Sandra Beldine Otieno, MSc

October 20, 2025

Share article

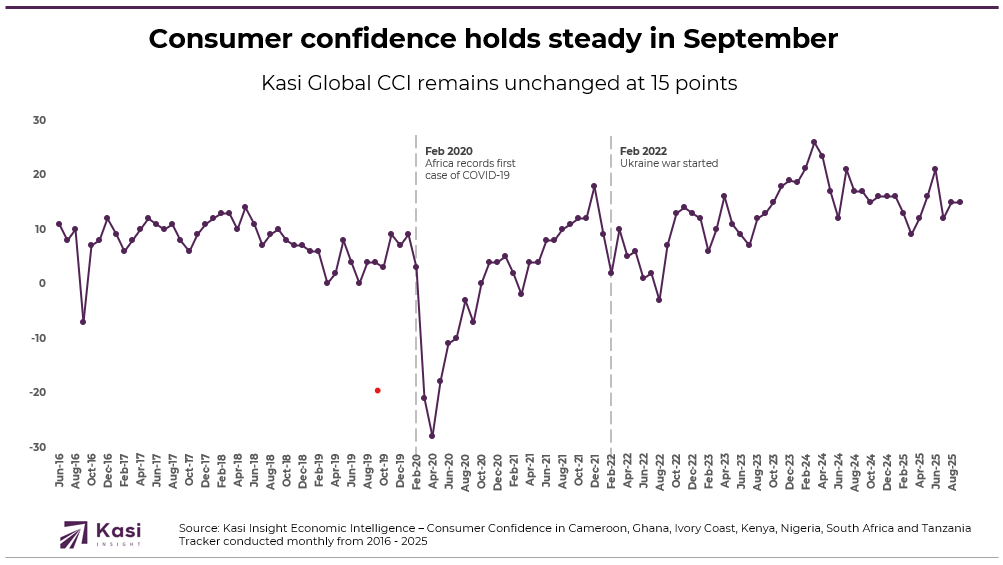

September marked a month of stability rather than recovery for consumer sentiment in Africa. Despite modest improvements in income and economic outlook, weaker household spending and job sentiment tempered optimism. The balance of gains and losses across markets points to an ongoing environment of cautious confidence, as consumers continue to weigh economic uncertainty against limited signs of improvement.

Consumer confidence in Africa remained unchanged in September, holding at 15 points recorded in August. The stability reflected a pause in the momentum gained in the previous month, as modest improvements in household income and broader economic outlook were offset by weaker spending and softer job sentiment. The household income index rose by 2 points, suggesting slight easing in financial pressure, while the personal finance index remained unchanged, indicating that most households continued to manage expenses cautiously despite marginal relief in earnings.

Spending indicators showed renewed weakness across key measures. The discretionary spending index inched up by 1 point, signalling limited recovery in non-essential purchases, while the household spending index declined by 5 points, reflecting restrained everyday consumption. These movements point to continued vulnerability in household budgets, with inflationary pressures and uncertain income growth keeping consumers cautious about discretionary outlays.

Labour market sentiment softened slightly, with the job prospects index slipping by 1 point, suggesting fading optimism about employment opportunities. However, perceptions of broader economic conditions improved marginally, as the general city economic conditions index rose by 2 points and the general country economic conditions index gained 1 point. The month was marked by balance rather than progress. While confidence held steady, households remained wary, underscoring the persistence of economic fragility despite isolated improvements in income and local outlook.

September reaffirmed the cautious consumer mood across Africa, with confidence holding steady and households remaining careful in their financial decisions. Small gains in income and modest improvements in local economic outlook were offset by weaker spending and softer job sentiment, underscoring the persistence of financial pressure. As the final quarter begins, consumers are prioritizing stability over aspiration, making deliberate choices shaped by discipline, value consciousness, and a desire to safeguard limited resources.

For brands, this environment demands clarity and authenticity. Consumers are seeking products that deliver tangible benefits, reliability, and fair pricing that reflects real economic conditions. Communication that feels empathetic and grounded in everyday realities will resonate more deeply than aspirational or exaggerated messaging. Brands that position themselves as consistent and supportive partners in helping households manage through uncertainty will build credibility and long-term trust. Those that overlook this shift risk appearing tone-deaf and disconnected from the lived experience of their audiences.

The path into Q4 calls for agility and purpose across diverse markets. In regions where financial strain remains acute, brands should focus on presence, reassurance, and dependable value. In markets showing early signs of resilience, cautious innovation anchored in utility and affordability can help reawaken engagement. The true differentiator in the months ahead will be how brands show up, those that combine reliability with empathy and a clear understanding of consumer realities will be best placed to earn loyalty in an era defined by caution and care.

Share on socials using this caption: 📈🔎 In September, consumer confidence held steady, signaling a pause in momentum after August’s modest rebound. While income levels and broader economic outlook showed small gains, spending and job sentiment softened, keeping households cautious. As Q4 begins, brands must lean into reliability, empathy, and real value to earn lasting trust. #AfricaInsights #ConsumerTrends #TrustEconomy #BrandStrategy

1860 views

Share article

Trust Is Becoming Economic Infrastructure

Consumer confidence loses momentum in October

Restless sentiment, divided opposition, and the path to continuity in Cameroon