Sandra Beldine Otieno, MSc

February 6, 2025

Share article

Kasi Insight's Cost of Living Tracker provides crucial insights into the shifting economic landscape across Africa. Conducted quarterly in 20 African markets, the tracker offers a comprehensive analysis of consumer perceptions on rising costs across various sectors and how people are coping with inflationary pressures.

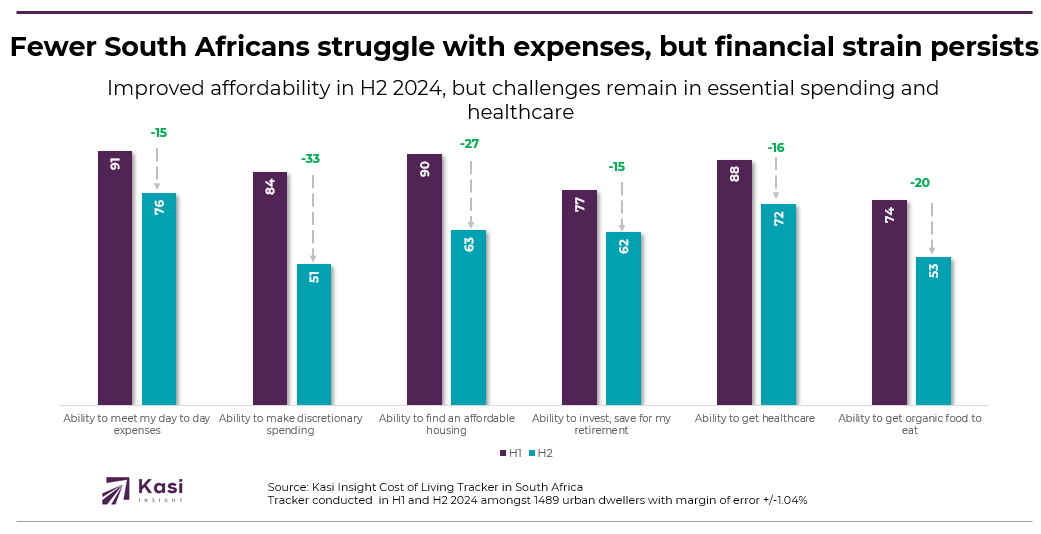

In South Africa, the latest findings indicate an improvement in financial well-being between H1 and H2 2024, as fewer people reported being negatively impacted by rising prices. The share of consumers struggling with discretionary spending, such as furniture, cars, and travel, decreased from 84 to 51—a notable 33-point shift—suggesting that more households are regaining financial flexibility. Similarly, affordability concerns around housing eased, with scores improving from 90 to 63 (-27), while access to organic or healthier food became less of a challenge, moving from 74 to 53 (-20), indicating that fewer consumers are being forced to opt for cheaper, less nutritious alternatives.

The pressure on essential expenses also showed signs of relief. The proportion of people struggling to meet daily expenses, including food, transport, and airtime, declined from 91 to 76 (-15). Long-term financial stability is also seeing gradual improvement, with fewer respondents finding it difficult to invest and save for retirement, as scores moved from 77 to 62 (-15). Similarly, concerns over healthcare affordability, including doctor visits, exams, and medications, decreased from 88 to 72 (-16), signaling a reduced financial strain on households.

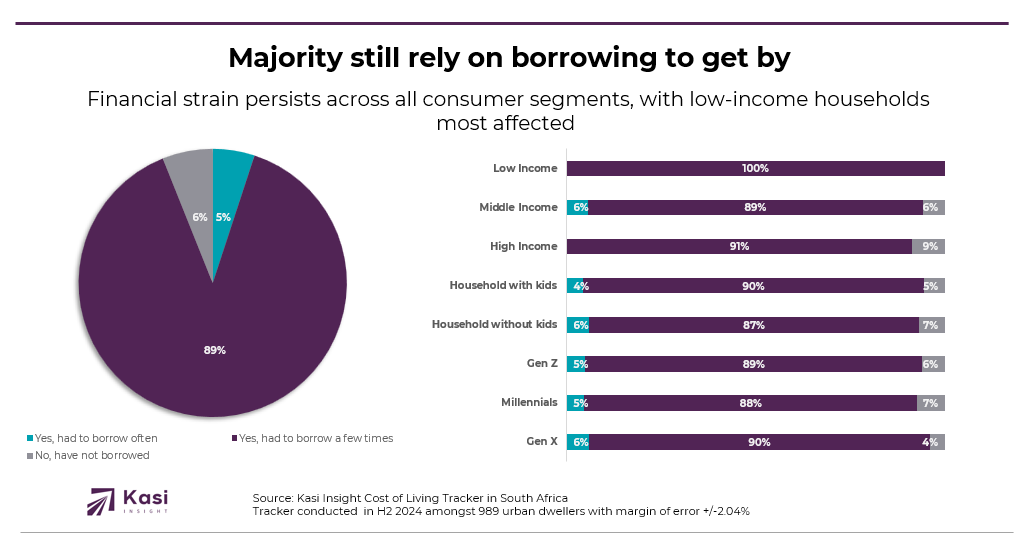

However, despite these improvements, many South Africans are still turning to borrowing to meet their day-to-day expenses. In H2, 89% of respondents reported having to borrow a few times, while a smaller 5% had to borrow frequently. Only 6% managed to avoid borrowing altogether, reinforcing the lingering impact of inflation on household financial stability. Breaking the data down by segments, borrowing remains high across all generations. Gen X respondents were the most affected, with 90% borrowing a few times, followed closely by Gen Z (89%) and Millennials (88%). This consistency across generations suggests that financial pressure is not limited to a specific age group but is instead a shared burden across different life stages.

Household composition also plays a role in borrowing behavior. Households with children were slightly more likely to borrow (90%) compared to those without children (87%), indicating that additional financial responsibilities, such as childcare and education expenses, continue to drive financial strain. Income level further amplifies disparities, with low-income earners being the most affected—100% of respondents in this category reported borrowing at least a few times. Among middle-income earners, 89% had to borrow, while even among high-income respondents, the number remained high at 91%. This suggests that while the number of people facing direct financial strain has declined, borrowing remains a widespread coping mechanism, highlighting the ongoing financial vulnerability of households.

For FMCG brands in South Africa, winning in 2025 means navigating a market where financial strain remains, but some consumers are regaining financial flexibility. While fewer people report being negatively impacted by rising prices, borrowing remains widespread, reinforcing affordability as the key driver of purchasing decisions. Brands must continue prioritizing budget-friendly pack sizes, bulk-buying options, and competitive pricing to align with evolving consumer needs. The shift toward private labels and cost-effective alternatives will persist, making it crucial for national brands to emphasize value, quality, and strategic promotions to maintain loyalty. Essential categories such as food, personal care, and household goods will remain resilient, while discretionary segments must reposition products as affordable indulgences. Additionally, as financial conditions stabilize, brands have an opportunity to reintroduce fortified and nutritious products that cater to both affordability and well-being.

To win in 2025, brands must refine their distribution strategies to align with shifting spending patterns. While financial strain is easing for some, borrowing remains a reality for many, underscoring the need for greater accessibility across all income segments. Strengthening distribution in informal retail markets will be essential for reaching cost-conscious consumers, while e-commerce and digital platforms will play a bigger role in price comparisons and flexible payment options. Optimizing supply chains will be crucial to maintaining affordability without sacrificing quality. Ultimately, success will come to brands that stay agile, anticipate consumer shifts, and strike the right balance between affordability and value in an increasingly price-sensitive market.

Share on socials using this caption: 📉💵 Rising costs are still forcing majority of South Africans to borrow just to afford daily essentials. While some relief is emerging, financial strain continues to impact consumers across all segments. How are you managing? 🛒💰 #CostOfLiving #InflationCrisis #SouthAfrica #FinancialStrain

1680 views

Share article

Trust Is Becoming Economic Infrastructure

Consumer confidence loses momentum in October

Confidence plateaus in September as caution defines household behavior