Sandra Beldine Otieno, MSc

May 15, 2025

Share article

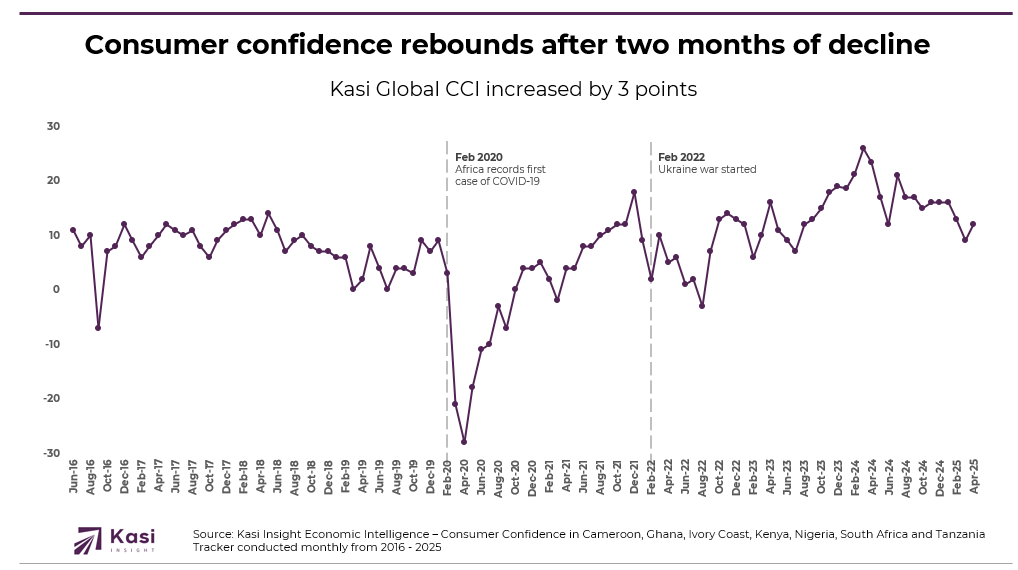

In April, African consumer confidence rose by 3 points, breaking a two-month streak of decline. This rebound was mainly fueled by improving expectations for the future, even as current conditions remained fragile. Household income and personal finance indicators showed solid gains, while spending and job sentiment were mixed. At the national level, Tanzania emerged as a clear standout, while Ivory Coast saw the steepest decline in consumer sentiment.

In April, household indicators pointed to a modest rebound in consumer confidence, driven primarily by improvements in personal financial sentiment. The household income index rose by 8 points, reflecting growing confidence in earnings and income stability. Likewise, the personal finance index increased by 5 points, suggesting that more households felt better equipped to manage their finances. These gains signal a slow but encouraging recovery in financial well-being after a period of strain.

However, this renewed confidence did not fully translate into increased spending. The household spending index declined by 4 points, and the discretionary spending index edged down by 1 point. These declines suggest that despite improved income perceptions, many consumers remained hesitant to loosen their budgets. Rising living costs, coupled with broader uncertainty, may be prompting households to prioritize savings or delay non-essential purchases.

Labor market sentiment also continued to weigh on overall confidence. The job prospect index fell by 2 points, indicating persistent anxiety around employment stability and future opportunities. Still, perceptions of the broader economic environment improved meaningfully. The general country economic conditions index jumped by 12 points, and the general city economic conditions index rose by 3 points. These shifts suggest that while households remain cautious in their own spending behavior, they are beginning to regain confidence in national and local economic recovery.

In April, consumer confidence across Africa improved slightly, ending a two-month period of decline. However, this recovery was not uniform and did not reflect a return to unrestricted spending. Key household indices such as discretionary and household spending continued to fall, suggesting that consumers are still focused on essential needs and exercising caution. In this environment, brands should continue to prioritize relevance, value, and empathy. Consumers are more likely to respond to clear, honest communication about functionality and savings rather than lifestyle-driven promises that feel out of touch.

Although perceptions around income and personal finances improved in April, concern around job prospects remained. This means that while households may feel marginally better about their finances today, they are still uncertain about the future. Brands can respond by making purchasing easier and more flexible. Offering affordable pack sizes, value bundles, and pricing consistency builds trust. Introducing accessible payment models, such as installment plans or low-commitment subscriptions, can help consumers manage short-term pressure. Brands that remove friction and show they understand everyday financial realities will build stronger emotional and commercial connections.

The shifts in confidence across countries also highlight the need for locally responsive strategies. Sentiment rose sharply in Tanzania and improved in Kenya and Nigeria, while it declined in South Africa, Ghana, Ivory Coast, and Cameroon. These differences matter. In markets where optimism is returning, brands can cautiously explore innovation and experience-based marketing. In more fragile environments, the focus should remain on protecting market share and reinforcing essential value. By staying close to what consumers feel and need in each market, brands will remain relevant, resilient, and trusted throughout the recovery.

Share on socials using this caption: 📈🛍️ Consumer confidence in Africa edged upward in April, breaking a two-month decline. While financial optimism improved, spending remained cautious as consumers focused on essentials. #ConsumerConfidence #AfricaInsights #SpendingTrends #EconomicUpdate

1464 views

Share article

Trust Is Becoming Economic Infrastructure

Consumer confidence loses momentum in October

Confidence plateaus in September as caution defines household behavior