Alison Okatch

May 21, 2026

Share article

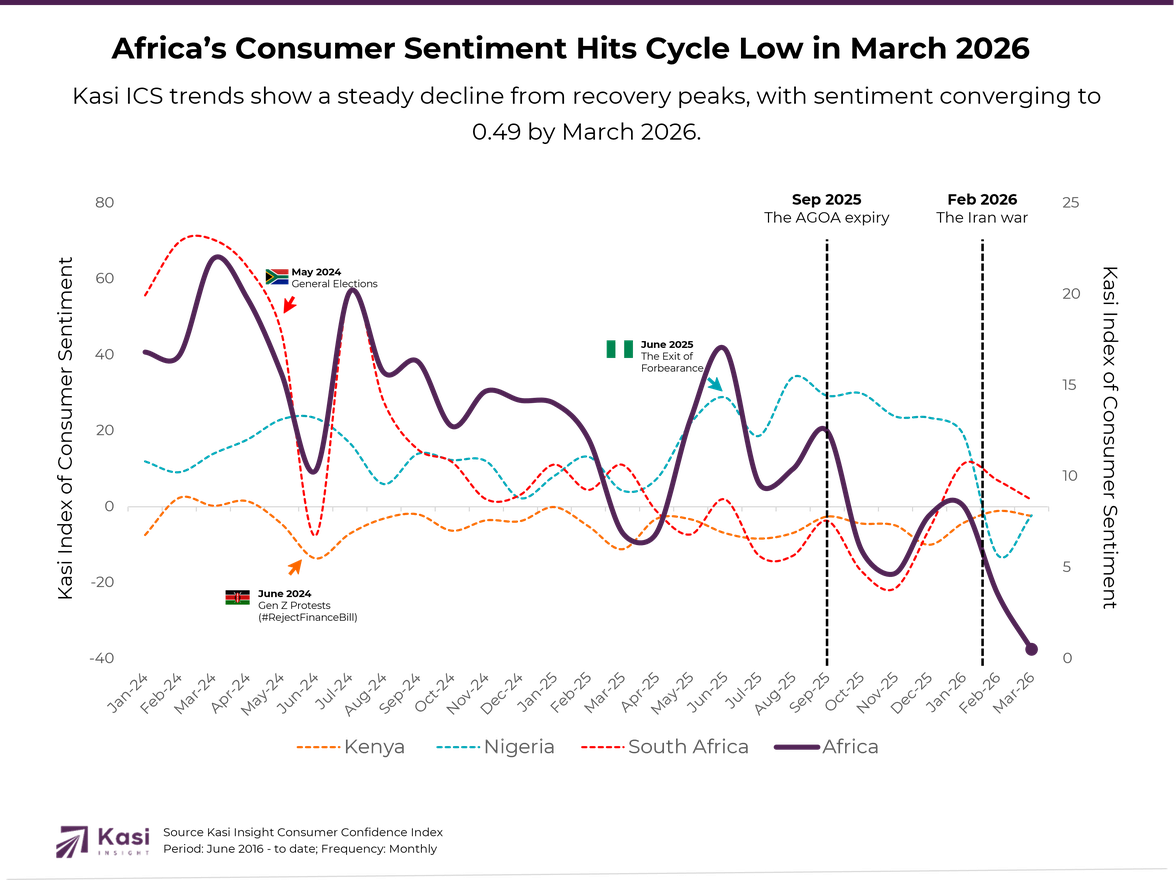

The Kasi Index of Consumer Sentiment (ICS) provides a monthly reading of how African consumers are navigating economic conditions, capturing shifts in confidence across personal finances, local economies, and national outlooks on a scale. The index offers a structured view of whether consumers are becoming more willing to spend or increasingly cautious. A reading above zero signals net optimism and stronger consumption intent, while values below zero reflect constrained confidence and more defensive spending behavior. By tracking sentiment continuously from June 2016 to date, and disaggregating results by demographic groups such as age and gender, the ICS provides a deeper insight into how different segments experience economic pressure and opportunity.

Africa’s consumer sentiment weakened further in March 2026, with the continental Kasi ICS falling to 0.49, down from 3.56 in February. While the decline coincides with geopolitical tensions and the Iran-related disruption that emerged in late February, the March results suggest consumers were already entering the period from varying levels of strength and vulnerability.

The March slowdown therefore appears to be an acceleration of existing pressure rather than a new crisis event. Several markets had already shown softer momentum through late 2025 and early 2026, meaning the external shock likely amplified caution rather than creating it.

Across markets, sentiment became more restrained as consumers reassessed household spending, affordability and future expectations. However, the data does not point to broad-based distress across the continent. Instead, it shows a moderation in optimism, with markets responding differently depending on their recent sentiment path and underlying economic conditions.

Kenya (-2.45 | ▼ Down from -1.13)

Nigeria (-2.29 | ▲ Up from -12.7)

South Africa (1.82 | ▼ Down from 6.98)

Cameroon (6.42 | ▲ Up from 4.26)

Ghana (16.76 | ▼ Down from 24.69)

Tanzania (-12.77 | ▼ Down from -7.36)

Ivory Coast (-12.91 | ▼ Down from 4.89)

Uganda (9.91 | ▼ Down from 10.9)

The Iran-related shock likely intensified concerns around fuel, inflation and spending, but the depth of impact was shaped by where each market already stood. Markets that entered March from weaker momentum experienced deeper pressure, while those with stronger sentiment foundations remained more resilient.

For brands and businesses, treating Africa as a single consumer story. While the external shock created pressure across markets, consumer response was shaped by existing sentiment trends and local market conditions.

Shift from expansion messaging to value reassurance. With sentiment softening and consumers becoming more cautious, brands may need to reinforce value, affordability and practicality rather than relying purely on aspiration-led messaging.

Focus on resilience segment even in softer environments, spending does not disappear; it becomes more selective. Consumers are likely to prioritize essentials, trusted brands and products that deliver clear value.

Shift from regional strategy to sentiment-based segmentation. Winning approaches now require tailoring to consumer confidence rather than geography, focusing on value protection in weaker markets and momentum retention in stronger ones, while avoiding assumptions of uniform recovery.

External events may trigger shifts in sentiment, but underlying consumer conditions determine the depth of impact. The opportunity for brands lies in identifying where resilience remains and adapting market-by-market responses accordingly.

About Kasi Insight

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

418 views

Share article

Africa's Consumer Confidence Slips Back Into Negative Territory in May

Assessment Of the Potential for Trade and Investment Exchanges Between Quebec and Africa

From Price Shock to Structural Reallocation; How Inflation Has Reshaped Everyday Life in Tanzania