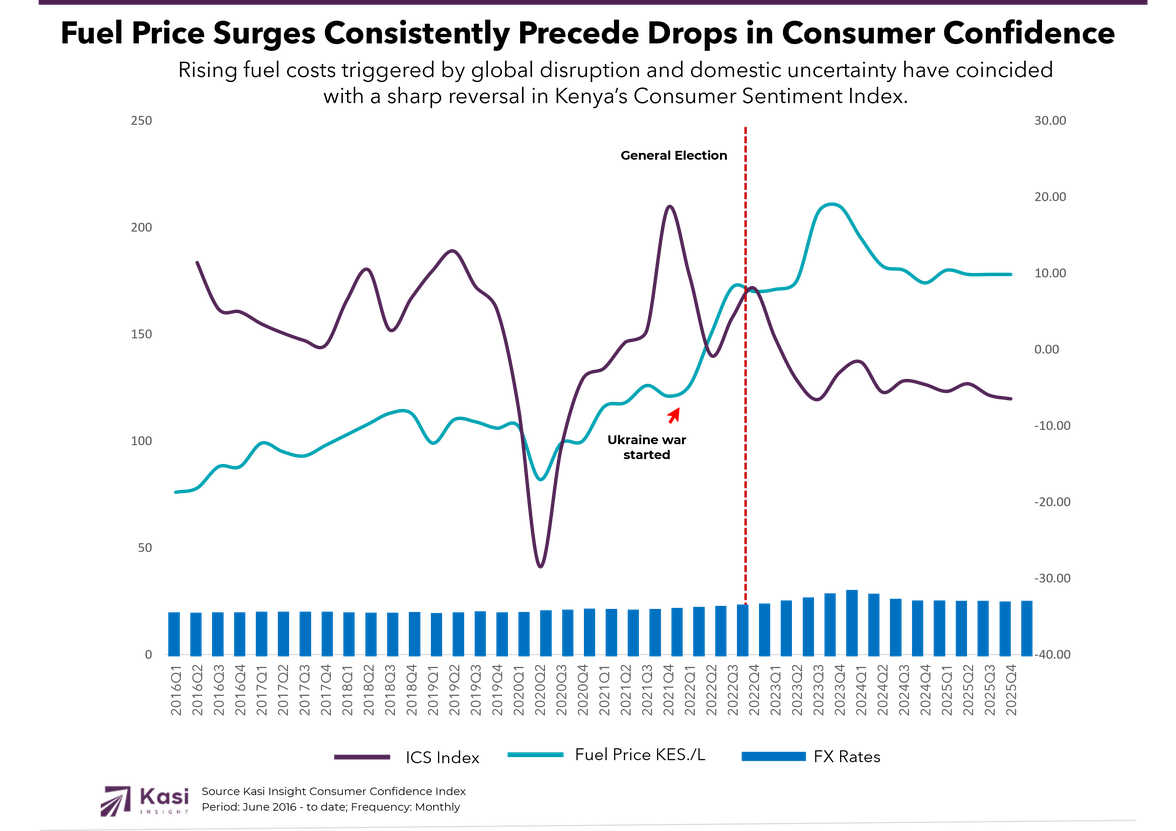

One of the strongest drivers of consumer sentiment in Kenya is fuel prices. The country relies heavily on road transportation, making fuel a central cost across the economy. When fuel prices rise, the effects ripple quickly through transport costs, food prices, and household budgets.

In 2023, fuel prices surged to KSh 210 per litre, triggering a significant cost-of-living shock. Although prices later stabilized around KSh 173 per litre by early 2026, global geopolitical tensions continue to pose risks to this fragile stability. Fuel price increases affect households through several channels including higher commuting costs, increased food prices due to transport costs and rising logistics expenses for businesses. As these pressures accumulate, households often cut discretionary spending and prioritize essential expenses such as transport and food. This adjustment in spending behavior often precedes broader economic slowdowns.

For financial institutions and investors, monitoring consumer sentiment can significantly improve economic forecasting and risk management. Key indicators to watch include:

Consumer Sentiment Trends - Persistent declines may signal emerging credit risk.

Fuel Price Movements - Energy costs remain a key driver of household financial stress.

Household Spending Patterns - Reductions in discretionary spending often precede broader economic slowdowns.

By combining these signals, decision-makers can gain a more complete picture of emerging risks in the economy.

In emerging markets, real-time economic data is often limited. Many traditional indicators are published with significant delays or fail to capture household-level dynamics. High-frequency consumer data offers an alternative approach. By continuously tracking household expectations, spending behavior, and financial confidence, sentiment indicators provide a forward-looking view of economic change. This capability is particularly valuable in economies where shocks—whether geopolitical, financial, or climatic, can propagate quickly through household budgets.

Kenya’s recent economic history demonstrates a consistent pattern: when consumers become pessimistic, credit stress soon follows. Consumer sentiment captures the financial pressures households experience long before those pressures appear in traditional economic indicators. As a result, it provides a powerful tool for anticipating economic cycles and managing financial risk. For Kenya’s banking sector, the message is clear. While balance sheets may appear strong today, the underlying health of the financial system ultimately depends on the financial resilience of households. And households often signal the future long before the markets notice.

About Kasi Insight

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

#CreditRisk #BankingInnovation #KasiICS #FinancialIntelligence #NPLs #KenyaBanking #RiskManagement #ConsumerSentiment #EconomicForecasting #DecisionIntelligence

236 views

Share article

Kenya Banking Sector 2025: Reading the Balance Sheet Through Marketing Signals

How Consumer Sentiment Predicts South Africa’s Credit Cycles

Kenya’s financial sector gains momentum as demand climbs in July 2025